“Traditional banks aren’t mobile-first, and they’re definitely not customer-first. As more and more people use their smartphones to manage money, we saw an opportunity to address another customer pain point,” said John Legere, CEO of T-Mobile, according to a press release.

This might be a ploy to retain T-Mobile customers, but it’s also intended to appeal to consumers without any real affinity for a more traditional financial services provider, including the highly coveted millennial, as well as the unbanked and underbanked.

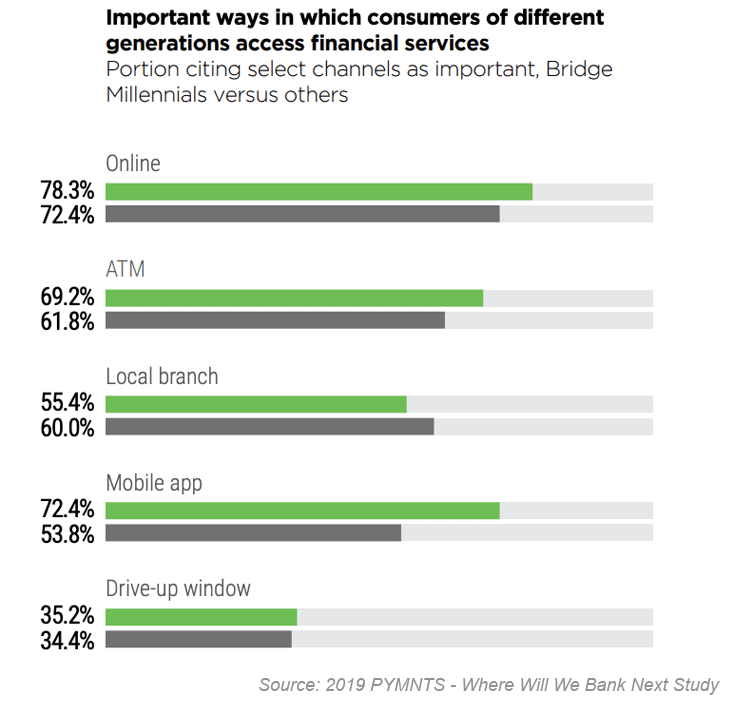

T-Mobile MONEY isn’t the first non-bank to offer branded banking services, or to tap into the consumer desire to seek an alternative to the more traditional bank. Findings from the April 2019 Where Will We Bank Next? survey by PYMNTS found an openness among U.S. consumers to these non-traditional forms of banking, fueled in part by a strong preference among younger (but not the youngest) consumers for mobile access. In fact, 72.4 percent of Bridge Millennials, ages 30 to 40, said mobile apps were important in accessing bank accounts, compared to 53.8 percent of all consumers.

Overall, 57.5 percent of all consumers indicated interest in receiving some banking services with these new, alternative brands. Part of that interest may have a lot to do with what consumers expect from banks, and how available those services are from others. This study showed that checking accounts were the most wanted service (87.3 percent), and trust was cited as the number-one reason why a bank fit a customer’s needs (63.3 percent).

