The retail data released Tuesday (May 16) by the Commerce Department shows a reversal in consumer spending after two months of declines.

But one headline does not a rebound make.

And the more deeply one dives into the data, the more apparent it is that consumers have been pulling back on some key categories of discretionary spending — which does not auger well for retailers, and perhaps the payment networks and processors down the line.

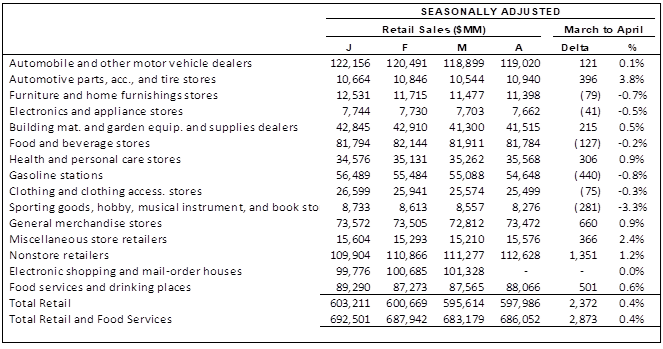

The data released by the Commerce Department Tuesday shows that on a seasonally adjusted basis, retail sales rose 0.4% in April. The gains reverse a 0.7% decline in March and a 0.4% decline in February, as measured month over month.

The chart below, using the government data and compiled by PYMNTS, shows that automotive parts, accessories and tires saw a bump in the latest month, up 3.8%. Non-store retailers, which traditionally encompass eCommerce firms, were up 1.2%. That’s a somewhat anemic growth rate in online sales, where the month over month rate was 1.9% as measured in March.

But sporting goods were off 3.3%, spending at electronics stores slid 0.5% and furniture displayed a 0.7% decline. As a category, clothing and accessories were off 0.3%. Sports and hobbies were 3.3% lower.

Slippage in Discretionary Categories

All of the above, we note, are categories that represent discretionary purchases. The auto sector? One can argue that getting the parts that are needed to keep our vehicles on the road are less discretionary, and there’s more need for parts given the fact that the cars themselves are aging. (The average is now more than 12 years, according to several sources.)

It’s relatively cheaper to triage repairs and keep putting miles on the family car, van or SUV than it is to go out and buy a new set of wheels. That’s been reflected in our recent coverage of online car platforms’ earnings results, where companies have noted their efforts to sell the inventory that’s been on hand for months, and where eCommerce sales have plummeted by double-digit percentage points.

Though the retail sales data shows a bump, the 0.4% positive print came in lower than the consensus of 0.7% — and April’s already in the rearview mirror.

Home Depot’s results on Tuesday morning splashed some cold water on sentiment that the rebound may prove longer lived (at least if stocks’ broad-based decline Tuesday has been any indication). Sales at the company were down 4.2% from the same period in 2022, and comp store sales fell 4.5% from the same period last year. Only four of 14 departments had positive comps.

Holding back on big ticket renovations may be low-hanging fruit, at least for now, as consumers forgo opening the wallet today in favor of waiting for a more opportune time to remodel. The slump here also hints that furniture sales could see a continued decline — ditto the electronics that tend to be snapped up to outfit a room.

But the question comes: What’s likely to happen to the discretionary categories that are still lagging into the summer months? Apparel, especially, might wind up crowding brick-and-mortar (and virtual) shelves, which makes the holiday season that much tougher.

SOURCE: PYMNTS, BLS Data