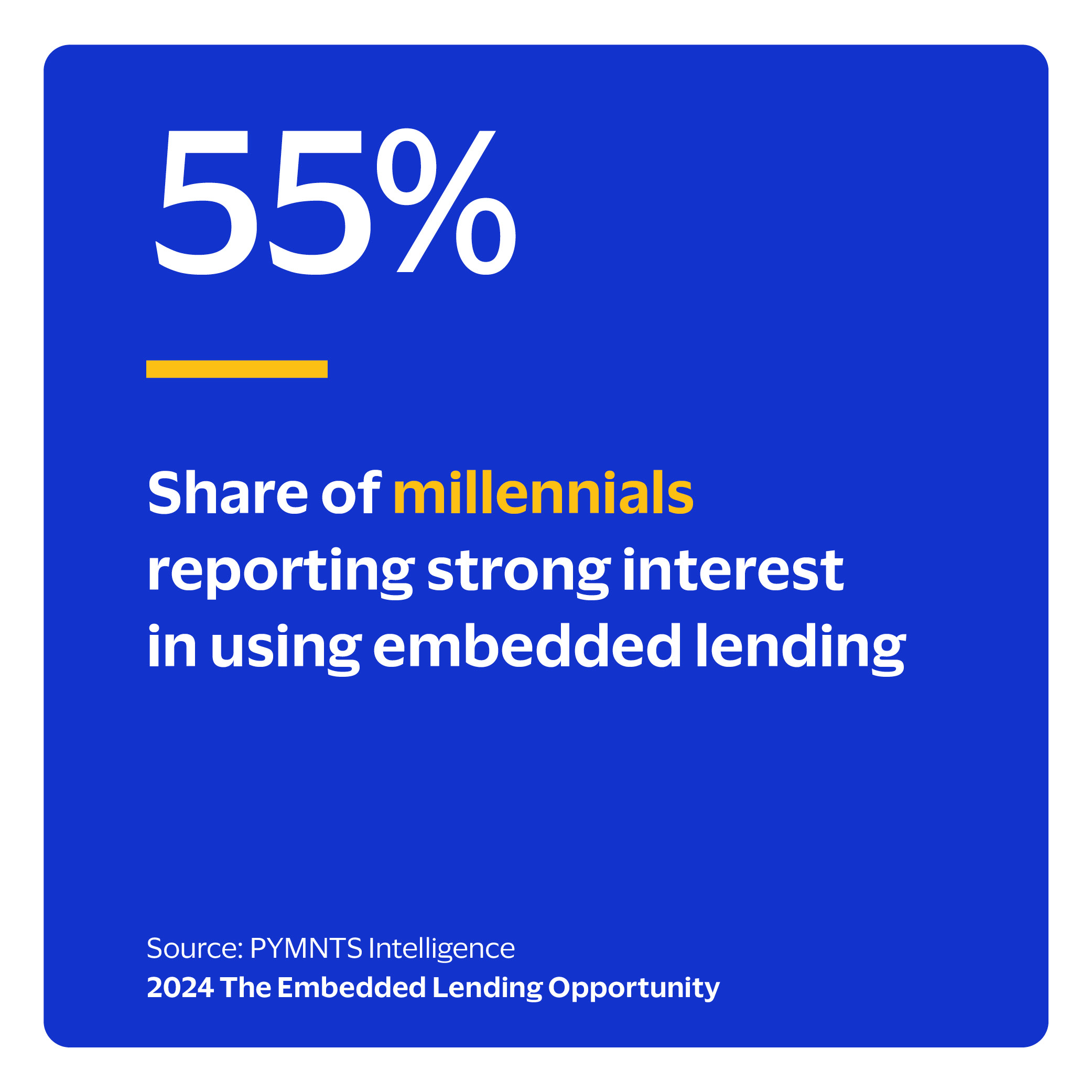

Lenders in key global markets offer an ever-increasing range of consumer credit products. Still, consumers express dissatisfaction with the current options. Just 50% of consumers across six major economies are highly satisfied, with rates in Australia and Japan particularly low. While younger individuals tend to be more satisfied than their older peers, just 60% of millennials, the age group with the greatest satisfaction levels, are highly satisfied. The availability of embedded lending represents a key area where providers appear to be missing the mark.

This data clearly illustrates the unfulfilled demand for credit across key markets — and an opportunity for embedded lending providers. These products can fill gaps in credit availability and reach new market segments by providing consumers with additional financing options. These include buy now, pay later services or instant credit card offers that they can use instantly at checkout.

These are just some of the findings in “The Embedded Lending Opportunity,” a PYMNTS Intelligence report commissioned by Visa. This report explores the state of play for embedded lending and consumer preferences about financing options. It draws on insights from a survey of 8,326 consumers across six major economies: Australia, Germany, India, Japan, the United Kingdom and the United States. The survey was conducted from Jan. 22 to Feb. 13.

Other findings from the report include the following:

Other findings from the report include the following:

Many more consumers express interest in embedded lending than currently use it.

