They have different business models — but often compete for the same customers.

And for banks and neobanks, there may be one commonality:

The challenge of pushing back against the rising tide of fraud, both here in the U.S. and across the pond in the U.K.

Neobanks, of course, are digital-only players in financial services. Traditional banks have a hybrid model, tied to physical branches and online banking channels. We’ve noted in recent coverage that, as shown in earnings season, the banks themselves are seeing a continued pivot to digital means of getting all manner of banking activity done. Mobile phones and other devices may offer freedom and flexibility in how individuals interact with providers. But the anonymous nature of those transactions, account openings and P2P fund flows opens the door for fraudsters to probe vulnerabilities.

The magnitude of the issue is detailed in joint efforts between PYMNTS Intelligence and Hawk.AI, in the report “The State of Fraud and Financial Crime in the U.S.”

The responses from 200 executives queried were eye-opening. As many as 43% of financial institutions (FIs) have experienced increased fraud in the past year. The average cost of fraud for FIs with assets of $5 billion or more also increased by 65%, from $2.3 million in 2022 to $3.8 million in 2023.

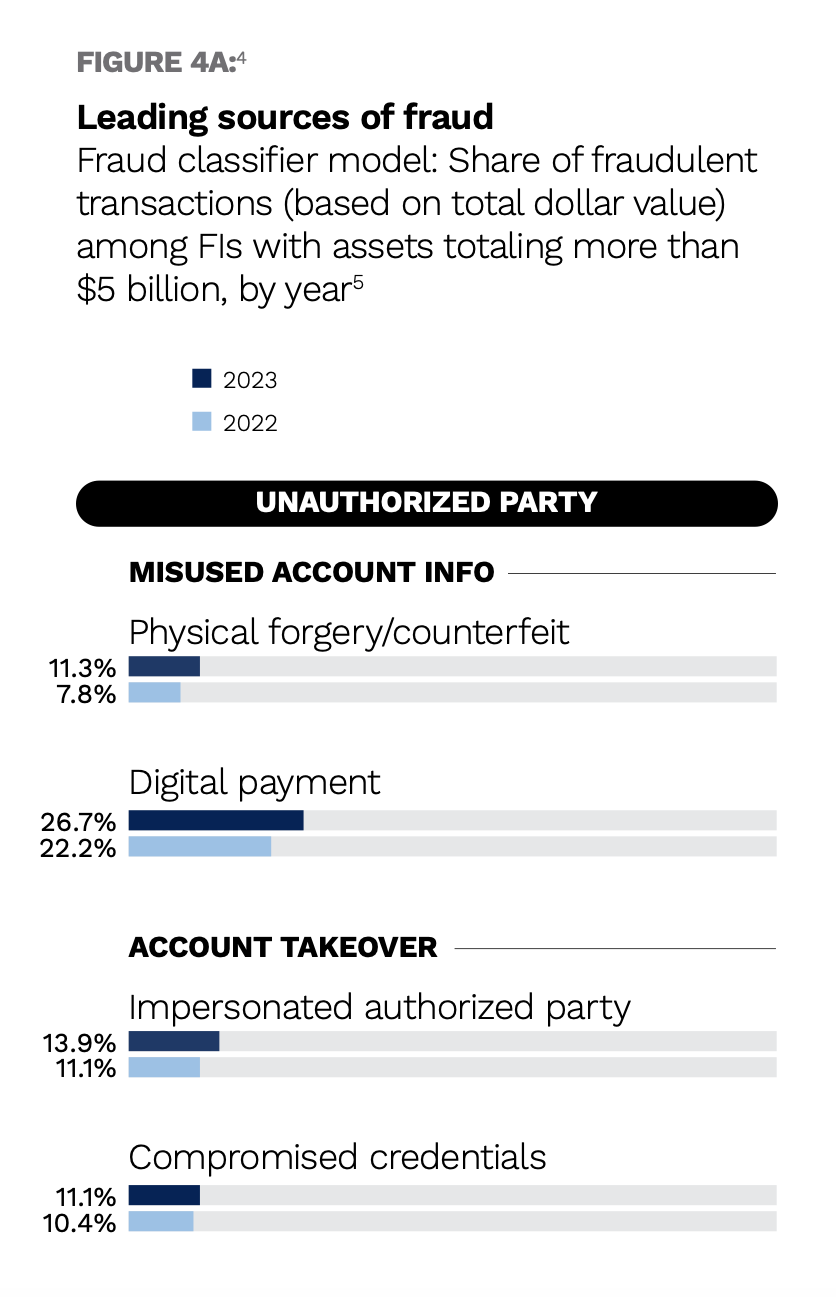

And digging into the details, the data show that 12% of fraudulent transactions can be traced to scams, with bank tech support impersonation and IRS scams most common. The popularity of those “outside” party schemes among bad actors is corroborated by the Federal Reserve’s Fraud Classifier Model.

The rates of unauthorized fraud surpass authorized fraud, as we note that 63% of fraudulent transactions stemmed from unauthorized party fraud, as external actors took over credentials and compromised accounts. The accompanying chart notes the specific impact and approaches the fraudsters take once they’ve compromised credentials.

In building defenses against the plethora of attack vectors, the share of FIs with assets totaling more than $5 billion that mention data breaches and the increased speed of payments as their top challenges rose significantly in 2023 compared to 2022. In 2023, 16% of FIs cited cyberattacks and data breaches as a top challenge, doubling the 7.7% share that pointed to those issues last year.

In the U.K., long a bastion for faster payments and for P2P transactions, authorized push payments fraud continues to bear watching and gives food for thought as real-time transactions, via the FedNow® Service, become more prevalent in the United States.

This week, the U.K.’s Payment Systems Regulator noted that authorized push payments fraud — centered around criminals posing as payees to trick someone into sending them money — cost consumers north of $600 million per year and accounts for 40% of scams. Neobanks are among the most prevalent targets for APP fraud, including Monzo Bank.

It’s no surprise, then, that advanced technologies are being used (and are planned for more use), with artificial intelligence (AI) and machine learning (ML), to shore up defenses. The research by PYMNTS Intelligence and Hawk.AI found that 66% of FIs with more than $5 billion in assets use ML and AI, exceeding the 44% of smaller FIs that do the same.

The improvements are tangible: FIs using ML or AI also report lower rates of the two most common scams: 22% of FIs not using these technologies experienced bank tech-support impersonation scams, but just 18% of those using these ML or AI faced the same scams. And for the banks leveraging AI and ML, 20% of FIs using those tools encountered those attacks, better than the 24% of FIs not using those tools.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More