The most recent Nobel laureates in economics confirm that banks have cemented a level of trust with consumers that is invaluable.

The Nobel Prize in Economic Services was awarded to former Federal Reserve Chief Ben Bernanke and to Douglas Diamond and Philip H. Dybvig, economists, respectively, at the University of Chicago and Washington University.

And while the Nobel Committee said the work of the trio touched on everything from the role of banks in the Great Depression to the Great Financial Crisis, there was also a singling out of work that showed the intermediary role banks play in the modern economy, as The Wall Street Journal (WSJ) and other news sites reported.

“Diamond and Dybvig … presented a theory of ‘maturity transformation’ and showed that an institution using demand deposits to finance long-term projects is the most efficient arrangement,” even as banks are vulnerable to bank runs, the committee wrote.

And in the traditional relationships that are established, per the relationship between Diamond and Dybvig, banks channel funds from savers to investors, making it possible for the borrower to have a long-term financing agreement, while simultaneously, lenders can withdraw the money they lent to the bank on demand. Thus, financial intermediaries perform essential functions for society, and their insights into their customers is invaluable too, as WSJ noted.

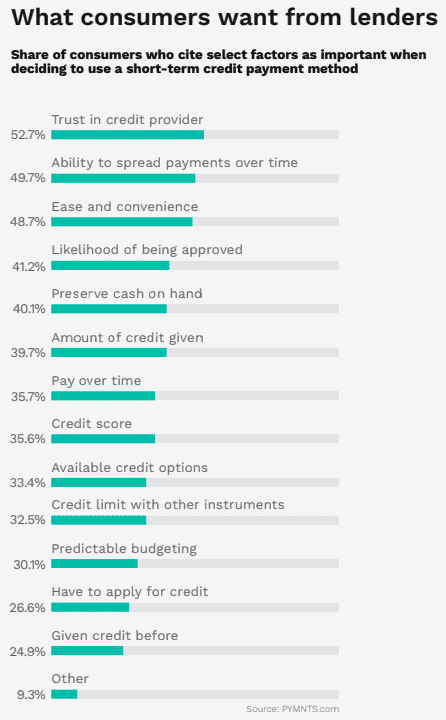

Inherent here is the issue of trust, which has been borne out by PYMNTS’ own data. Beyond those basic and fundamental activities of deposits and lending, we’re seeing that banks are among the “go-to” or “top-of-mind” providers for all sorts of new, digital-first initiatives, and by extension, greater access to credit for individuals.

The rise of buy now, pay later (BNPL) and the opportunity for banks here represents a microcosm. As PYMNTS found in “BNPL, Banks and the Trust Factor,” 53% of consumers have already used short-term credit and stated that borrowing from trusted lenders is important.

Elsewhere in the potential development of a super app — a digital front door that provides access to a broad continuum of daily activities, all linked together — banks again hold the top spot as trusted providers. Late last month, joint research from PYMNTS and PayPal found that a similar percentage as the previous PYMNTS study — 53% — trust banks to craft and deliver the super app.

The common thread here is that the banks have the decades of experience in place with individual consumers, with families and with enterprise clients that provide a launching pad for banks to invest the time and money in those new initiatives (through the size of the capital bases). The deposits and the checking and lending accounts offer a natural segue into new activities, such as applying for mortgages online.

At the same time, the clients themselves have enough familiarity with the financial institution (FI) itself to know that data and money are safer than might be held otherwise, with less-regulated entities.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More