The paycheck-to-paycheck consumer won’t — and in fact, cannot — be saved by savings.

Inflation still is rampant, hovering between 8% to 9%, eating away at our collective paychecks’ purchasing power.

And since the P2P economy includes most of us — more than 60% of consumers as of last count, where there’s little left over at the end of the month after meeting basic expenses — the impact is widely and deeply felt.

It’s well-known that through the pandemic, consumers across the U.S. and across income strata managed to pad their savings, aided by stimulus checks and the fact that there was so much financial “dry powder” built up as businesses were shuttered and no one could venture outside much.

But savings are dwindling, PYMNTS’ data finds that this is not just a thought exercise: Nearly half of U.S. consumers have faced at least one unexpected expense in the last 90 days, with 56% of emergency expenses costing more than $400. In fact, consumers’ average emergency expense was approximately $1,400.

Paycheck to Paycheck is the Norm

Additionally, living paycheck to paycheck is becoming the norm, and as many consumers now live paycheck to paycheck without issues paying bills as those who do not live paycheck to paycheck. The affluent are not immune to these trends, either, as the share of high-income consumers living paycheck to paycheck has increased in the past year.

These are just some of the findings detailed in this edition of “New Reality Check: The Paycheck-To-Paycheck Report,” a PYMNTS and LendingClub collaboration. The Emergency Spending Edition examines the financial lifestyle of U.S. consumers who live paycheck to paycheck, the factors that cause financial distress and how financial stressors, such as emergency spending, impact their ability to manage expenses and put aside savings.

The series draws on insights from a survey of 4,006 U.S. consumers conducted from July 8 to July 27, as well as an analysis of other economic info and recent stats, as found in the report “New Reality Check: The Paycheck-To-Paycheck Report: The Consumer Savings Edition,” in collaboration between PYMNTS and LendingClub, show that Americans are spending more than they take in.

The survey of 3,583 U.S. consumers to gauge how inflation and volatile markets were impacting them revealed that 13% of households had spent more than they earned in the past six months.

Dig down a bit, and the situation is even more prevalent among the consumers who struggle to pay the bills. About 40% of those consumers have spent more than they have earned in the past 6 months.

There are two ways to “cover” shortfall: Utilizing credit or tapping into savings. We’re seeing evidence of the latter as savings dwindle, a trend that is crystallizing across official government stats, too.

The Bureau of Economic Analysis reported in its own most recent report that the saving rate as a percentage of personal income remained unchanged at 5% in July versus June and is down from earlier readings this year of 5.2%.

