The whipsaw action in the stock market feels a bit more like whiplash.

A brief few days of rallies, and then a plummet — and this past week, no surprise, saw macro concerns driving the action. Any hopes for a more “dovish” stance on interest rates were dashed, at least for now, by jobs numbers and a low unemployment rate that indicate that the economy is still running “hot.”

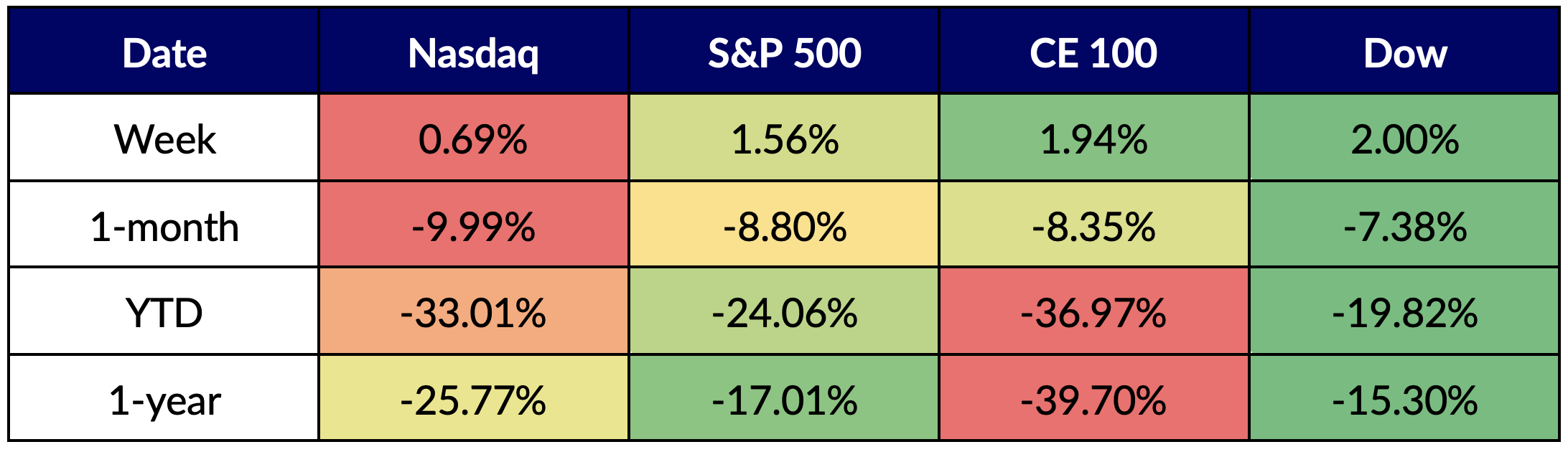

And yet, the ConnectedEconomy™ 100 (CE100) Stock Index, and the broader markets, managed to eke out some gains — in this case, ending the week up 1.9%.

CE100 Relative Performance

Source: PYMNTS

All Pillars Gain Ground

All pillars were in the black this time around, and the Pay and Be Paid group led the pack, gaining just under 4%.

Sezzle surged 16.2%, and though there was no company-specific news underpinning the rise, the snapback in this name, and in others, might be due to a bit of relief that consumers are still spending. Per data at the end of last month, consumer spending in August rose 0.4%, aligning with bigger paychecks and rebounding from a decline in July even as inflation remains elevated.

Meanwhile, PayPal gained 4.8% and Block (Square’s parent company) gathered 4.4%. In the case of the former, PayPal clarified this past week that a reported acceptable use policy that stated users would be fined up to $2,500 if they use the service to “promote misinformation” was sent out in “error” and would not be taking effect.

Block’s rise came as Square has launched artificial intelligence (AI) features within its Square Messages platform, allowing merchants to communicate with customers using suggested replies and actions. As noted in this space, Square said that these AI messaging features help to “boost a buyer’s reply rate by 10%.”

See also: Square Debuts AI Features for Conversational Commerce Platform

But the standout was Peloton, which leaped 25% on the week. As PYMNTS reported, the company has undertaken its fourth round of layoffs this year to help shift its fortunes. The news comes after a recently-announced partnership with Hilton.

Eight months into the job as the new head of Peloton, CEO Barry McCarthy — former CFO at Spotify and Netflix — said the company has six months to put up the numbers to show it can operate as an independent organization now that people have re-established everyday post-pandemic routines and embraced new behaviors.

There were some names that declined, of course. Tesla lost 15.9%, and Elon Musk has been in the midst of plotting a course for Twitter and what might happen when a buyout is done.

Learn more: Musk’s Super App Ambitions Face Uphill Battle

It may be the case that there are concerns about what happens to Tesla, with attention diverted in the bid to build a super app. Musk is reportedly in the running to debut an as-yet-undefined offering that will (at least for now) be known as “X, the everything app.” There’s no real detail beyond that.

Additionally, DocuSign was 10.5% lower. Headed into last week, the company said it would lay off about 9% of its workforce to help improve its operations and margins.