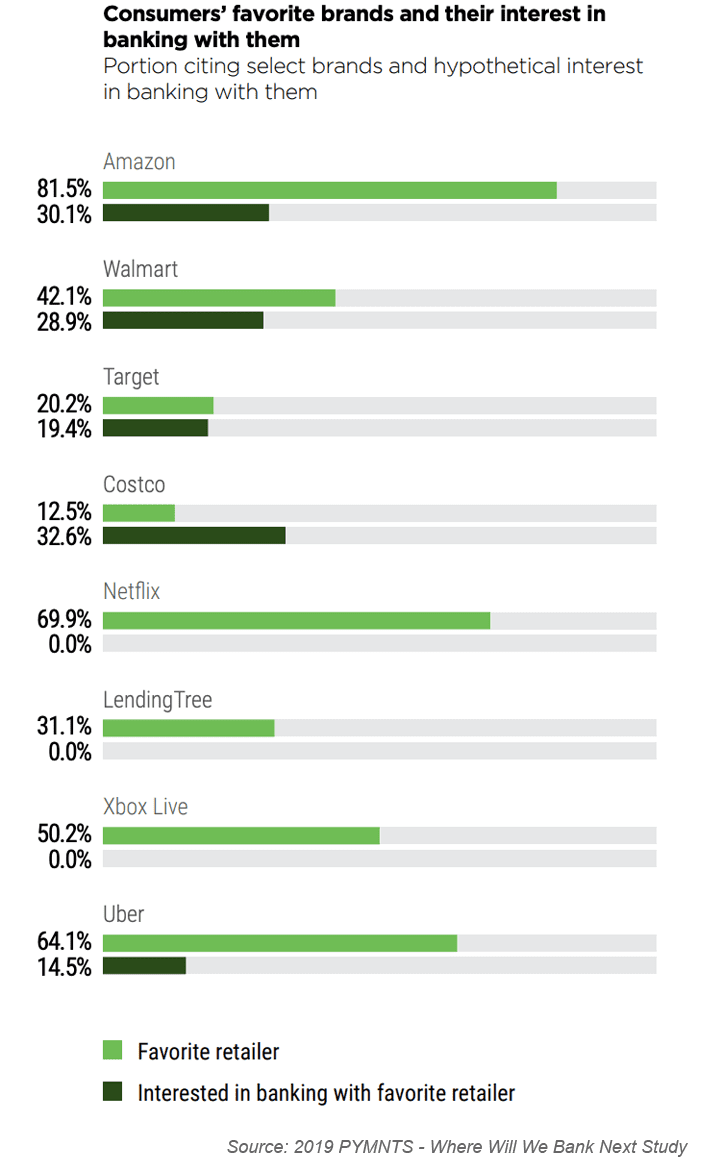

Trust may play a role in customer satisfaction with financial institutions (FIs), but, according to the study, familiarity would potentially influence consumer choice of non-traditional FIs as well. When asked about favorite brands and retailers, Amazon, Walmart, Target and Costco topped the list. These same brands also ranked highly on hypothetical interest in banking with them.

Though likeability wasn’t the only criteria for trying a non-FI, there must certainly be a financial or transactional relationship in place to make the switch plausible. Not surprisingly, PayPal, Amazon and Walmart received a good deal of consumer interest as non-FIs. These established brands already offer payment solutions, and link to bank accounts or credit cards, upping consumer trust. On the flip side, many said Netflix and Xbox Live were favorite brands, but none would want to bank with those companies.

Taken as a whole, online retail was the category that most consumers were interested in using for banking. One in five consumers agreed with online retailers serving as FIs, while 27.5 percent of Bridge Millennials did so.