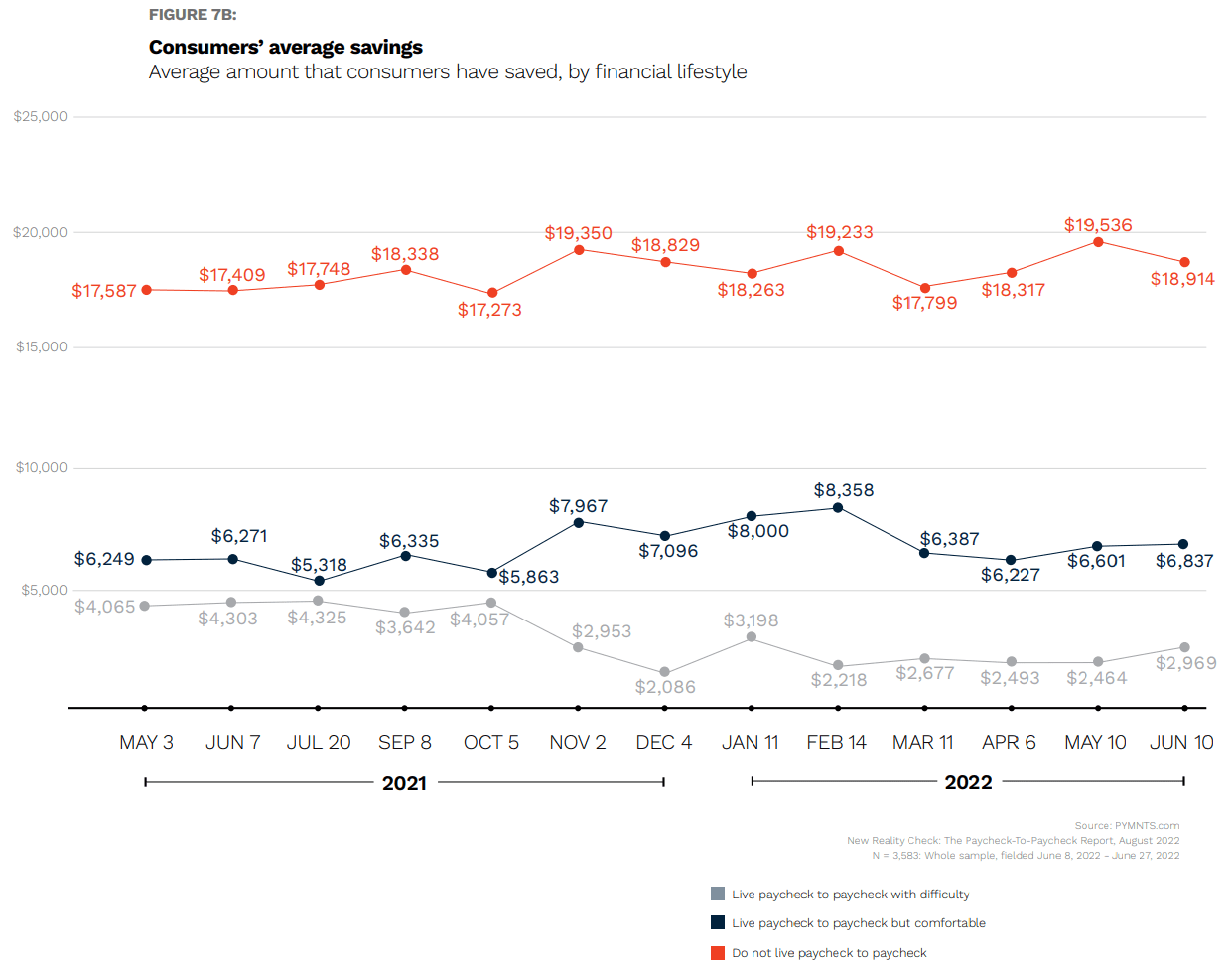

The PYMNTS data shows that the savings for people who live paycheck to paycheck but do not have issues paying their bills have dipped to a bit more than $6,800, down from more than $8,300 at the peak. The situation seems a bit ominous for the paycheck-to-paycheck consumers who are struggling with expenses, and where the average savings here stands at less than $3,000, down from more than $4,000 at the peak.

We noted in other data that paycheck-to-paycheck consumers are more likely to prioritize easy access to funds when choosing where to hold their savings, keeping an average of 70% of their money in banks, digital wallets or cash. Doing so, we contend, means they can tap those funds in a pinch as needed, rather than allocating them to long-term retirement funds or other accounts meant to keep (and grow) that money over time.

And, increasingly, emergency expenses are draining the reserves. As reported on Monday (Aug. 29), Nearly half of 4,000 U.S. consumers surveyed have faced at least one unexpected expense in the last 90 days, with 56% of emergency expenses costing more than $400. In fact, consumers’ average emergency expense was approximately $1,400. That can be a huge drain on the declining cash cushions as detailed above.

There might be at least some breathing room afforded by the recently-announced cancellation of student debt, and we wonder if taking that monthly burden off the table might give borrowers a chance to “re-pad” their savings.

In doing so, they can also leverage platforms such as on offer from LendingClub, to take on personal loans that wind up being significantly cheaper than credit card debt and automatic savings deposits that yield interest rates higher than some traditional players.