Data demonstrates that any rumors of the installment plan’s demise may have been greatly exaggerated.

By most accounts, buy now, pay later (BNPL) and similar installment plans are having their heyday. Consumers across income and age demographics have embraced the option as one alternative to credit cards, whose interest rates are tied to the Fed’s policy-making decisions. Its utility has recently been reimagined as a way of helping patients out from crushing medical debt. BNPL has is also moving beyond its roots a consumer-facing product as some firms explore its utility as a credit option for B2B marketplaces.

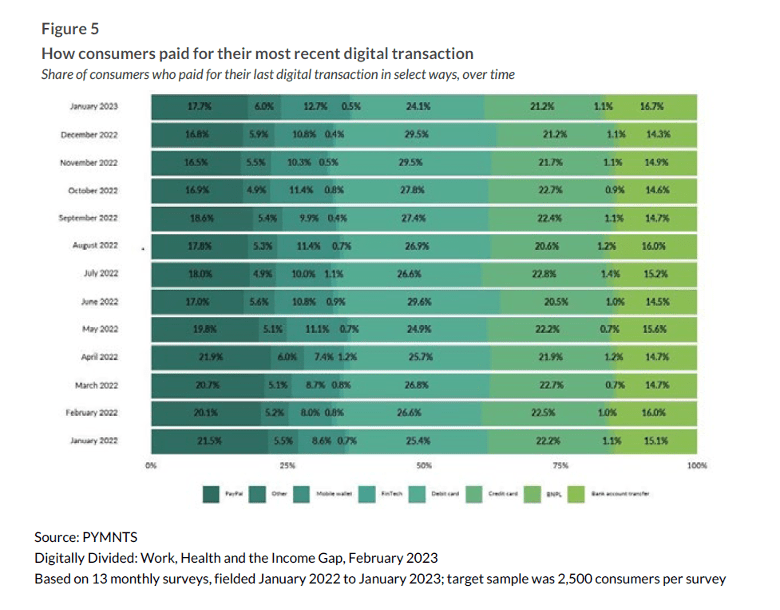

The latest PYMNTS’ ConnectedEconomy™ Monthly Report, “Digitally Divided — Work, Health and the Income Gap” demonstrates these anecdotes of BNPL’s staying power. Perhaps not in market share, as any platform has a long way to go in disrupting credit and debit cards’ hold on in-store and eCommerce, but in consistency.

While there is some month-to-month variation, BNPL as consumers’ payment choice for their most recent digital transaction between January 2022 and January 2023 remained remarkably even. Its low use rate may be partially attributed to wide availability as payment choice. Merchants and retailers have only begun exploring incorporating BNPL into its cross-channel sales as part of a greater customer loyalty play. While some security concerns linger over host trustworthiness, bank-backed BNPL plans are gaining support by both consumers and merchants alike as financial institutions started the year with increased BNPL offerings.

So, why all this talk about BNPL firms losing their footing, especially as the major sector firms report record earnings? Two words: market saturation. Simply because the product has promise doesn’t mean that every player will reap the benefits. In some cases, like PayPal, first to market means top spot. Others, like Klarna and Sezzle, have become major competitors through actively seeking partnerships and identifying additional revenue sources. Without these unique selling points, questionable choices such as Affirm’s to raise merchant interest rates could lead to company downsizing.

BNPL utility as a credit tool has only just begun as it evolves beyond the traditional retail installment plan into bill pay and B2B marketplaces. Viewing the thinning of BNPL competitors and current low transaction uptake as a sign of its doom may be counting the innovation out early.

See More In:

Affirm, BNPL, buy now pay later, Featured News, installment plans, Klarna, News, payments, PayPal, Retail, sezzle