Inflation is top of mind for consumers, and is contributing to a muted outlook of where things stand — and where we are headed.

The Conference Board said in a Tuesday (Aug. 29) press release that its Consumer Confidence Index reading for August came in at 106.1, down from 114 in July. The consensus estimate had been for 116.

The survey also found that individuals’ view of current conditions fell to 144.8 from 153.

Muted Future Expectations

Perhaps among the more notable stats here: The index for future expectations was at 80.2, down from 88 in July. The Conference Board has stated that readings below 80 for future expectations tend to signal a recession in the subsequent year.

“Write-in responses showed that consumers were once again preoccupied with rising prices in general, and for groceries and gasoline in particular,” Dana Peterson, chief economist at The Conference Board, said in the press release.

The Board estimated that “the pullback in consumer confidence was evident across all age groups — and most notable among consumers with household incomes of $100,000 or more, as well as those earning less than $50,000.”

Consumers’ short-term income prospects worsened in August, too: 16.5% of consumers expect their incomes to increase, down from 17.8% in July. And another 12.4% expect their incomes will decrease, up from 9.9%.

The less than sanguine outlook, and dampened expectations about income, may spell some pressure headed into the holiday shopping season, and worries about how to grapple with credit card debt.

Already Stretched

The consumer-focused report comes against a backdrop where, as research by PYMNTS and Elan has shown, high-income consumers — those earning more than $100,000 annually — were shown to have the highest increase in credit card reliance, at 34.2%.

Overall, 33% of credit card holders across all demographic categories increased the share of their expenses paid with credit cards in the past six months, while only 15% reduced it. Younger consumers were more inclined to shift a larger portion of their expenses to credit cards, with 43% of Generation Z and millennial consumers, as well as 46% of bridge millennials, doing so.

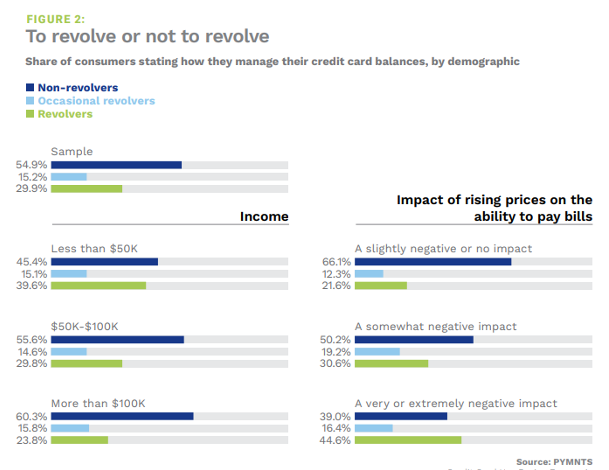

The data show that the highest and lowest-earning brackets are the ones that revolve their credit card debt most significantly — and thus they have less dry powder to spend. As seen in the accompanying chart, the impact of rising prices is decidedly negative. Our estimates show that 55% of consumers with bank-issued credit cards always, or usually, pay their card balances in full each month, while 45% — approximately 89 million consumers — carry revolving balances.

The logic follows that if consumers are at least somewhat hamstrung by their monthly obligations to meet their credit card debt payment – a recurring binary choice, where one pays it, and has less discretionary income, or doesn’t pay it, and suffers an adverse credit event — and are less optimistic about income to offset that obligation … well, spending will be curtailed as a result.