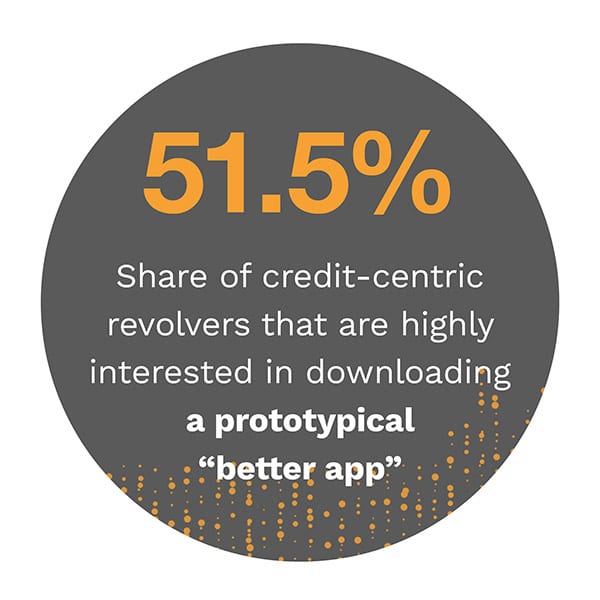

There is an important underlying dimension to these findings, however. Interest in mobile card apps is especially high among two key groups: those who primarily use debit cards for purchases and those who primarily use credit cards while carrying balances every month. Among the former group, 46.3 percent would be very or extremely interested in downloading a prototypical “better app,” as would 51.5 percent of the latter. In other words, consumers who perceive the greatest value in mobile card management tools are those carrying debt on credit cards and those who are inclined to keep their spending in check by using debit cards, whether by choice or necessity. These tools are likely to only become more important to budget-conscious consumers during the economic downturn.

There is an important underlying dimension to these findings, however. Interest in mobile card apps is especially high among two key groups: those who primarily use debit cards for purchases and those who primarily use credit cards while carrying balances every month. Among the former group, 46.3 percent would be very or extremely interested in downloading a prototypical “better app,” as would 51.5 percent of the latter. In other words, consumers who perceive the greatest value in mobile card management tools are those carrying debt on credit cards and those who are inclined to keep their spending in check by using debit cards, whether by choice or necessity. These tools are likely to only become more important to budget-conscious consumers during the economic downturn.

How card use and spending patterns relate to interest in mobile card apps is the focus of the latest in the Building A Better App Playbook series, The Card User Preferences Edition, a PYMNTS and Ondot collaboration based on a survey of more than 3,000 cardholders. The Playbook series examines the key app features and functions that could drive greater adoption of card apps and could even lead cardholders to switch banks to obtain them.

To conduct our analysis, we divided cardholders into three groups: debit-centric, those who primarily use debit cards for purchases; credit-centric revolvers, those who primarily use credit cards and carry balances each month; and credit-centric transactors, those who primarily use credit cards and pay off entire balances each month.

To conduct our analysis, we divided cardholders into three groups: debit-centric, those who primarily use debit cards for purchases; credit-centric revolvers, those who primarily use credit cards and carry balances each month; and credit-centric transactors, those who primarily use credit cards and pay off entire balances each month.

Our research reveals that while credit-centric revolvers and debit-centric consumers are the most interested in downloading better card apps, the features they find most compelling diverge in interesting ways. Three features stand out as the most popular for both groups: reporting cards lost or stolen (at least 67 percent are interested), disputing incorrect or fraudulent transactions (67 percent) and setting preferences for alerts (54 percent). Credit-centric revolvers are interested in a wider range of features, however, specifically those that could help them get a better handle on their finances. Among this group, 57.9 percent are interested in payment plans for large purchases, for example, and 54.1 percent are interested in spending insights.

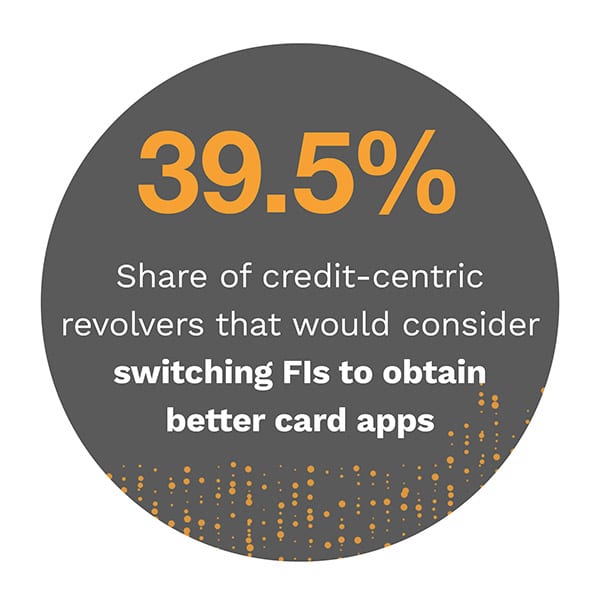

Card apps are not viewed as mere side benefits for significant shares of consumers: More than a quarter of them overall would be willing to switch financial institutions (FIs) to access better card apps. Yet, there is an important distinction between credit-centric revolvers and debit-centric consumers in this regard. The former would be remarkably motivated to switch FIs — 39.5 percent of them would be at least somewhat likely to do so — while debit centric consumers are less inclined, with 28.7 percent of them willing to switch.

Card apps are not viewed as mere side benefits for significant shares of consumers: More than a quarter of them overall would be willing to switch financial institutions (FIs) to access better card apps. Yet, there is an important distinction between credit-centric revolvers and debit-centric consumers in this regard. The former would be remarkably motivated to switch FIs — 39.5 percent of them would be at least somewhat likely to do so — while debit centric consumers are less inclined, with 28.7 percent of them willing to switch.

This makes sense considering that switching banks is a more significant move than switching credit cards, and it also points to an important advantage that smaller debit card-issuing banks may wield in the competitive arena of digital banking services. These banks may stand a better chance of retaining the loyalty of their customers than credit card issuers — provided they can meet their customers’ appetites for better mobile card apps.

About The Playbook

The Building A Better App Playbook: The Card User Preferences Edition is based on a survey of more than 3,000 consumers and examines how debit and credit card use patterns relates to demand for better mobile digital services.

Convincing consumers to designate precious space on their mobile phones to download yet another app can be a tough sell these days. Yet, large shares of consumers would be willing to make room for additional apps that can give them greater control over their spending. PYMNTS research has shown that approximately 40 percent of consumers would be very interested in downloading highly functional mobile card apps that can be used to manage multiple cards, track spending and issue transaction alerts, among many other features.

Convincing consumers to designate precious space on their mobile phones to download yet another app can be a tough sell these days. Yet, large shares of consumers would be willing to make room for additional apps that can give them greater control over their spending. PYMNTS research has shown that approximately 40 percent of consumers would be very interested in downloading highly functional mobile card apps that can be used to manage multiple cards, track spending and issue transaction alerts, among many other features.