I’ve counted at least 15 companies whose primary value proposition is converting a corporation’s payables to settlement via virtual cards, rather than check or ACH. Many of these companies offer other services (e.g., e-invoicing), but it is clear they make their real money on the interchange associated with these transactions.

Some of these companies target large enterprises generally and some specialize in verticals ranging from health care to entertainment to higher education. Together, these companies represent an entire emerging sub-industry in B2B payments.

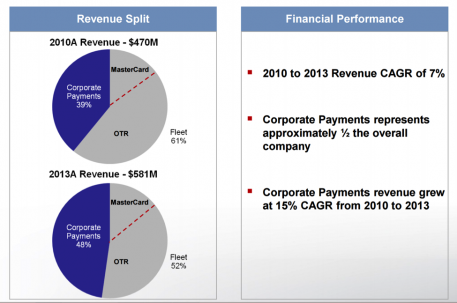

These virtual card-based settlement companies are succeeding. WEX, a major backer of these enterprises, has an “Other Payments” segment which includes the use of virtual cards in health care, travel, and corporate payables. WEX reports that this segment has been growing at an eye-popping 40 percent+ CAGR since 2010. Another major player in the industry, Comdata, was acquired by Fleetcor in late 2014, in part because of their virtual card payments business. Fleetcor noted this business had been growing at 15 percent since 2010—more than twice the growth rate of the core business. (See chart below from a Fleetcor’s investor presentation on Comdata).

Source: Fleetcor Investor Presentation

Why is this such a growth business? It’s the interchange, stupid. A payments provider that converts a large enterprise’s suppliers to accept virtual card payments splits roughly 250 bps in fees three ways: between the issuer/processor, the enterprise buyer, and themselves. That is a great payoff for changing a check to an electronic payment.

In these deals, typically 100+basis points are everted to the buyer in the form of “dividend,” “rebates,” or “incentives.” It is a great deal for everyone involved in the transaction, except the supplier. As a result, you will hear the vendors talk about the importance of “supplier education,” “supplier enablement,” and “supplier acceptance.” What they mean is: “we have to convince as many suppliers as possible to accept a rather expensive payment mechanism.” I suspect there is some subtle arm-twisting involved.

To be fair, suppliers have been notoriously slow to change from paper check to any form of electronic payment. (We all know checks are still more than 55 percent of all B2B payments.) Suppliers do trust and recognize the brands associated with virtual cards, so there is some attraction to virtual card settlement–still 2.5 percent is quite a fee to pay. The existence of 100+ bps rebates to buyers is prima facie evidence of a deal that is better for buyers. (Suppliers are typically not told much about the rebate, of course.)

In the end, it’s not exactly clear how many suppliers accept this form of payment. V-card settlement vendors claim 40 percent-75 percent acceptance rates and compete on the basis of how many suppliers they can get to agree. They all claim suppliers are much more accepting that one would think. This may be true, but it’s easy to say that a company like NBC accepts cards—they certainly do in their store in Rockefeller Center. It’s another matter to suggest they want to on invoices sent to Procter & Gamble.

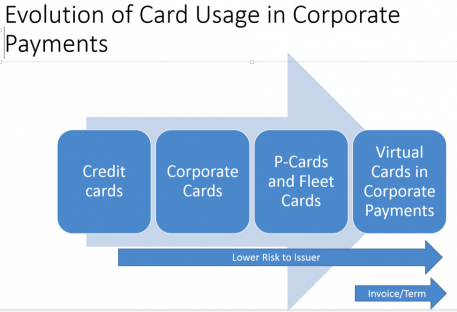

The typical interchange associated with cards fees made sense in a world where consumers were the credit risk for issuers and suppliers were getting paid almost immediately. Unfortunately, the interchange business model stayed largely the same, while cards morphed into corporate cards, procurement cards (P-Cards) in the early ’90s and now to virtual cards in corporate payments. The business model does not fit the use case nearly as well as it used to.

P-cards (either physical or more likely “ghosted” cards) have been a phenomenal success. These products ushered in the world of substantial buyer rebates, but they still made sense for suppliers. The supplier value proposition was clear:

-pay on ship/authorization

-no need to produce an invoice and wait until term

-typically used on transactions on small dollar transactions (less than $5,000)

Source: Visa

In the early 2000s, virtual cards, also known as “one-time use cards” or “controlled payment numbers,” were a great security innovation, especially in the consumer and online shopping world. (Users did not have to worry about a card or number being stolen, as the virtual card numbers were only good for one, very specific, transaction.) This same feature has been attractive to buyers and suppliers for corporate payments.

Starting in the late 2000s, with much credit (no pun intended) to the folks at MasterCard, the use of the virtual card in settling corporate invoices came to the fore. In this type of transaction, however, several of the value proposition for suppliers have long since been forgotten. In particular, suppliers now have to produce an invoice and wait until the end of the payment term to get paid at a similar, if not identical, interchange rate!

Many observers would say the use case no longer makes sense for both parties. But it must still work based on the growth levels cited above. Suppliers accept this form of payment for a variety of reasons:

-Suppliers (or the person making the decision) does not understand the cost implications

-Suppliers only do small volumes of business with the buyer, so the percentage fee is not material to their business

-Suppliers feel pressured by the vendor or buyer to participate

-The payment provider wraps additional services (e.g, remittance, interchange reductions, earlier payment, etc.) that suppliers feel justifies the fee

-Suppliers have already factored the fee into their prices

The finance world is very efficient at allocating capital to attractive risk/reward opportunities. Many of the dynamic discount, supply chain finance, and receivables financing vendors see the mismatch between the interchange model and corporate payments as an opportunity to be exploited—or at least a way to address the percentage of spend that will never make it onto virtual cards due to the price of interchange.

These numerous providers have an uphill battle in that their brands are not as well recognized as Visa’s or MasterCard’s, but they have a more flexible business model and they can offer better “win-win” solutions for buyers and suppliers.

Some buyers can find alternative (non-card) ways to pay electronically and improve working capital. These would be buyers who:

• are not addicted to high rebates,

• want to address a broader base of suppliers, or

• recognize that they may be simply paying these interchange fees in other ways (e.g., higher prices)

Suppliers can improve their DSOs at lower rates more closely related to the risk and interest rate environment, rather than subsidizing rebates. These providers are also growing very rapidly and attracting a lot of capital. The battle is on.

The two approaches are not mutually exclusive, but right now they tend to be offered by different vendors. Over time, each will find their place and interchange on virtual payments may be forced to adapt more than it has already.

Bob Solomon

CEO, Software Platform Consulting

Bob Solomon is the principal of Software Platform Consulting, Inc. (SPCI). Bob helps clients develop networks and platforms that offer value to all industry participants, including their owners. Prior to founding SPCI, Bob was President of ServiceChannel, a SaaS platform in the facilities management industry. During Bob’s tenure, ServiceChannel nearly doubled in size, instituted a new business model, and dramatically improved profitability. Prior to ServiceChannel, Bob was Senior Vice President, Network and Financial Solutions for Ariba, Inc. (now part of SAP). Reporting to Ariba’s CEO, Bob was responsible for monetization of the Ariba Network, Ariba’s cloud platform for connecting Global 2000 customers to their supply bases. Bob’s team helped make the Ariba Network Ariba’s fastest growing and most profitable business.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More