Medical debt and payments plans are increasingly scrutinized by the Consumer Financial Protection Bureau, the White House and regulators. But the data shows that consumers want those options when it comes time to ensure they get the care they need.

To that end, the CFPB is scheduled to host a hearing Tuesday (July 11) on medical debt and various payment options, with attendance from White House, Treasury Department and U.S. Department of Health and Human Services officials.

The hearing will feature testimony from CFPB Director Rohit Chopra, and we note that the tone may be set a bit by the heading of the announcement heralding the meeting itself, where the agencies stated the hearing will be an “Inquiry into Costly Credit Cards and Loans Pushed on Patients for Health Care Costs.”

At a high level, the hearing comes against the backdrop where the CFPB had said in its regulatory agenda — which give a look ahead as to what’s in focus — that credit reporting and collections will be on the list, so to speak.

The hearing announcement states that, amid a request for public input, medical payment products “were once used primarily” to pay for procedures and care that had not been covered by insurance (such as elective procedures). But more recently, payment options have been embraced to cover everything from emergency room visits to a broader range of everyday — and critical — procedures.

“Financial firms are partnering with healthcare players to push products that can drive patients deep into debt,” Chopra said. “We are opening a public inquiry to better understand how these practices are affecting patients in our country.”

The hearing and the request for input may set up some fireworks and may set the stage for providers and payments firms to gird against a volley of criticism. The CFPB said that the mean medical debt held by individual consumers at the beginning of 2018 was $615 — and it’s risen 30% to $802 as of the beginning of 2022.

But drilling down a bit, the rise of medical debt underscores the pressure that confronts both providers and their patients. Out-of-pocket costs are high for patients, yes, but the healthcare plans themselves have become expensive for employers to underwrite, which means that “gaps” in coverage are what winds up getting put on those plans.

Patients, increasingly, want a way to get the care they need as they put off many procedures through the pandemic. And inflation, though cooling, is still stubbornly high in an age where more health care is tied to out-of-pocket costs and seemingly ever-rising deductibles. If the CFPB winds up cracking down wholesale on attempts to inject some innovation into healthcare financing, it may inadvertently wind up curtailing at least some of the “snapback” in medical care — in effect, placing at least some restrictions on who gets the care and when, and where.

For the providers, the agreed-upon financing, via cards or installments, represents a way to collect on services rendered — and avoid chasing after unpaid bills, which top $140 billion in healthcare.

The availability of financing such as installment payments addresses an industry that, as PYMNTS has found, has all manner of friction when it comes to paying for care. More than half of consumers have said that they’ve experienced “pain points” when paying for health care expenses.

PYMNTS research, in the report “The Digital Platform Promise: How Patients Want to Streamline Healthcare Payments,” shows that 57% of patients see fast and easy payments as an important part of their healthcare experiences — which in turn may go a long way towards cementing provider loyalty, especially for the smaller providers (think: mom and pop dentists) that might lose business to competitors if they don’t at least some payment options.

Elsewhere, we found that 19% of paycheck-to-paycheck consumers who have issues paying bills and setting up a payment plan are very or extremely likely to switch healthcare providers for a better payments experience. We’ve found that 70% of consumers want a unified digital platform — a portal that gives users detailed information about their health insurance benefits, and 72% said they’d like to use the portal to access financing options.

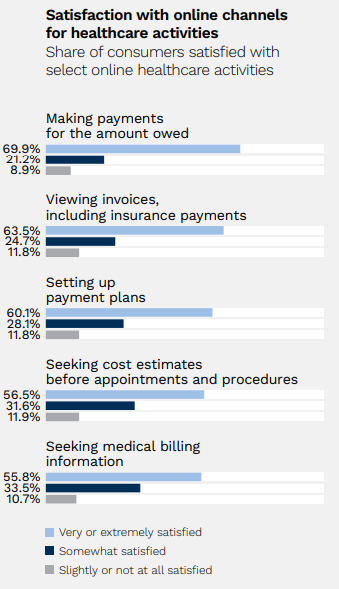

As seen in the chart below, the vast majority of consumers said that online conduits offer a satisfactory way to set up payment plans — and get estimates on costs before committing to appointments and procedures.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More