Financial institutions have an opportunity to provide customers with the financial literacy tools they want.

January is Financial Wellness Month, and as inflation continues to stretch most household budgets, consumers are seeking better ways to manage their funds.

With only 4% of Americans able to demonstrate financial literacy, the need is more urgent than ever. This financial gap presents an opportunity for banks and credit unions to increase their customer loyalty by offering budgeting tools and financial guidance.

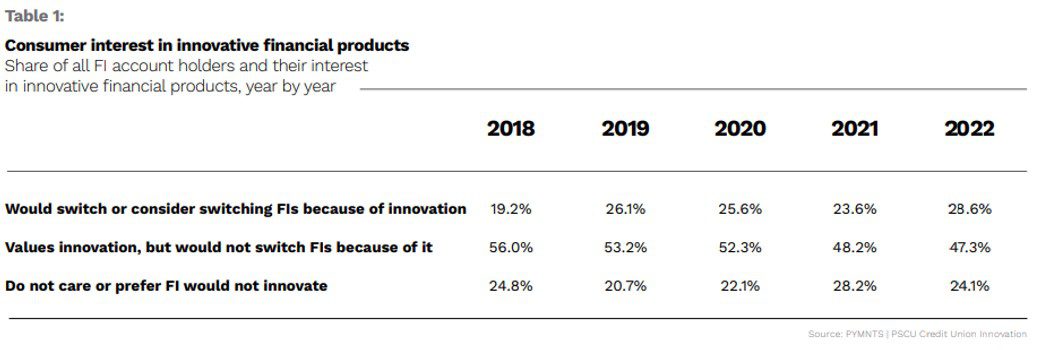

Technology is playing an increasingly large role in promoting financial inclusion among bank customers in the U.S., leading to a growing demand for personalized banking experiences to help them pursue their financial goals, such as budgeting tools. And, per PYMNTS’ long-running research into consumer interest in financial innovations, customers are willing to switch institutions if this need isn’t met.

Banks and other financial institutions looking to roll out personalized financial tools could consider cost-cutting solutions like the one offered by the neobank Bunq, which allows European users to allocate money into separate budget categories. Bunq then automatically determines to which budget a given payment belongs and assigns funds from the correct sub-account. Additionally, the FinTech Moneyhub allows retirees to view and manage all their pensions in one central dashboard.

Financial education can also take a hybrid path.

In an interview with PYMNTS, Robert Cashman, president and CEO of Metro Credit Union, describes how education is an important component of how Metro helps its members. Cashman said the credit union offers an abundance of seminars, trainings and online resource materials to guide members through challenging times.

This educational content is designed to be useful for members of all ages and life stages, whether they are recent graduates just learning to budget and save, or older people planning for retirement. He added, “We even have resources for children, so our kids have early access to the tools they need to be informed and confident as adults.”

Social media is another untapped opportunity, as people search beyond traditional outlets for financial advice – especially younger customers, who are willing to turn to alternative sources. Banks that hesitate to innovate these sorts of offerings may risk alienating these social media-savvy consumers.

Keeping pace with shifting customer expectations is a perennial challenge across the financial services industry. However, a little help can go a long way. By offering tools that foster financial literacy and empowerment, banks can gain the long-term loyalty of digital-minded consumers.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More