As the impact of rising prices on bill payments becomes more pronounced, U.S. consumers are increasingly relying on credit cards to manage their finances. Cardholders are also seeking credit cards that offer rewards and financial management features to navigate the economic turbulence, as inflation takes a toll on incomes and purchasing power.

In “Credit Card Use During Economic Turbulence,” PYMNTS Intelligence leverages insights gathered from a survey of over 2,200 U.S. consumers to examine the evolving role of credit cards in the U.S. in the face of inflation as well as identify trends in increased credit card usage.

According to findings detailed in the PYMNTS-Elan report published in May, one-third of cardholders have increased the share of their expenses paid by credit cards prior to the study, while only 15% have reduced their credit card spending. This surge in credit card usage is driven by the combination of higher costs and reductions in income, with more consumers turning to credit cards as a means to maintain their financial stability.

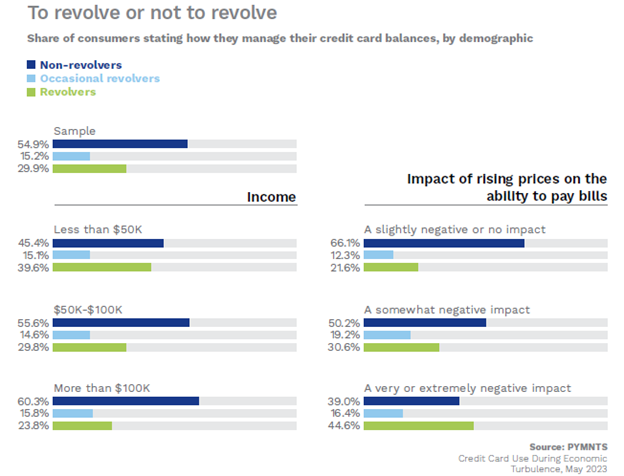

The research further indicates that the impact of rising prices strongly influences consumers’ tendency to carry revolving balances on their credit cards. In fact, while 22% of cardholders who experienced no adverse effects from rising prices regularly carry revolving balances, the percentage of cardholders carrying revolving balances more than doubles to 45% among those significantly affected by inflation.

Additionally, low-income consumers are more likely to revolve balances, with 40% doing so, while high-income cardholders are less likely, at just 24%. High-spending revolvers are also the most likely to shift more spending to their cards, with nearly half doing so.

When it comes to younger generations, they are also more inclined to increase their reliance on credit cards compared to older ones. Furthermore, 43% of consumers significantly impacted by higher prices have ramped up their card spending in the six months prior to the study.

Further data analysis suggests that while consumers most affected by inflation cite reduced income as the most important driver for increasing credit card spending, rewards and cash-back programs are the primary motivators for cardholders when choosing one card over another, at 31%, followed by real-time fraud monitoring alerts, at 13%.

The data also found that among various credit management personas, the value placed on monitoring features for fraud detection is consistent. However, among high-spending non-revolvers, a significant 68% prioritize these features above all others, surpassing the average of 62% among all other credit cardholders who share the same preference.

Rewards and cash-back programs also appeal to 13% of non-cardholders, yet within this group, the most sought-after feature is the capability to set spending limits, cited by 15% of consumers in this group.

In conclusion, the impact of rising prices on bill payments has led to an increased reliance on credit cards among consumers. With inflation eroding purchasing power, cardholders are seeking credit cards that offer rewards and financial management features to optimize their spending in real-time. By providing these features, credit card issuers can boost adoption rates and meet the evolving needs of consumers during economic turbulence.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More