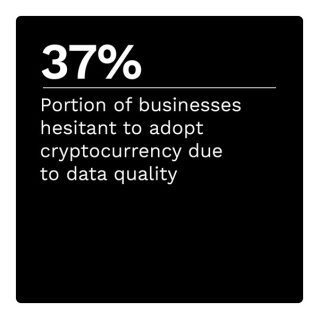

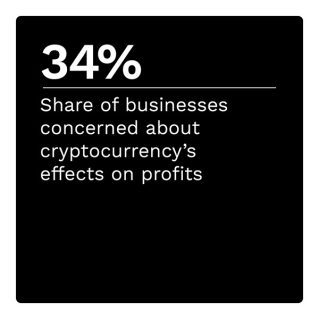

Cryptocurrency is exploding in popularity but brings with it significant personal and societal risks. Bitcoin, for example, was valued at approximately $16,000 per coin in 2017 before skyrocketing to nearly $65,000 last year, just to plummet right back down to its current value of approximately $20,000. Experts have also raised significant concerns about the blockchain’s environmental impact, with a single transaction using more energy than the average U.S. household consumes in a week.

Countries across the world are taking regulatory action in an attempt to solve these pressing blockchain issues. The White House, for example, is calling for legislation that would develop comprehensive standards for the cryptocurrency industry’s environmental issues. The European Union, meanwhile, recently enacted legislation that would allow cryptocurrency wallet providers to market themselves across the continent so long as they meet certain anti-money laundering and stability requirements.

The “Blockchain Payments Tracker®” examines the latest developments in the evolving blockchain field and why lawmakers and businesses are working to enable blockchain regulation.

Around The Blockchain Payments Space

Bad actors sometimes use cryptocurrency in scams and illicit purchases, with the real estate field emerging as a new favorite for cryptocurrency scammers. The United Arab Emirates recently announced new regulations to curb cryptocurrency real estate fraud and money laundering, requiring real estate agents to alert authorities of any property purchased using cryptocurrency.

Bad actors sometimes use cryptocurrency in scams and illicit purchases, with the real estate field emerging as a new favorite for cryptocurrency scammers. The United Arab Emirates recently announced new regulations to curb cryptocurrency real estate fraud and money laundering, requiring real estate agents to alert authorities of any property purchased using cryptocurrency.

Employees of the United States government are typically subject to strict ethics rules to ensure that they are not unfairly profiting from their positions, and these regulations have just been updated to account for non-fungible tokens (NFTs). The new guidance says that government employees must file financial disclosures if they own an NFT worth more than $1,000 or if the asset produces more than $200 in income during the reporting period.

For more on these and other stories, visit the Tracker’s News and Trends section.

Navigating The Confusing Regulations In The Blockchain Field

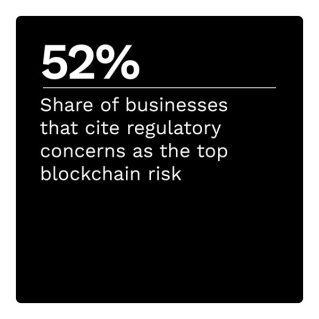

Regulators have been toying with the idea of regulating the blockchain field for several years, but they only recently started passing legislation in earnest. These regulatory efforts are still nascent, however, as lawmakers struggle to understand this complex technology and craft appropriate legislation.

To get the Insider POV, we spoke with Andreas Veneris, professor of electrical and computer engineering at the University of Toronto, about why cross-border payments would be a good start for blockchain regulation.

The U.S. And EU’s Regulatory Priorities

A recent study found that the blockchain global market size is expected to hit $4 billion by 2026, driven by more than 81 million cryptocurrency wallets and its multitude of other functions. This colossal growth is drawing the eyes of government regulators, however, who seek to constrain fraudsters, limit the environmental impact and protect investors and enthusiasts from the potential drawbacks of blockchain technology.

This month’s PYMNTS Intelligence examines current and upcoming blockchain regulations in the U.S. and the EU.

About the Tracker

The “Blockchain Payments Tracker®” examines the latest developments in the evolving blockchain field and why lawmakers and businesses are working to enable blockchain regulation.