Deferred payment plans such as credit card installment plans and buy now, pay later (BNPL) options have gained popularity among consumers in recent years, providing a convenient way for consumers to manage their spending and make large purchases more affordable.

According to a joint PYMNTS Intelligence-AWS survey, consumers use deferred payment plans for three main reasons: convenience, financial cushion, and the ability to purchase more products. Against this backdrop, 28% of consumers reported using deferred payment plans in the last three months, including BNPL and credit card installment plans.

Source: PYMNTS.com

However, while credit card installment plans have seen widespread usage, BNPL still lacks certain features that potential users demand.

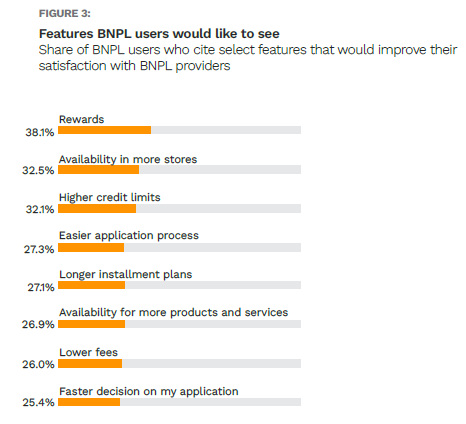

In fact, the survey found that BNPL users have specific features they would like to see in order to improve their satisfaction with BNPL providers. For example, the study found that 38% of consumers would like to see BNPL offering more and better rewards.

One of the prominent features that credit card users enjoy that BNPL lacks is the ability to earn rewards for their purchases. Take for example the collaboration between Chase and Amazon, which since May enables Prime Visa and Amazon Visa cardmembers to earn 5% back and 3% back, respectively, on purchases made through Chase Travel, Chase’s new and enhanced travel booking platform.

More recently, payments FinTech Fiserv announced that it is allowing cardholders at financial institutions that are part of its uChoose rewards program to redeem points on qualifying Amazon purchases, another example of the wide gap between BNPL and credit card incentives.

Another aspect where BNPL lags behind credit card installments is in-store availability. While credit cards are widely accepted, BNPL services still have limited acceptance in physical stores, highlighting a need to expand their network of partner stores and increase acceptance. As noted in the study, about 33% of consumers expressed their desire for BNPL to be more widely available in brick-and-mortar establishments — a move which will enable BNPL lenders to enhance convenience for users and make their services more appealing for larger purchases.

Additionally, 32% of consumers highlighted their need for higher credit limits with BNPL, which — unlike credit cards — often limits the scope of purchases that can be made.

Overall, while credit card installments currently dominate in terms of frequency and larger purchases, BNPL services have the potential to bridge this gap by incorporating features that potential users demand such as reward programs, higher credit limits, lower fees, easier application process and faster decision on applications to create a more comprehensive and appealing offering.

Addressing these demands can go a long way to make BNPL a preferred choice for consumers, encouraging them to use the service more frequently and for larger purchases.