For many U.S. consumers, raising the debt ceiling is usually one of those pieces of legislation that just passes. But in a sign of living in anything-but-usual times, the U.S. government is facing a default that the Congressional Budget Office (CBO) now estimates could arrive as soon as June 1.

This update from the CBO’s previous July forecast comes amid reports by The Wall Street Journal and other outlets that any resolution is far from secure. Although there have been past grumblings and skirmishes in Congress about raising the debt ceiling, such measures have historically passed with the Treasury having to seek a limited amount of “extraordinary” measures. And so, in usual times, these debates don’t much affect small and medium-sized businesses (SMBs).

These are not usual times, however, and no such promise is secure. The White House has outlined how hitting the ceiling, and having the government no longer able to repay its debts, could affect businesses of all sizes. SMBs, which usually carry a higher lending risk, would have diminished borrowing capabilities as it would cost financial institutions (FIs) more to extend these loans as interest rates rise.

Shaking international markets, as countries may rethink investments should a default occur, hitting the debt ceiling may also result in an extended dip in consumer confidence. This in turn could result in more layoffs and further economic contraction, turning recession fears into reality.

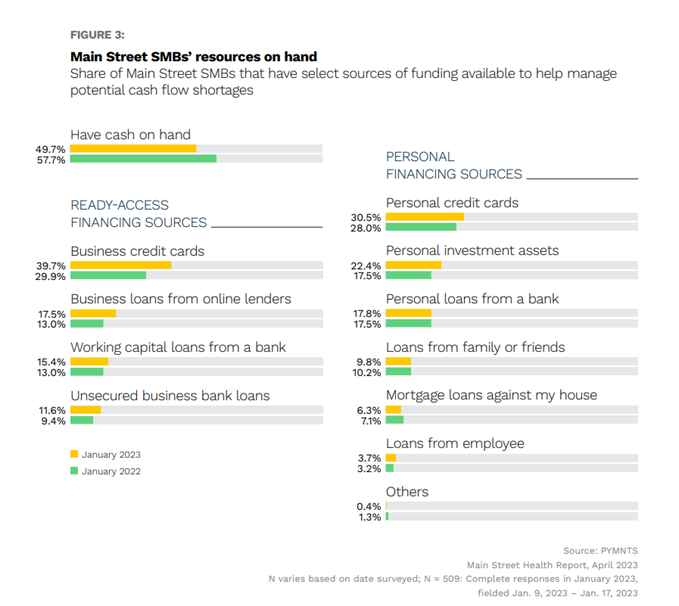

A hint to the extent hitting the debt ceiling and a resulting default may further affect SMBs is detailed in PYMNTS’ collaboration with Enigma, “Main Street Health Q1 2023.” Illustrated is the reliance on credit by Main Street small businesses when it comes to managing cash flow shortages.

Rates rising in the event of a default may be especially relevant to the over half of SMBs relying on credit or other loans, including personal mortgages, to keep their businesses afloat. Credit has already been drying up in the wake of the collapses of Silicon Valley Bank and other regional banks as 9% of SMBs report more problems securing their last loan than in previous attempts. Any extended debt ceiling debate could not come at a worse time, then, for SMBs seeking loans.

Some alternative financing sources for SMBs exist that may cushion the lending blow should a default occur, including buy now, pay later platforms aimed solely at businesses. Additionally, the Small Business Administration recently lifted its moratorium on licensing new Small Business Lending Companies which includes the ability for certain nonprofits to make loans.

There’s no crystal ball here when trying to read into the debt ceiling debate and negotiations may well go to the eleventh hour. Should the government default, however, businesses of all sizes may have to prepare for some serious credit pain.