Consumer interest in these lending options is high. Forty-three percent of consumers show high interest in switching to a provider offering these options. At the same time, just 15% of respondents used an embedded lending product in the last 90 days. Younger consumers and those reporting tight financial situations were the most interested in switching to providers offering embedded lending options.

Cash flow availability drives embedded lending use.

Consumers experiencing ongoing cash flow issues are much more likely to have used embedded lending in the last three months than those with more stable financial situations. Fourteen percent of respondents with ongoing cash flow strain used these lending options to pay for groceries. On the other hand, just 2.3% of those without such pressure did so. The data shows a similar pattern across several types of expenses.

Consumers experiencing ongoing cash flow issues are much more likely to have used embedded lending in the last three months than those with more stable financial situations. Fourteen percent of respondents with ongoing cash flow strain used these lending options to pay for groceries. On the other hand, just 2.3% of those without such pressure did so. The data shows a similar pattern across several types of expenses.

Consumers want these options for many reasons.

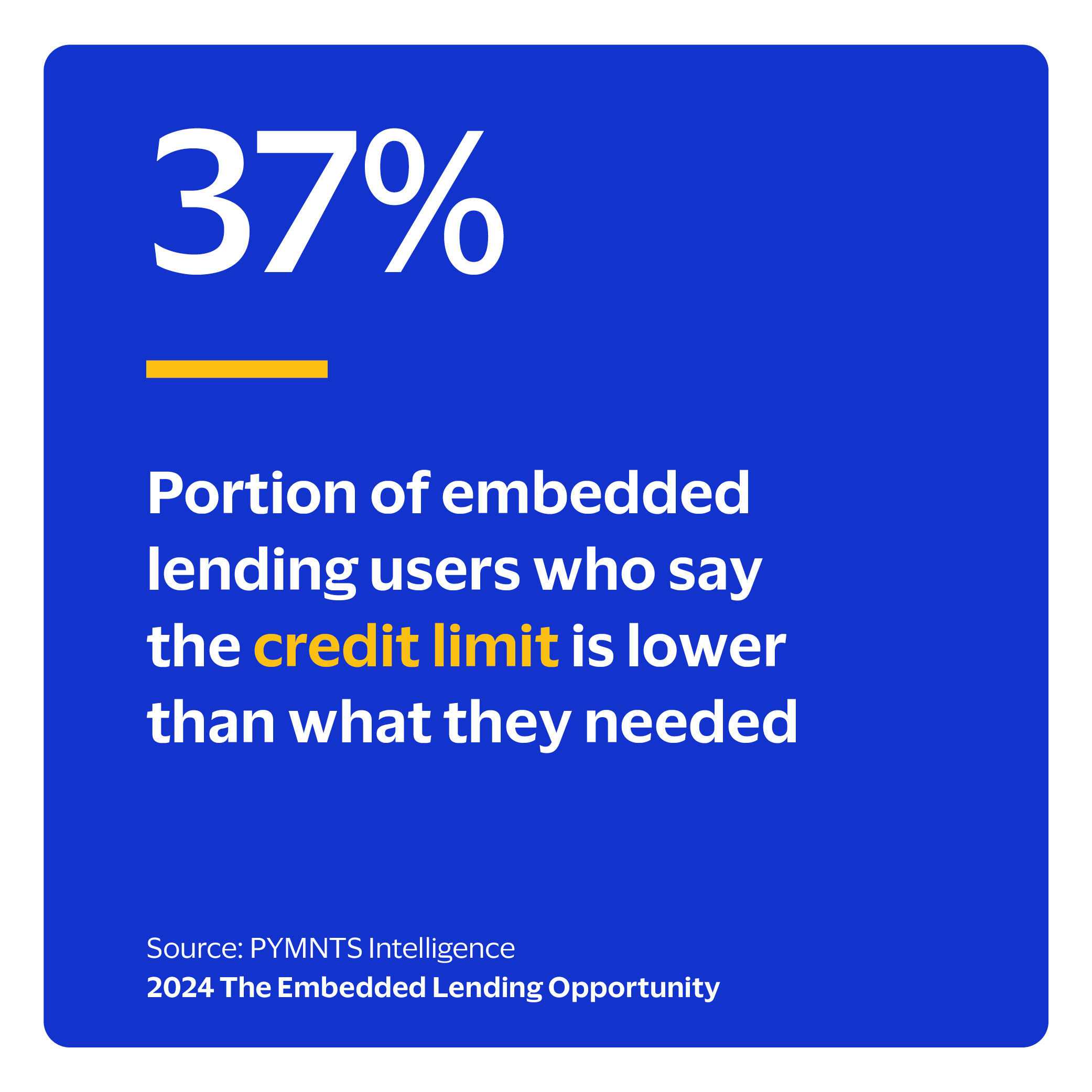

Among consumers who used credit products in the last year, 30% said they would likely prefer embedded lending for emergency expenses. The share jumps considerably for those who say they generally use financing out of need. However, sufficient credit limits need to be available to meet these needs.

Nearly half of consumers express strong interest in changing to providers offering these lending options. Still, providers must address friction points and understand consumer dynamics to draw them in. Download the report to learn how embedded lending can meet unfulfilled demand in the consumer finance space.