Would it surprise you to learn that Gen Z consumers — the oldest of whom turn 24 this year — are the most likely of all demographic groups to seek information on life insurance? Coming out of the COVID-19 episode, few things are truly surprising — but that finding is.

PYMNTS’ new Life Insurance Engagement Report: Consumers, FIs and the Life Insurance Digital Path to Purchase, a Franklin Madison collaboration, is packed with those types of eye-openers, as banks and financial institutions (FIs) are viewing insurance as a viable new revenue stream.

Researchers surveyed over 2,300 consumers about their behaviors and attitudes toward life insurance for the report, finding that “the rise in the number of newly insured, younger consumers and an increased general interest in life insurance products among younger demographics has had a significant impact on the insurance industry landscape. Opportunities now abound for insurance providers to engage new audiences and build enduring customer relationships over time.”

A clear takeaway is that “consumers want to comparison shop, pay and interact with their providers how they want and when they want,” yet they want to close the deal with another human being. Per the report, “our research shows that consumers prefer to discuss their life insurance choices in person before purchasing, even when the decision process that brings them to a particular insurance product runs through digital channels.”

It spells new money flows and deeper engagement for banks and FIs that decide to leverage their positions of trust, providing consumers with the coverages they seek post-COVID.

Consumer Trust a Deciding Factor for Insurance Post-Pandemic

Consumer Trust a Deciding Factor for Insurance Post-Pandemic

Conducting research for the new Life Insurance Engagement Report, we found that 60 percent of respondents report having life insurance. They’re an interesting group, but more interesting still is the 40 percent of consumers who said they carry little or no life insurance.

Per the report, those without life insurance include baby boomers and older seniors (38 percent), Generation Z (40 percent) and Generation X (36 percent). These groups “represent significantly under-tapped audiences for insurers. Consumers who chose not to purchase a policy gave reasons that were essentially the result of exposure to poor — if any — marketing messages, such as a lack of clarity on their life insurance options or concerns about premium costs. Most of these consumer concerns could be resolved by insurance providers implementing effective marketing and consumer education plans that address key consumer concerns about life insurance.”

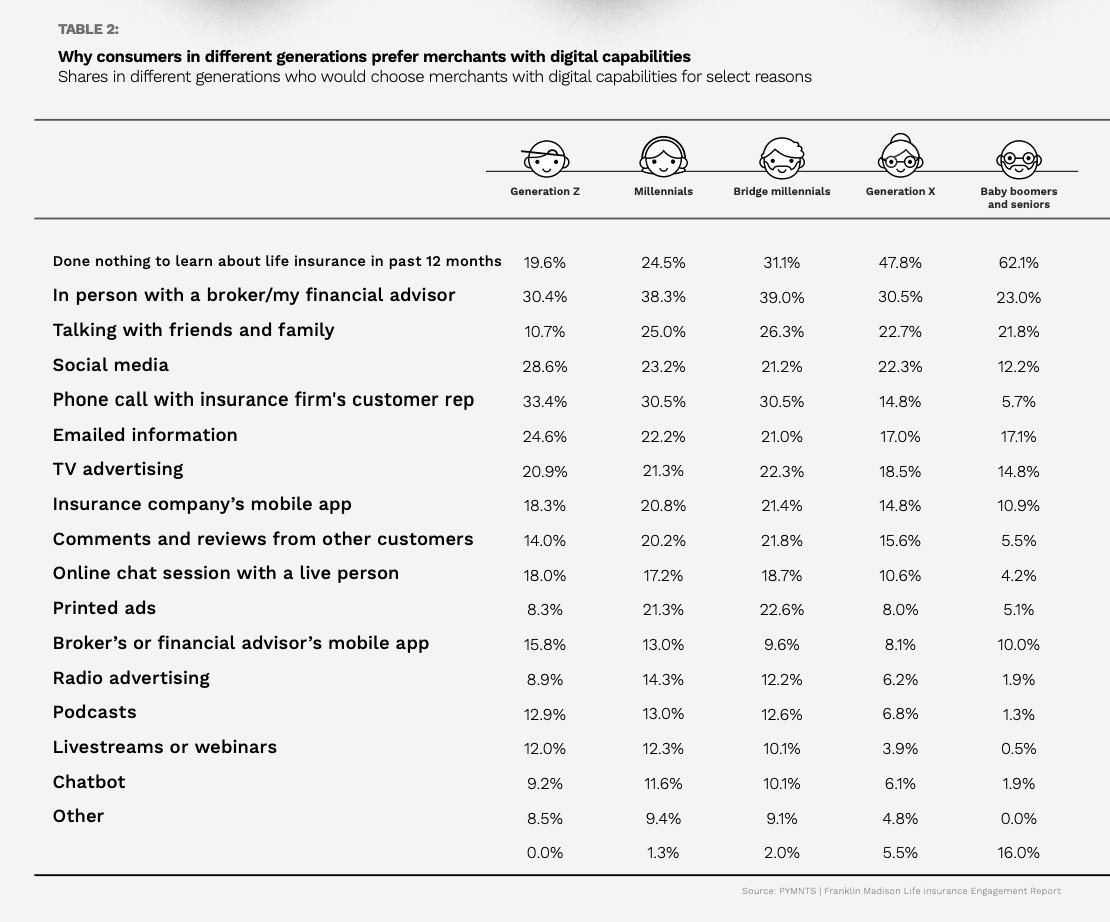

How people learn about insurance is where the rubber meets the road for banks and FIs. Consumers use an assortment of social and online sources, such as friends and family (25 percent), customer comments and reviews (19 percent) and social media (10 percent) when seeking information about life insurance. “Insurance providers can leverage these connections by creating a 360-degree marketing strategy that is data-driven and content-focused,” per the report.

Access to information is a “crucial determinant in the life insurance purchase journey of a significant number of consumers,” the report states, adding that roughly 37 percent of consumers don’t know if their FIs offer life insurance, and 32 percent of consumers want more information about their FIs’ life insurance products. “The opportunity for insurance providers to ‘get it right’ is clear: Life insurance product information should be readily available, easy to understand and unambiguous about affordability, product function and relevance to the unique needs of each audience,” the report states.

People Who Need People

With 35 percent of life insurance customers preferring live human interactions with brokers and advisers over other ways of buying insurance (self-directed web searches are the second-most popular method at 31 percent), banks and FIs rarely face such easy product decisions.

According to the Life Insurance Engagement Report, 38 percent of consumers think life insurance should be more affordable, while 30 percent feel that buying it should be easier. More importantly, “…29 percent of customers who had already purchased insurance from their primary FIs report that they wanted better information from their providers. That means insurance providers have an open invitation to deliver meaningful marketing messages to consumers motivated to hear about new life insurance products and payment solutions that make those products more affordable.”

To that end, the report states that insurers and FIs that want this business “must provide an effective hybrid model of customer service — one that blends clear product information with live or text chat help for self-directed customers interested in a human-focused insurance-buying experience.”