The worst is over for inflation, and the impact of rising prices will recede.

Not by a long shot.

The long-term perspective tells us otherwise.

The latest Consumer Price Index report from the Bureau of Labor Statistics shows that inflation’s growth rate fell for the sixth straight month. The latest reading of 6.5% growth is a marked downshift from the peak of more than 9% growth seen earlier this year.

On a monthly basis, the BLS said the overall prices were little changed, falling 0.1% in December after rising by the same amount in November.

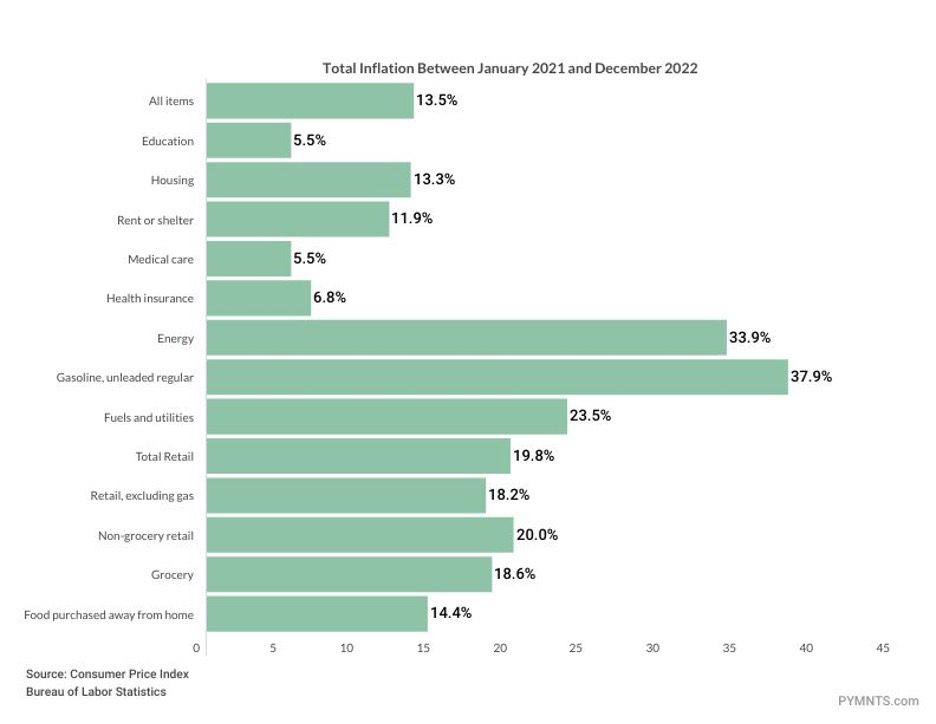

To be sure, the fact that inflation is trending lower is welcome news. But PYMNTS’ proprietary analysis of the BLS data shows that, when viewed across a longer time frame, the month-to-month ebbs and flows and year-over-year comps pale in comparison to how much more expensive life has become since the beginning of 2021. At a high level, the most essential goods and services that we use on a daily basis — even excluding volatile energy prices — are up double-digit percentages over that time frame.

And deflation’s not in the cards, which means we’re not getting back to the “good old days” of January 2021’s affordability anytime soon. We’re being a bit tongue in cheek about that “good old” moniker — of course, two years ago, the world was trying to claw its way out of the grip of a raging pandemic. But viewed through the lens of today, a gallon of milk was quite a bit cheaper, so was medical care and so was a shirt.

The headline number gleaned from the chart below shows that our “basket” of goods and services is 13.5% more expensive than it was two years ago. With a bit more granular insight, non-gas and non-grocery retail items are 20% more expensive. Groceries are 18.6% more expensive. Health insurance and medical care are up single digits.

The paychecks on which we all rely are not keeping pace with inflation, which means that there’s less money to go around, and to counter the price increases that, as shown above, have been relentless. The report, “The New Reality Check, The Paycheck-to-Paycheck Report: The Employment Edition,” shows a meager 15% of consumer wages are not keeping up with inflation. Just 1 in 10 consumers have said their incomes are growing at least on pace with inflation, which implies that, really, none of us are getting ahead. Only 4% said their wages increased more than inflation, which would imply at least some additional purchasing power .

This analysis dovetails with recent PYMNTS reports that consumers are not feeling that the pressures of inflation are abating. As noted in this space and in the recent report “Consumer Inflation Sentiment: Perception Is Reality,” the thousands of consumers we queried said prices have increased “significantly.” And past seems to be prologue, at least when it comes to expectations: These same consumers think inflation will remain inflated (sorry for the pun) through at least the next year and a half.

The aforementioned grocery price hikes have had a significant impact on how we shop. We’ve found that almost 60% of grocery shoppers have dialed back on their grocery purchases and about 11% have opted to purchase lower quality items to keep food on the table.

We note that the same inflation that bedevils consumers also is hurting the Main Street businesses that power employment and wages. As has been detailed in the latest Main Street reports, nearly two-thirds of firms raised prices in their own response to inflationary pressures. But, looking ahead into 2023, 40% of firms say that inflation is their biggest challenge.

In the short term, the government data may signal that the worst is over. Over the long term, inflation’s damage has already been done, has been widespread, and there may be no going back to the affordability of daily life seen just two years ago.