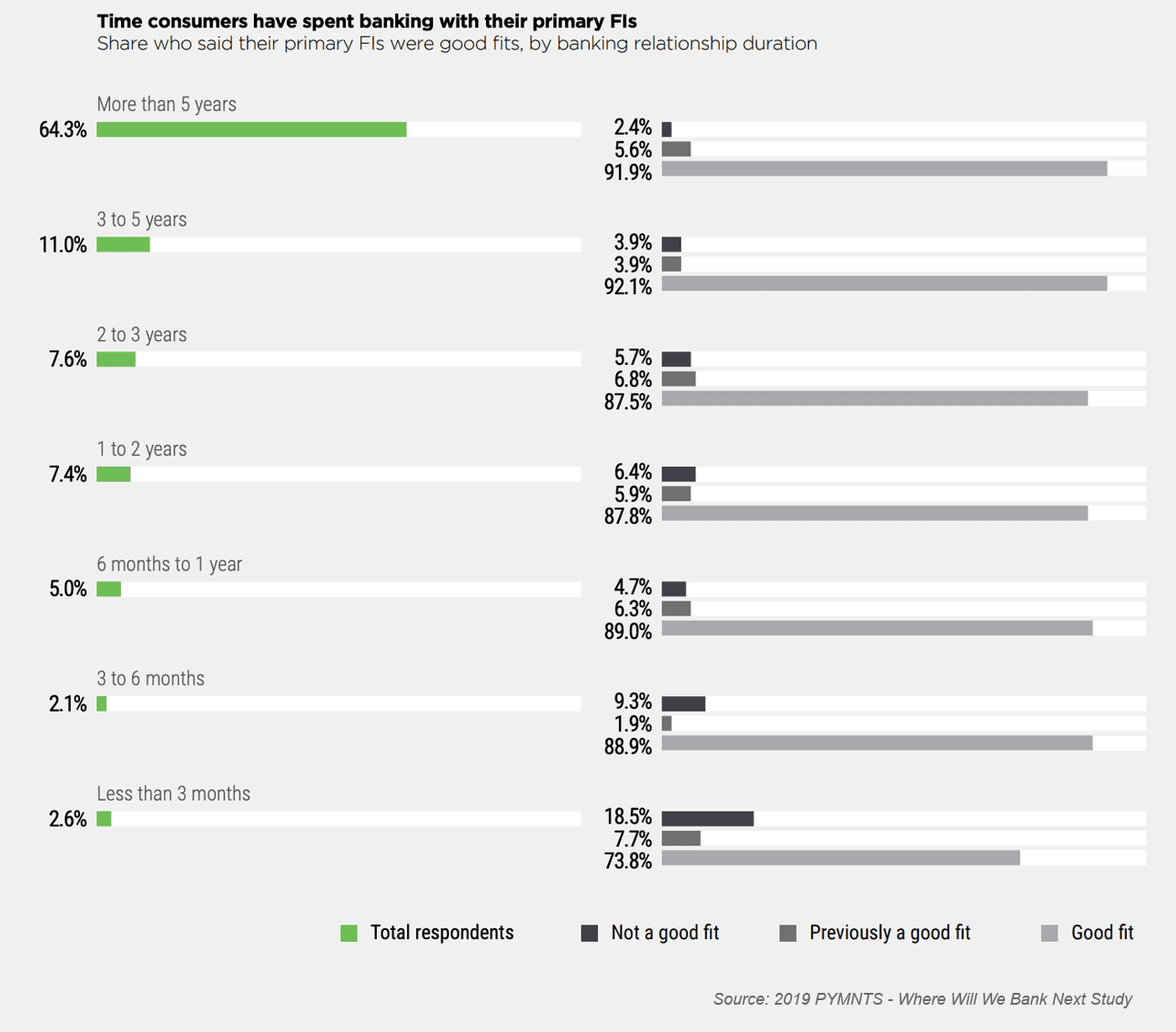

Age was a factor in openness to new types of banking service providers. The largest group (32.5 percent) with interest in switching were those aged 24 to 35. Interest declined with age; only 6.1 percent of consumers 65-plus were “very” or “extremely” interested in switching FIs. (Length of time with an FI corresponds with overall satisfaction, and older consumers might be more likely to have had a longer relationship with a particular bank than younger consumers.)

Non-FIs offering banking services is still a new concept, so it’s logical that not everyone would be on board yet. That hasn’t stopped brands from trying, though. In the PYMNTS study, only 12.1 percent of consumers indicated interest in using Apple as an FI — meanwhile, in March, Apple debuted its own credit card. The latest non-FI with plans to step into the space is Venmo. Last week, there was speculation that Venmo would also launch a credit card.

The PYMNTS study didn’t specifically ask about Venmo, but parent company PayPal was popular as a banking alternative, with 30.5 percent of all consumers open to switching. PayPal had particularly high interest among Gen X (54.7 percent).

Wireless carriers ranked fairly low with the total: AT&T (7.7 percent), Verizon (6.4 percent) and T-Mobile (4.8 percent), yet Bridge Millennials had higher interest in all three companies. Only 7.2 percent of Bridge Millennials cited interest in T-Mobile as an FI. However, the importance of mobile banking apps to this generational subset, coupled with their openness in trying non-traditional banking, could work in T-Mobile’s — and other wireless carriers’ — favor.

It might be some time before we see Uber or Netflix banking (though Uber took a stab at it a few years ago), but anything is possible. Most wouldn’t have predicted that Starbucks’ app would become the most popular proximity mobile payment app in the U.S. either.