Inflation’s been the main concern for merchants and consumers through the past few years.

But as PYMNTS Intelligence data shows, inflation’s impact on retail, in real terms, is ebbing.

Now, many other factors may wind up dampening the enthusiasm to open one’s wallet: Worries over employment, war, politics … and where inflation’s headed.

And it’s still the case that, as we’ve found in past reports, that the majority of consumers feel that their incomes have not kept pace with inflation.

Should those feelings linger, or deepen, so too will the headwinds to keeping up the spending pace.

For now, at least, it seems like the inexorable rise in prices is not serving as an impediment to filling baskets online and in-store. The coast isn’t clear for merchants, not by a long shot, but there may be glimmers of hope.

It may come as no surprise that December sales data released Wednesday (Jan. 17) came in strong, given the fact that the month includes the holidays. The headline numbers show that retail sales were up 0.6% overall for the month, building on November’s 0.3% gains.

Of the more than one dozen categories tracked by the government, most segments gained, with the exception of sales at furniture stores, at electronics stores, and health and personal care retailers. But as measured year on year, sales at food and drinking establishments were up more than 11%, electronics stores were ahead by more than 10% and spending at health and personal care stores were up by 10.7%. When viewing the data (which are not adjusted for inflation), the overall retails sales month over month jumps to 8%.

Wall Street, as usual, has been seesawing on sentiment about the Federal Reserve, and whether rate cuts will be in the offing sooner rather than later. Wednesday saw the markets drift lower.

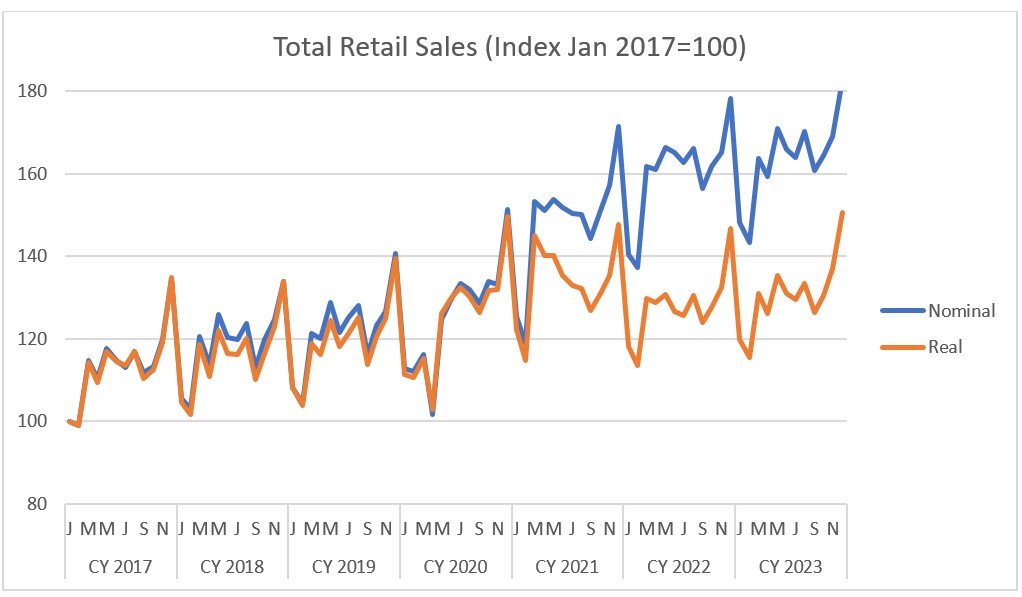

In gauging the overall health of the consumer and whether spending momentum remains — and can remain — intact, it is the long term picture that matters.

And as seen in the chart below, the real spending, adjusted for inflation, is spiking upward, tracking the headline or nominal trend. In other words, the read across is that, by and large, consumers are buying more — more goods, more gifts, more food, more clothes … name the category and the demand is there. In fact, PYMNTS has found that seasonally adjusted sales from 2022 to 2023 increased by 2.1%.

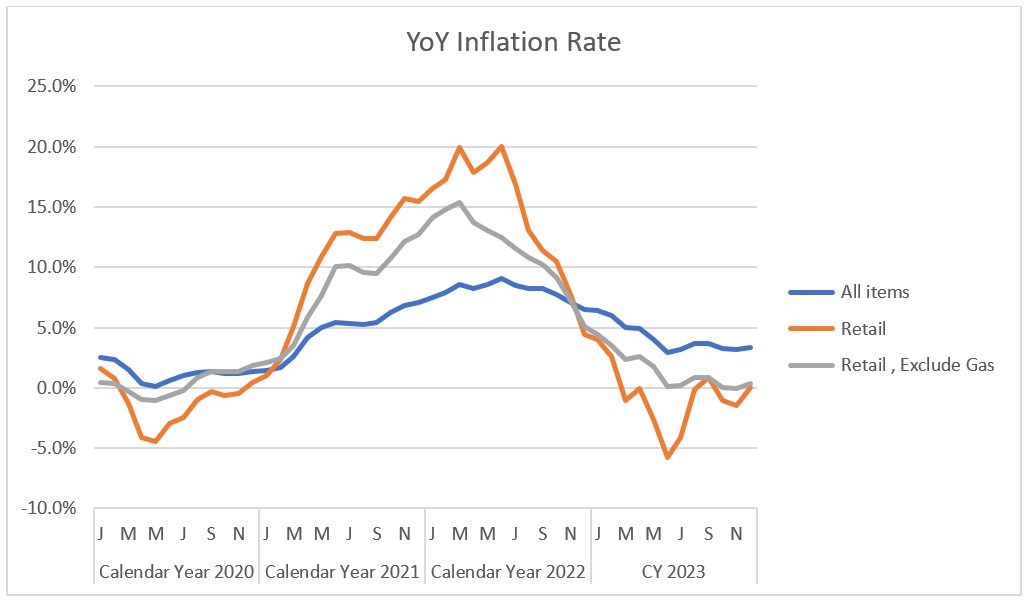

Part of the reason for the surge — and the narrowing of the gap between real and nominal sales — lies with the fact that inflation for retail items (not overall) has been near 0%, though volatility reigns.

We caution that a few months of data points do not a trend make. December’s bounce may give way to at least some retrenchment in January, as consumers take stock of the household budgets. For those consumers who loaded up on debt to finance their purchases, the paydown of the increased obligations may be pressing. But then again, separate PYMNTS research shows that buy now, pay later (BNPL), and paying over time gathered a larger slice of wallet share through the holiday shopping season.

Bank earnings to date, and as spotlighted in our own earnings coverage, has showed debit spend up in the mid to high single digits, pacing credit card spending, and management commentary has said that delinquencies are normalizing rather than alarming.

January’s just underway, and there are no guarantees of what lies ahead, but if December’s any indication, merchants may see some brighter days ahead.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More