Many consumers hit their credit card limit at least sometimes, and for consumers struggling to get by financially, that percentage skyrockets.

The December installment of PYMNTS Intelligence’s “New Reality Check: The Paycheck-to-Paycheck Report” series, “The Credit Card Use Deep Dive Edition,” drew from a survey of more than 3,200 U.S. consumers to examine their financial lifestyles and explore how they use credit cards to manage their cash flows to get by.

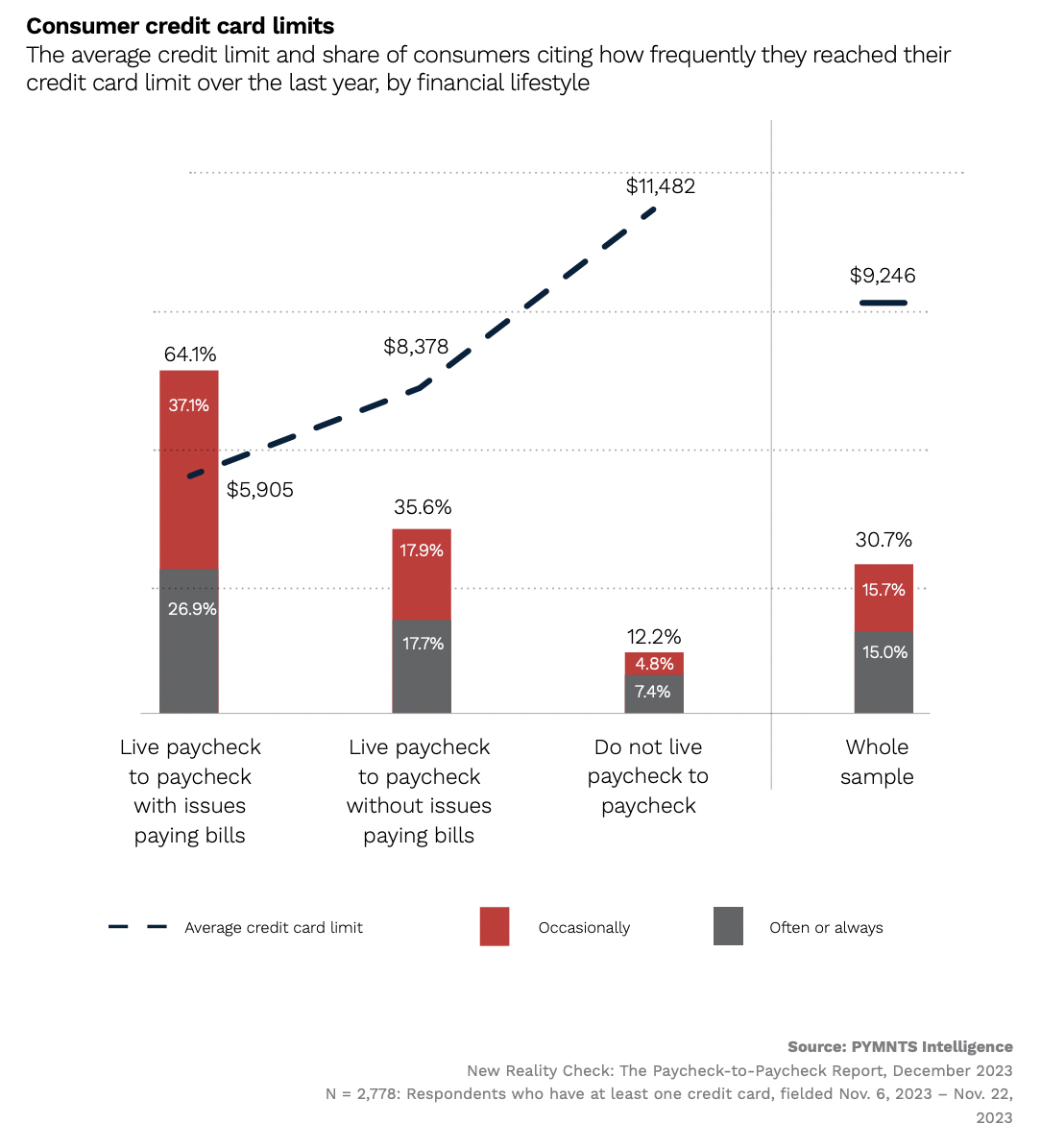

The results revealed that 31% of consumers said they had reached their credit card limit, which averaged $9,200, at least occasionally in the last year. That share more than doubled for consumers living paycheck to paycheck with issues paying their monthly bills. Nearly two-thirds of those in this group reported that they had reached their credit card limits, which averaged $5,900, at least occasionally in the last 12 months.

A study from the Federal Reserve indicated that it’s not income levels or ability to repay that drives banks’ willingness to extend credit. Rather, the use of credit — the engagement — is a factor in determining when, and by how much, credit limits are increased.

“Accounts with more engagement, as shown by income updates, may be more profitable” to the banks, according to the paper, titled “Income and the CARD Act’s Ability-to-Pay Rule in the US Credit Card Market.” The data showed that card holders using 40% to 50% of available credit on cards with higher annual percentage rates are more profitable due to the active use of the cards that indicate that consumers are “not using so much credit as to indicate liquidity constraints that might lead to delinquency.”

The Fed noted, too, that actual credit limits are “almost always substantially lower than reasonable ability-to-pay limits.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More