Even bleeding-edge firms face implementation issues integrating item-level receipt data into their operations.

Research in the 2023 playbook “Meeting the Need for Item-Level Receipt Data: How Integration Enables Innovation,” a PYMNTS and Banyan collaboration, found that no matter their level of data readiness, both FinTechs and traditional financial institutions (FIs) still report experiencing frictions when integrating item-level receipt data across their services.

This, as nearly three in four bank and FinTech executives surveyed by PYMNTS (72%) said they think consumers would go so far as to switch to businesses that provide solutions based on the use of receipt data.

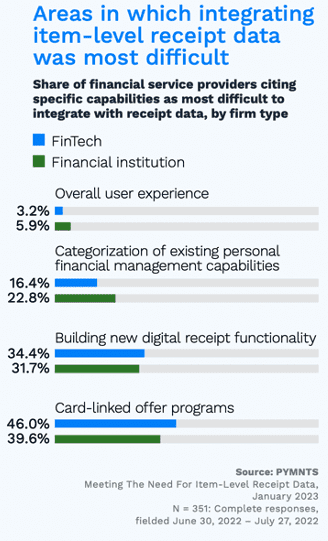

FinTechs experience more issues integrating item-level receipt data into their card-linked offer programs, while traditional FIs experience more difficulty integrating the data into the operations and processes they use to categorize personal financial management capabilities.

Even those firms already using receipt data reported finding it difficult to integrate. Among firms using receipt data, 47% considered loyalty and shopping offers the most difficult area to integrate, and 40% said tracking consumer spending behavior was the most challenging.

A key driver for firms looking to integrate item-level receipt data is the potential to attract new customers.

Leveraging the full value of item-level receipt data in a simple, secure way enables FIs, FinTechs and merchants to provide the many benefits of seamless commerce and banking experiences today’s consumers expect.

There are also many benefits for businesses. More than four in 10 firms (41%) said they already use receipt data to support most, if not all, of their operations.

Integrating item-level receipt data helps firms tailor loyalty and shopping offers with relevant, personalized rewards; as well as helps provide end-consumers a better understanding of their spending behavior.

Organizational benefits also include streamlined expense management solutions and automated solutions that handle the categorization of receipt data in expense management systems, and fraud solutions that support security teams in authorizing good transactions while offering features to remove dispute speedbumps.

To use receipt data, firms need to implement data-related capabilities.

Nearly half of firms considered data-related capabilities, such as data standardization and security, as necessary to using item-level receipt data. Newer data processing technologies, such as machine learning (ML) or artificial intelligence (AI), were only regarded as necessary by 22% of firms, yet FinTechs and high data-readiness firms were more likely to consider these technologies necessary.