Nearly 200 million in the United States hold at least one bank-issued credit card — a financial tool which has come in handy as inflation and higher costs continue to squeeze households in a challenging macroeconomic environment.

In the recent “Credit Card Use During Economic Turbulence” report, PYMNTS leverages insights gathered from a survey of over 2,200 U.S. consumers to identify patterns related to the spike in credit card usage and key drivers for choosing certain card features, with an emphasis on how higher inflation has influenced this behavior.

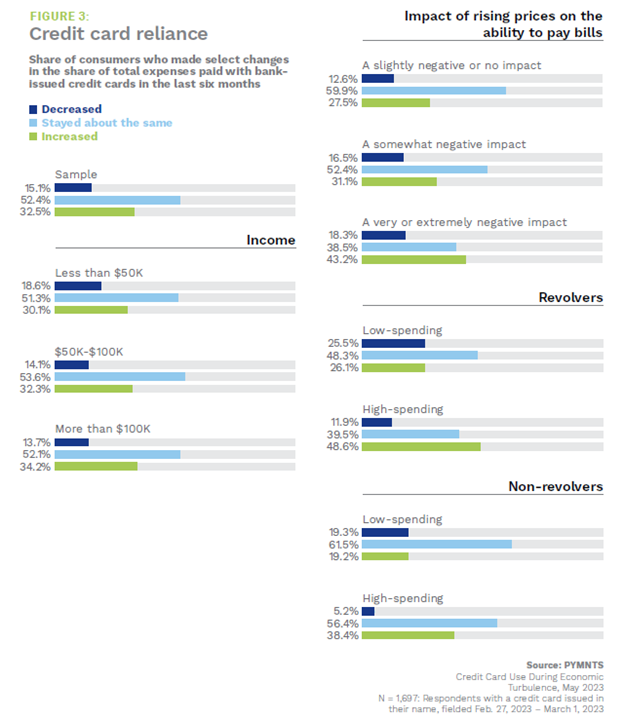

Findings captured in the joint PYMNTS-Elan Credit Card study show that individuals with credit cards are utilizing them more extensively in response to the heightened inflationary environment. In fact, the more severe the inflation, the more consumers rely on credit cards for expenses.

“While 28% of respondents who reported experiencing just a slightly negative or no impact from inflation increased their spending by credit card, 43% of those who reported experiencing a very or extremely negative impact did so,” the report stated.

Overall, 33% of credit card holders across all demographic categories increased the share of their expenses paid with credit cards in the past six months, while only 15% reduced it.

Leading this surge in credit card dependence are high-spending revolvers — consumers who pay more than 40% of their total expenses by credit card and who always or usually carry a revolving balance between statements, per the report. Of that group, nearly half increased the share of expenses allocated to credit cards in the last six months.

Drilling down into the data further reveals that younger consumers were more inclined to shift a larger portion of their expenses to credit cards, with 43% of Generation Z and millennial consumers, as well as 46% of bridge millennials, adopting this trend.

In contrast, the study found minimal differences across income brackets, with consumers earning less than $50,000, between $50,000 and $100,000 and more than $100,000 all increasing their credit card usage by about 32% on average.

Nonetheless, high-income consumers were the ones shown to have the highest increase in credit card reliance, at 34.2%.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More