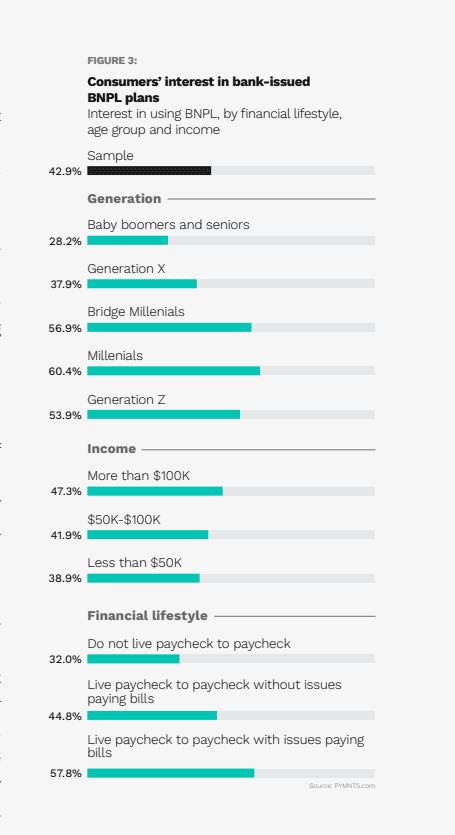

Buy now, pay later (BNPL) plans from FinTechs such as Klarna and Affirm are gaining popularity as shoppers seek alternative financing to avoid rising credit card interest rates. However, PYMNTS research has found that 70% of current BNPL users say they would be interested in BNPL plans offered by their banks. Millennials are more interested in bank-backed BNPL payment plans than any other generation.

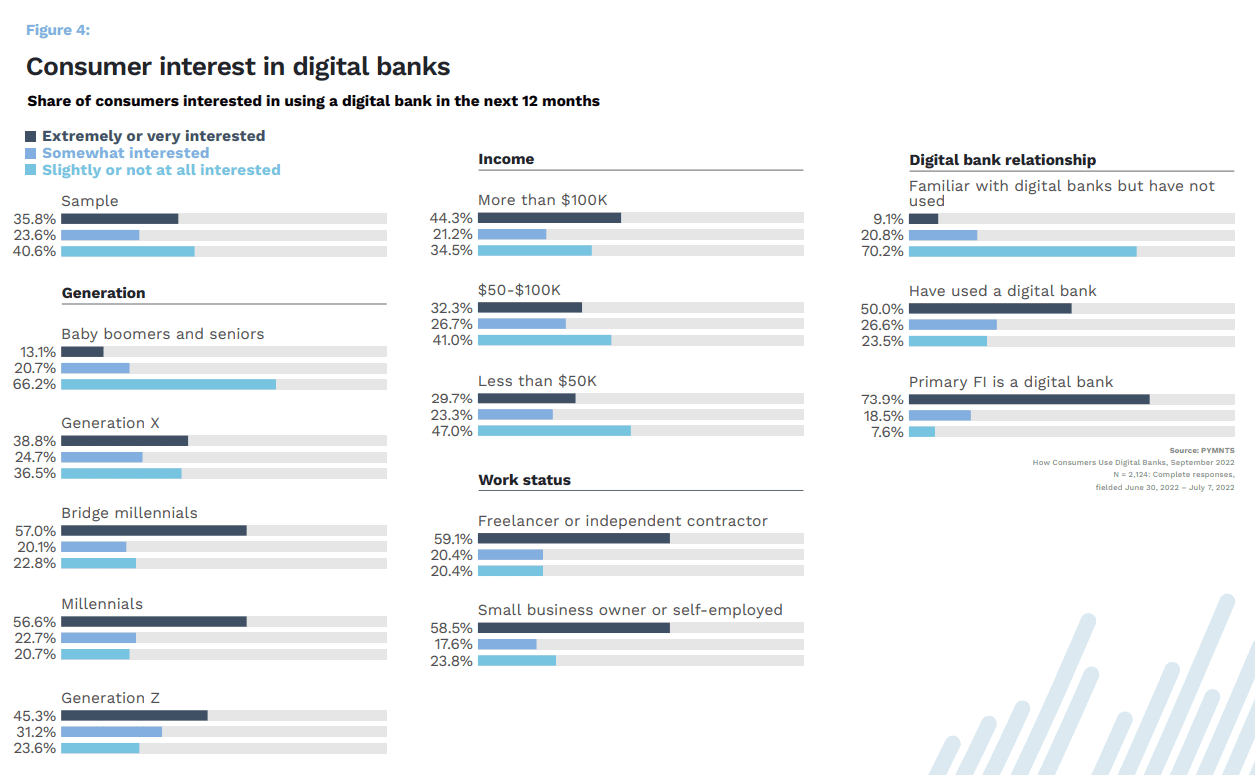

And, synchronously, PYMNTS’ report, “How Consumers Use Digital Banks,” found that millennials are the generation most interested in utilizing digital-only banks.

Digital-only banks, running on thinner margins than traditional financial institutions, have little room for error when releasing new consumer-facing programs and products. Given this need for more precise initiatives than their larger counterparts, neobanks may seek offerings they know are a “sure” bet. Bank-backed BNPL could be one approach to filling that need. The crossover of millennial interest represents an opportunity for digital-first banks to entice consumers seeking to build wealth away from traditional financial institutions.

Digital-first banks unable or unwilling to roll out their BNPL programs can partner with third parties. This may enable more seamless integration into the bank’s suite of offerings – possibly with more customizations than an in-house BNPL program could provide.

In an interview with PYMNTS, Galileo Chief Product Officer David Feuer described the breadth of his company’s latest customizable BNPL product for banks and FinTechs. “We look at everything — the payment terms, the repayment schedule, how many payments, what is required upfront, how the credit box looks — and we make it an environment where all of that is customizable, where the FinTech or neobank offering the loan are able to have whatever parameters necessary to build out a customer experience that best meets their needs.”

Some digital-only banks are already putting their own BNPL programs into place. In December, SoFi announced a partnership with Mastercard, becoming the first bank to launch the Mastercard Installments program. With the Pay in 4 option, qualified SoFi members can split a purchase between $50 and $500 into four interest-free payments. The program is not intended for everyday transactions but is instead meant for larger purchases such as airfare and home improvement.

In an interview with PYMNTS’ Karen Webster, Mastercard’s Chiro Aikat predicts eventual global acceptance of BNPL as more financial institutions and lenders make the payment plan accessible to their respective customer base. “These institutions are going to want to take advantage of a new way of paying — and this is just the start of a journey that we’ve been on for the past year and a half.”

By marrying millennials’ demands for digital-only banks and BNPL, neobanks may find a uniquely timed loyalty strategy. Getting these potential customers to make the switch at the beginning of their financial journey may be far easier than after banking habits and loyalty have become ingrained. https://www.pymnts.com/news/banking/2022/americans-hesitant-to-break-up-with-big-us-banks/