Banks, FinTechs, and others understand the benefits that item- or SKU-level data deliver.

Specifically, that greater adoption of this technology is needed, and that once its uptake accelerates, a new generation of highly relevant and actionable card-linked offers will be ushered in.

Analyzing this in the study Tapping Into The Benefits Of Item-Level Receipt Data, a PYMNTS and Banyan collaboration, we surveyed over 350 executives from financial institutions (FIs) with at least $5 billion in assets, and FinTechs with at least 1 million monthly active users (MAUs).

Per the study, 67% of high-data-readiness firms within these ranks believe consumers would be very or extremely likely to switch to institutions that provide solutions that use receipt data.

For specific solutions, such as streamlining expense management or loyalty and shopping offers, the report found that belief in SKU-level data solutions as a driver of customers changing behavior jumps to 88% and 78%, respectively for FIs and FinTechs.

Read the report: Tapping Into The Benefits Of Item-Level Receipt Data

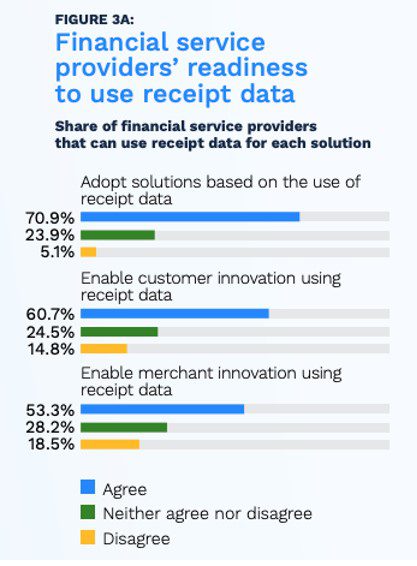

Zooming in on other key findings, the study revealed that “71% of firms have adopted solutions based on the use of receipt data, while 61% of firms enable customer innovation through receipt data and 53% enable merchant innovation.”

Data readiness matters when it comes to using SKU-level data, and the survey found that 27% of firms identifying as such can use receipt data to “adopt solutions, enable customer innovation and enable merchant innovation. FIs were more likely to cite such readiness than FinTechs, at 37% versus 23%, respectively.”

See the study: Tapping Into The Benefits Of Item-Level Receipt Data

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More