At least in some areas. As paycheck-to-paycheck living remains a reality for most U.S. consumers, the strategies are multipronged: trading down, trading off, or choosing where to allocate what seem to be increasingly limited resources.

Headed into 2024, PYMNTS found some shifts already in place. The share of consumers reporting that they had reduced the quality of the items they purchased dropped but was still significant at 32.5% in December. The share cutting down on nonessential spending was 61.6% in the same period.

There are some pockets of resilience, to be sure. Upcoming PYMNTS Intelligence data will spotlight the fact that many consumers will travel this summer. Only the subset of consumers who live paycheck to paycheck with issues paying bills don’t plan to travel this summer, or at least are unsure about those plans, representing roughly 56% of those surveyed.

However, the logic follows that if individuals are looking to get away from it all and book a trip, and they are seeking to find ways to pay for getting away from it all, they’ll need to shift at least some spending, especially with stubborn inflation.

The Big Picture on Income Remains Mixed

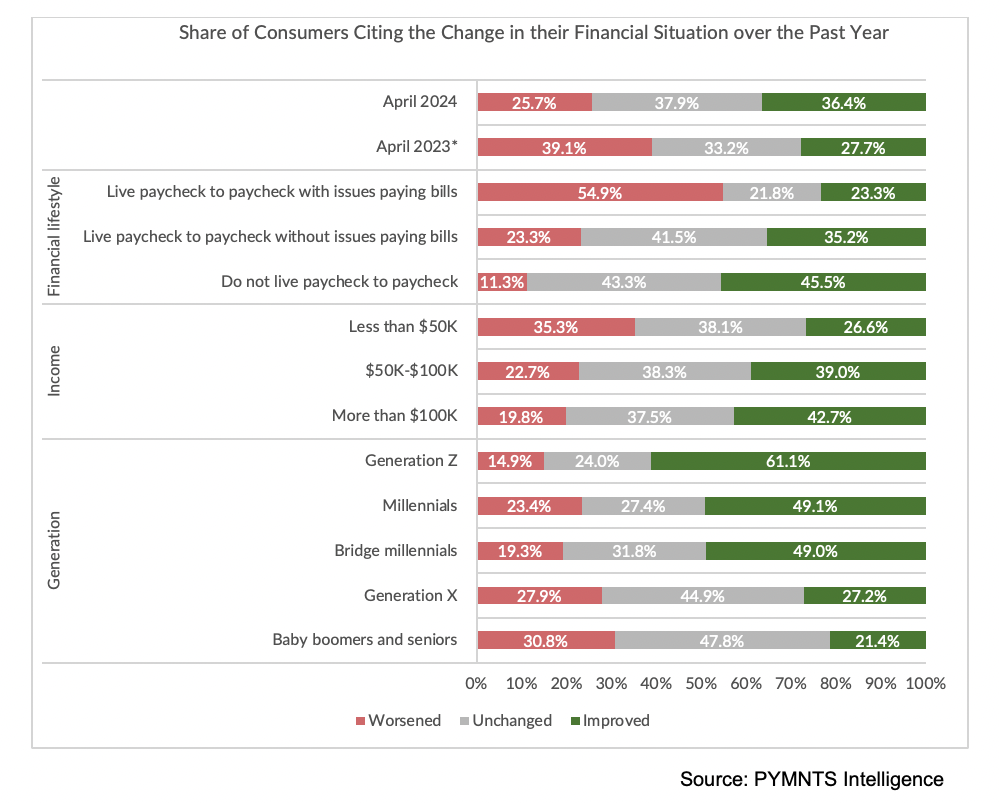

The big picture at first glance seems positive. As measured by PYMNTS Intelligence as recently as last month, more than 36% of consumers surveyed said their financial conditions had improved through the past year, which is a jump from the 27.7% who said the same last year. But drill down a bit, and the same survey showed that 55% of consumers with issues paying bills said their financial situation has worsened over the past year. In no cases did we see that most respondents think their financial situations have improved — no matter if the consumer is being viewed through the lens of income, paycheck-to-paycheck “status” or generation.

Percentages of Income Must Be Earmarked for the Essentials

Simply putting a roof over one’s head and paying for food eats up a significant share of the monthly budget. Across all demographics, we found that about a quarter of the budget is allocated to rent/housing costs. Grocery and household supplies represent a high teens to roughly a quarter of the budget. In the March retail sales data, there were shifts (and downright declines) in some spending categories, such as sporting goods and home furnishings.

More recently, as earnings season has wound on, there have been some telltale signs of pullbacks in what we might term “nice-to-have” items, where dollars saved can be earmarked for other goods and services. Starbucks, for example, saw headwinds from repeat business from occasional customers; and comp sales were down by 4%. Quick-service restaurants have seen some headwinds as disposable income has waned.

There’s Wide Recognition That Splurging Leads to Financial Distress

It’s the younger generations that have been feeling the pinch. PYMNTS Intelligence found that only about 10% of baby boomers and seniors said splurging has led to at least some financial struggle. The tally is nearly the same, at 16%, of Generation X consumers. But then we see some significant increases as the consumers skew younger. Twenty-four percent of millennials confessed that splurging on nonessential items contributes to their financial woes, and 34% of Generation Z consumers said the same.

Savings Are a Resource —but for How Long?

As of March, PYMNTS found, savings have been volatile. For consumers who do not live paycheck to paycheck, the March surveys indicated that consumers had about $22,000 in the bank, up from about $21,000 at the same period last year.

But for those who said they live paycheck to paycheck with no issues paying bills, savings dipped by about $500 through the same period to roughly $8,300.

For those consumers who struggle month to month to make ends meet, a year ago, these individuals and households had about $5,000 in the bank. The most recent reading stated that the cash coffers for these pressured consumers held just less than $4,000.

Earnings Season Is Depicting Some Stark Realities

Qualitative commentary from companies and management these past few weeks during earnings season has been telling.

Amid a few select examples, Citi CEO Jane Fraser said at the end of last month that consumers are becoming more cautious in their spending. Consumers are making small purchases, almost all spending growth is coming from affluent customers, and there is less spending by consumers with lower credit scores.

During Discover Financial’s earnings call, also last month, Chief Financial Officer John Greene said in his prepared remarks that card sales were down 1% compared to the prior year quarter.

“Sales slowed across categories with the largest decline occurring in the everyday category, which includes supermarkets, gas and wholesale clubs,” he said.