While buy now, pay later (BNPL) is certainly a disruptor of traditional credit like store-issued co-branded cards and major credit cards, in reality, BNPL has a long way to go before it presents a true threat to more established payment methods, namely charge cards.

Getting to the heart of this matter is a new study, “The Truth About BNPL And Store Cards Report” a PYMNTS and PayPal collaboration. The survey of nearly 2,200 U.S. consumers taken in December 2021 as holiday shopping was in full swing found that 87% of consumers used store-issued cards whenever possible, while 13% used other traditional cards or cash.

The study states that “zero percent of consumers with store cards paid for their most recent eligible purchases via BNPL.”

Additionally, only 4% of store cardholders planned to use only BNPL in the next three months, and 12% said they’re likely “to use a combination of BNPL and store cards in that time.”

Store cardholders from Generation Z were the most likely of any age group to plan on paying via BNPL in the next three months, and millennials were a close second. Even among Gen Z and millennial store cardholders, however, just 8% and 6% intended to use BNPL for purchases within the next three months, respectively.

It’s surprising given the headlines that BNPL keeps generating, and the attention this alternative form of credit is getting from lawmakers who fear consumer credit bloat from overusing BNPL.

It’s surprising given the headlines that BNPL keeps generating, and the attention this alternative form of credit is getting from lawmakers who fear consumer credit bloat from overusing BNPL.

Findings from “The Truth About BNPL And Store Cards Report” show that consumers are using these payment methods more and more for specific types of purchases, and for their spend management capabilities.

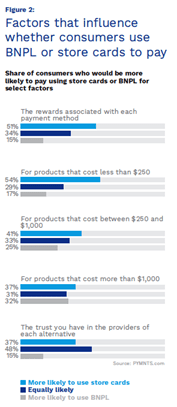

Rewards are the main gain from using store-issued cards, researchers found, while BNPL use is tied to affordability. The study states, “the higher the price, the more likely consumers are to use BNPL. Our research shows that 32% of all consumers would be more likely to pay with BNPL than store cards for purchases costing more than $1,000. Just 17% would be more likely to pay via BNPL than store cards for items costing less than $250.”

As BNPL matures and consumers come to understand it better, usage patterns indicate that they see it as a tool for specific tasks like tracking and managing spend.

The study states that “68% of consumers believe BNPL options allow them to better track the payments they make for their purchases and 78% believe BNPL options allow them to make larger purchases.”

Compare that to the 41% of consumers who say store cards are better for larger purchases, and the 42% who believe “store cards make payments easier to track than other options.”

Speed and convenience bear on this as well. PYMNTS found that “40% of the cardholders who did not use their cards to make their most recent eligible purchases said it was because using credit cards, debit cards or, to a lesser extent, PayPal was faster and more comfortable.”

Speed and convenience bear on this as well. PYMNTS found that “40% of the cardholders who did not use their cards to make their most recent eligible purchases said it was because using credit cards, debit cards or, to a lesser extent, PayPal was faster and more comfortable.”

In the census-balanced survey of 2,161 U.S. consumers taken Dec. 10 to Dec. 17, 2021, 52% of respondents were women, 32% held college degrees and 36% earned over $100,000 annually. Another 34% of respondents were baby boomers or seniors, 27% were Gen X and 28% were millennials.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More