At a time when investors are increasingly risk averse, it is important that buy now, pay later (BNPL) firms — and FinTechs more generally — reevaluate their business strategies. Investors are prioritizing present profits over rapid growth, so companies need to pivot toward a model of achieving sustainability and profitability.

Turning a profit can be challenging even in the best of times, and the regulatory uncertainty and economic headwinds facing the BNPL space make it more difficult still. While there is no fail-safe path to profitability, there are steps companies can take to move in the right direction.

Cost Reductions and Partnerships Can Help Steer Companies to Profitability

Cost Reductions and Partnerships Can Help Steer Companies to Profitability

The first thing that FinTechs can do is to cut costs and reduce spending. A common way to do this is through layoffs, as many have already done. Companies can also reduce expenses by scaling back their operations and scrapping underperforming products and services.

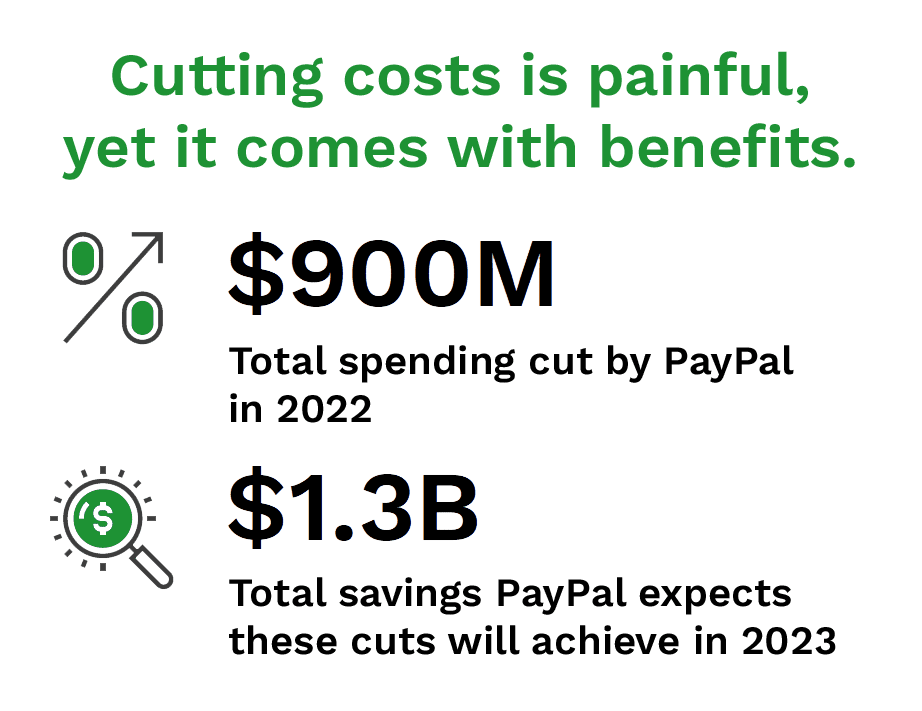

Although painful and difficult, these moves can be very effective. PayPal, for example, cut spending by $900 million in 2022, partly with layoffs, in anticipation of saving $1.3 billion through 2023, and markets responded well to these moves. Moreover, after Australian-based BNPL platform Zip Co. ceased operations in the United Kingdom and Singapore, it ended the year with $78.5 million in cash and liquidity — and, according to its CEO, Zip will break even by the end of the financial year.

In addition to cutting costs, FinTechs can pursue partnerships. Despite the BNPL industry’s challenges, this lending type is still popular among consumers. Traditional financial institutions, tech companies and payments providers are aware of this, and many are interested in getting into the BNPL space. The same holds true for merchants, and many have partnered with BNPL firms. Expedia, for example, partnered with Afterpay to allow customers to split up payments for travel. Finally, analysts also anticipate opportunities for mergers and acquisitions in 2023 and beyond.

Companies Can Increase Revenue With New Products and Services

Another avenue FinTechs can pursue involves expanding product offerings. Some providers are now offering debit cards, while others, such as Affirm, are offering short-term financing products in addition to pay-in-four arrangements. Companies can also adopt Installments-as-a-Service products. Splitit, for example, is using funds to bolster its white-label offering with global enterprise merchants.

There is also a promising opportunity to expand BNPL to B2B payments. The incentive here is that B2B purchases tend to be larger than those made by consumers, and according to one prediction, the market for B2B BNPL transactions in the U.S. and Europe will eclipse $200 billion within a few years. Companies are already exploring this possibility. Allianz Trade, Two — a B2B eCommerce platform — and Santander Corporate & Investment Banking have partnered to create a global B2B BNPL solution for multinational corporates.