This next installment of PYMNTS’ mini-series on consumer behavior popularized during the pandemic focuses on the rise of digital-only banking.

Traditional, brick-and-mortar banking through well-established financial institutions (FIs) was the standard until lockdowns and restrictions swept the globe, driving consumer adoption of online banking platforms to replace many local branch functions. After all, there was little other choice for quite some time.

However, consumers have built some trust in digital banking — enough to open the door for the institutions competing with the country’s largest FIs. As illustrated in the PYMNTS collaboration with Treasury Prime, “How Consumers Use Digital Banks,” the share of consumers using digital-only banks, including neobanks, is still small overall but growing among select demographics.

![]()

The overall share of consumers holding a checking or savings account at a neobank is still a relatively low 9%. But that portion grows to 16% of bridge millennials, 15% of millennials and around 14% for small business owners or those who are self-employed or freelancers — the gig economy.

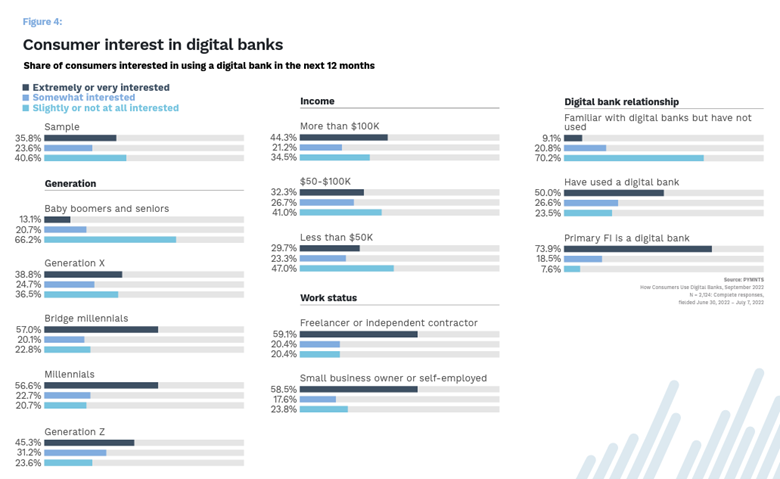

Although those shares may seem low, there is evidence that a rise is on the horizon, as the same report demonstrates that 36% of consumers are interested in using a digital-only bank in the upcoming 12 months after being surveyed.

The report further hints at the reasons for this rising interest, with 43% of consumers saying their primary reason for this interest is for improved transfers. Another 33% cited lower costs as a reason for interest, with 11% finding it the most important reason. Millennials, in particular, expressed interest in digital-only banks because they expected earlier access to the latest tech tools. Further PYMNTS research also found that consumers are beginning to trust digital-only banks, with 39% saying they are comfortable with the current security measures at their current online institution.

And in this current economic environment, offering consumers high-yield savings rates close to Apple’s while leveraging that growing trust doesn’t hurt, either.

There is no expectation, however, that digital-only banks will take over the industry anytime soon. In an interview with PYMNTS, U.K.’s Allica Bank CEO Richard Davies details the nearly sector-wide strategy that neo- and digital-only banks employ to take industry market share from more established institutions. “Our goal is to be a full-service replacement for a NatWest or Barclays, [but] we don’t expect to win the primary account from day one because there’s this view that there’s a lot of hassle around moving primary accounts. Our aim is to win a lot of secondary accounts and then use those as building blocks to win primary accounts over time… We don’t have a big consumer brand, whereas established banks advertise everywhere on TV and sponsor deals, and so by default, they [have an advantage over us].”

Some of the greatest behavioral shifts for consumers come out of a crisis. The rise of digital-only banking, with adoption and interest that is still growing, is just one example. And as detailed in other installments of our mini-series, consumers have made clear that certain conveniences and innovations arising from the pandemic’s peak are set to stay for the long haul.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More