The digital payment experience offered by the Starbucks app captured consumers’ attention when it was rolled out over a decade ago, triggering a wave of similar branded apps and services geared toward ousting cash — and eventually plastic card payments — from their treasured positions in consumers’ wallets.

More and more consumers have bypassed physical cards in favor of online or mobile-enabled alternatives at the in-store point-of-sale (POS), tapping wallets such as Apple Pay or Google Pay instead. The ongoing shift to digital-first payments grew in 2020, with the Starbucks Rewards member base expanding 10 percent from 2019 figures, for example.

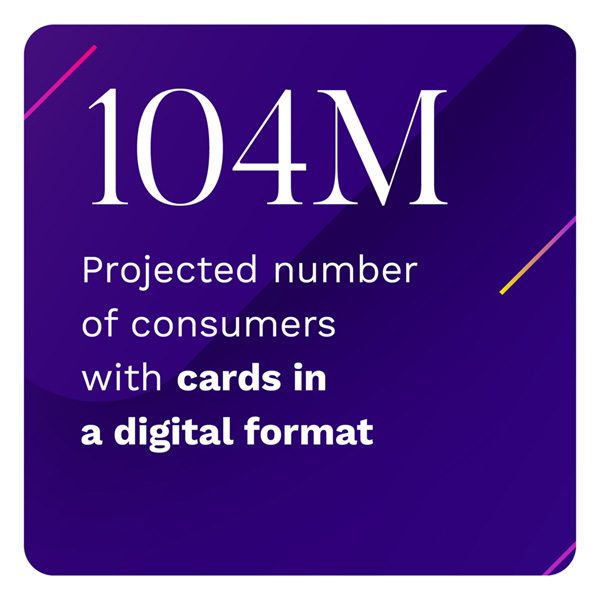

Yet the adoption of digital cards has begun to taper off from previous highs; while 41 percent of consumers stated they had virtual credit or debit cards attached to digital wallets, swiping or tapping physical plastic cards still remains the top way most consumers want to pay. PYMNTS research found that only 5 percent of consumers without digital cards stated they were either “very” or “extremely” interested in getting them. This does not mean opportunities for digital card growth are disappearing, however, but that issuers must be able to present the benefits of these cards to consumers who remain lukewarm on their advantages.

Digital Card Usage: A Path Forward, a PYMNTS and IDEMIA collaboration, takes an introspective look at the current state of digital card adoption and how issuers and other financial players could champion its growth. The report analyzes the responses of a census-balanced panel of 2,244 United States consumers regarding the key factors driving their use of digital cards, as well as the barriers that may be preventing them from doing so.

Cons umers are still intrigued by virtual cards’ potential; 11 percent reported tentative interest in signing for digital cards in the future, indicating this market is still ripe for expansion. The draw of digital cards is especially strong among millennials or lower-income consumers, with the added convenience or ease-of-use of the payment method being the top factors drawing their attention. Fifty-seven percent of millennials claimed they were attracted to the possibility of paying with digital cards in stores, for example.

umers are still intrigued by virtual cards’ potential; 11 percent reported tentative interest in signing for digital cards in the future, indicating this market is still ripe for expansion. The draw of digital cards is especially strong among millennials or lower-income consumers, with the added convenience or ease-of-use of the payment method being the top factors drawing their attention. Fifty-seven percent of millennials claimed they were attracted to the possibility of paying with digital cards in stores, for example.

The fascination with digital cards even among younger generations has not yet translated into actual use, however, and one reason why this is the case may be due to the continued dominance of plastic card acceptance, especially brick-and-mortar transactions. Seventy-percent of respondents noted they are comfortable paying in stores with plastic credit or debit cards, while notably, only 46 percent stated the same about digital wallets.

Improving comfort with digital wallets may be key to convincing more consumers to turn to their phones instead of their plastic cards when paying both in-store and online, therefore. Taking a careful look at how consumers want to pay and the factors they value out of the payment experience is also essential to the continued growth of digital card adoption.

To learn more about the state of the digital card market and how issuers can shore up adoption, download the report.