PYMNTS research shows that 36 percent of CUs consider microbusinesses to be a very or extremely important part of their member base, and that 41 percent consider microbusinesses’ unique banking needs when designing and implementing their innovation plans.

PYMNTS research shows that 36 percent of CUs consider microbusinesses to be a very or extremely important part of their member base, and that 41 percent consider microbusinesses’ unique banking needs when designing and implementing their innovation plans.

So, in which innovations are CUs investing in hopes of catering to this section of their broader communities, and how do they hope these innovations will help improve their bottom lines?

These are only a few of the questions PYMNTS sought to answer in the Credit Union Innovation Playbook: Microbusiness Opportunity Edition. In collaboration with PSCU, PYMNTS surveyed 100 decision-makers at CUs throughout the United States to gain a more thorough understanding of how microbusinesses help shape CUs’ innovation strategies, and how those strategies change depending on the prominence of microbusinesses in CUs’ broader communities.

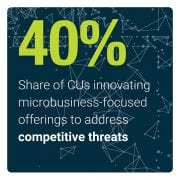

Our research shows that CUs that innovate microbusiness-focused products and services do so primarily to provide microbusiness members with faster transaction processing, with 67.3 percent citing this as their reason. We also found that 45.8 percent expressed interest in innovating microbusiness-focused products to increase their deposit volumes, and 43.9 percent are doing so already to help their microbusiness members meet their customers’ rapidly changing expectations.

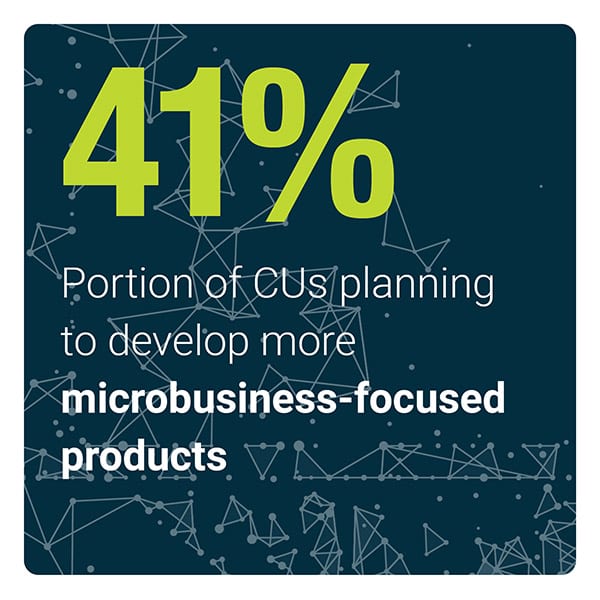

Yet not all CUs are equally invested in innovating new products and services for microbusinesses. Small CUs tend to have more microbusiness members than large CUs, and their innovation plans are often more microbusiness-focused as a result. Our study finds that 55.3 percent of CUs with less than $500 million in assets are planning to develop more microbusiness-focused innovations going forward, for example, compared to just 27.3 percent of CUs with more than $5 million in assets that plan to do the same.

microbusiness-focused innovations going forward, for example, compared to just 27.3 percent of CUs with more than $5 million in assets that plan to do the same.

So, how do CUs in these various asset classes and with different portions of their member bases made up of microbusinesses shift their innovation plans to match those bases’ vastly different needs? The Credit Union Innovation Playbook: Microbusiness Opportunity Edition explores the answer to this question and many more.

To learn more about the role of microbusinesses in driving CU innovation agendas, download the Playbook.

About The Playbook

The 2020 Credit Union Innovation Playbook series, a PYMNTS and PSCU collaboration, analyzes the evolution of the innovation trends in the financial ecosystem. The Microbusiness Opportunity Edition draws from a data sample of 3,908 consumers, 100 credit union leaders and 50 FinTech executives to examine microbusinesses’ impact on decision-makers for CUs of all sizes.

Microbusinesses are firms that either generate less than $1 million in annual revenue or are operated by a single individual. They may be small, but they represent an important part of the credit union (CU) ecosystem.

Microbusinesses are firms that either generate less than $1 million in annual revenue or are operated by a single individual. They may be small, but they represent an important part of the credit union (CU) ecosystem.