As PYMNTS has found, those obligations are among the most important to individuals and families.

But recent data from the U.S. Consumer Financial Protection Bureau show that collections on non-financial debt — even excluding medical debt, a pressing problem — remains significant.

In the paycheck-to-paycheck economy, a missed payment here and there can snowball and wind up in collections, ultimately hurting credit reports.

Data from the CFPB shows, on a headline basis, that there’s been a one-third decline in collections — at least in the number of accounts reported — from 261 million tradelines in 2018 to 175 million tradelines last year.

The data shows that most collections — nearly 75% — are for non-financial debt and low-balance amounts. The median collections balance is $382. We spotlighted earlier this week that medical collections tradelines are still a majority of all collections on consumers’ credit reports — at 57%.

Banking and financial debt is another 13.2%, followed by telecom at 10.8%, retail at 8.1% and utilities at 4%.

Not Out of the Woods

On the face of it, things are headed in the right direction. The number of tradelines for utilities was down by 47%, and telecom by 51%. But, as the CFPB cautioned, per commentary from Director Rohit Chopra: A “decline in collections tradelines does not necessarily reflect a decline in debt collection activity, nor an improvement in families’ abilities to meet their financial obligations.” The decline, he said, is tied to “a choice by debt collectors and others to report fewer collections tradelines, while still conducting other collection activities.”

In other words, the debt and missed payments are out there.

And the data show, further, that the median balance for the telecom debt stood at $390, roughly steady from 2018, and utilities saw the median balance grow by 31% through the same timeframe to $276.

And the data show, further, that the median balance for the telecom debt stood at $390, roughly steady from 2018, and utilities saw the median balance grow by 31% through the same timeframe to $276.

The relatively low balances here may hint that the paycheck-to-paycheck economy is playing a form of “roulette” with bills, making partial payments on some obligations and missing others.

The relatively low-dollar amounts for utilities and telecom and retail debt show that at least some top-of-the-list payments are being triaged.

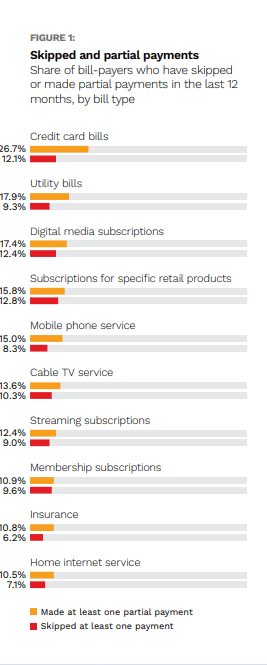

Those sentiments are corroborated by PYMNTS data show, as per the “The One-Stop Bill Pay Playbook,” a Mastercard collaboration, that more Americans are making partial bill payments or skipping some months altogether. We found that 27% of consumers surveyed “are more likely to remit partial payments” for credit card debt. But 18% are also willing to make partial/skip payments on their utility bills.

The chart from PYMNTS to the left shows that 9% have skipped at least one utility bill, 8% have skipped a mobile phone bill and 15% have made partial payments on those obligations. All income brackets have reported falling behind:

PYMNTS/Mastercard found that more than a quarter of consumers earning up to $100,000 annually have failed to make at least one payment on these bills — and nearly a quarter of high-income earners above that $100,000 threshold have done so.

There’s at least some indication of what providers/billers can do here to ensure at least some of these consumers pay on time: The report reveals that 14% of bill-payers who prioritize at least one bill over others identified the ease of making payments as a key factor in that decision-making process.