Personalized assistance could help the credit marginalized from slipping further behind.

Having good credit is a near necessity for U.S. consumers. Maintaining a good score matters in facets of daily life ranging from rental applications and automobile purchases to mortgage loans. However, for the 25% of U.S. consumers who are credit marginalized — consumers who have been turned down for one or more credit products over the last 12 months — those facets may be increasingly difficult to reach.

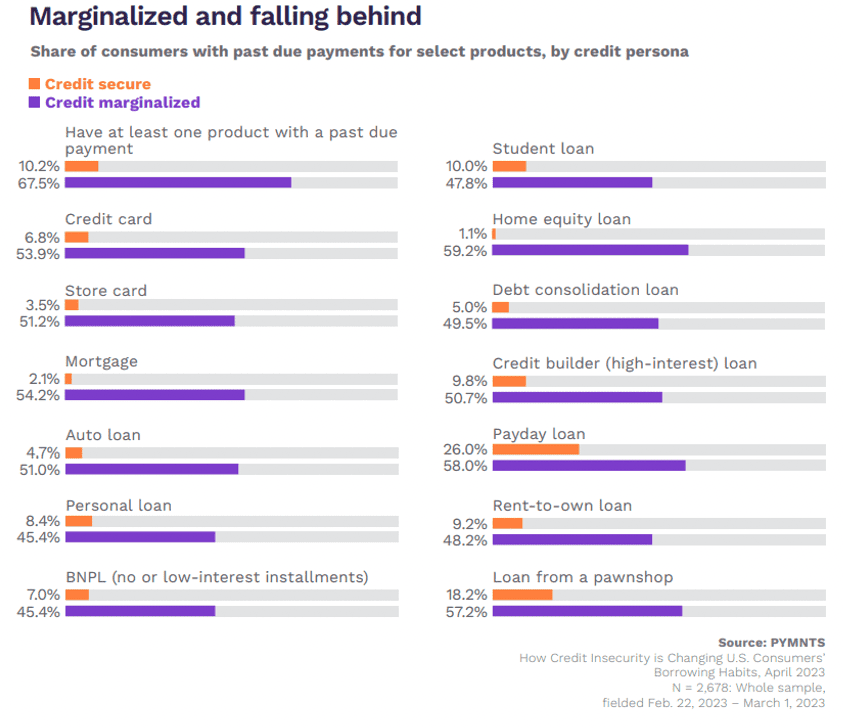

And, as detailed in PYMNTS’ collaboration with Sezzle, “How Credit Insecurity Is Changing U.S. Consumers’ Borrowing Habits,” the credit marginalized are having trouble keeping up with repaying the credit that has already been extended.

In 10 of the 14 select products, the share of credit-marginalized consumers with past due payments is over 50%, and in no category is the share below 45%. Credit marginalized consumers represent approximately 63.5 million individuals in total, and PYMNTS data shows that nearly 43 million of them are past due on at least one credit product.

This large pool of credit marginalized consumers, who may also fall under the broader category of underbanked, may benefit from assistance when it comes to credit products. As previous PYMNTS research has found, customers are actively seeking education and tools to manage debt. This could offer an opportunity for financial institutions and FinTechs to leverage the trust they have built with their customers to provide tools and education that promote financial literacy — and deepen customer loyalty as a result.

Orland Zayas, CEO of lease-to-own provider Katapult, detailed the business opportunity that organizations have to reach the credit marginalized and underbanked in an interview with PYMNTS. One strategy he touched on includes getting them banked by offering a zero-fee debit card checking account to start, and then helping them access additional accounts and financial products.

“I think using that strategy … will get [these customers] to graduate, if you will, up the spectrum to banked, and then fully banked and good credit,” he said.

Financial institutions’ goal in pursuing this strategy should be “to build [up] that customer, build their confidence in how they manage their finances and how they manage their credit so that they can continue to succeed and get the items that they need, and they don’t run into emergency situations.”

For the credit marginalized, daily tasks may be anything but ordinary when faced with rejection for products and services deemed all but essential to everyday life. Banks and FinTechs that can successfully leverage the need for financial literacy tools and education may find themselves both expanding their customer base and bettering their customers’ financial lives.