With most consumers who migrated to online shopping during the pandemic expected to remain there, eCommerce will most likely remain the dominant form of purchase for many products.

A growing percentage of these online sales will be made across borders, with predictions that the value of cross-border retail payments will reach $3.6 trillion by 2022. This soaring global eCommerce market is accompanied by an increase in local payment methods, with regions adopting a wide variety of online payment preferences to meet consumers’ needs.

In the October edition of “Cross-Border Retail Payments Tracker®,” PYMNTS explores how the right payment gateway solution can help merchants manage local payment options, minimizing payment frictions and enabling retailers to better attract and retain cross-border customers.

Around Cross-Border Retail Payments Space

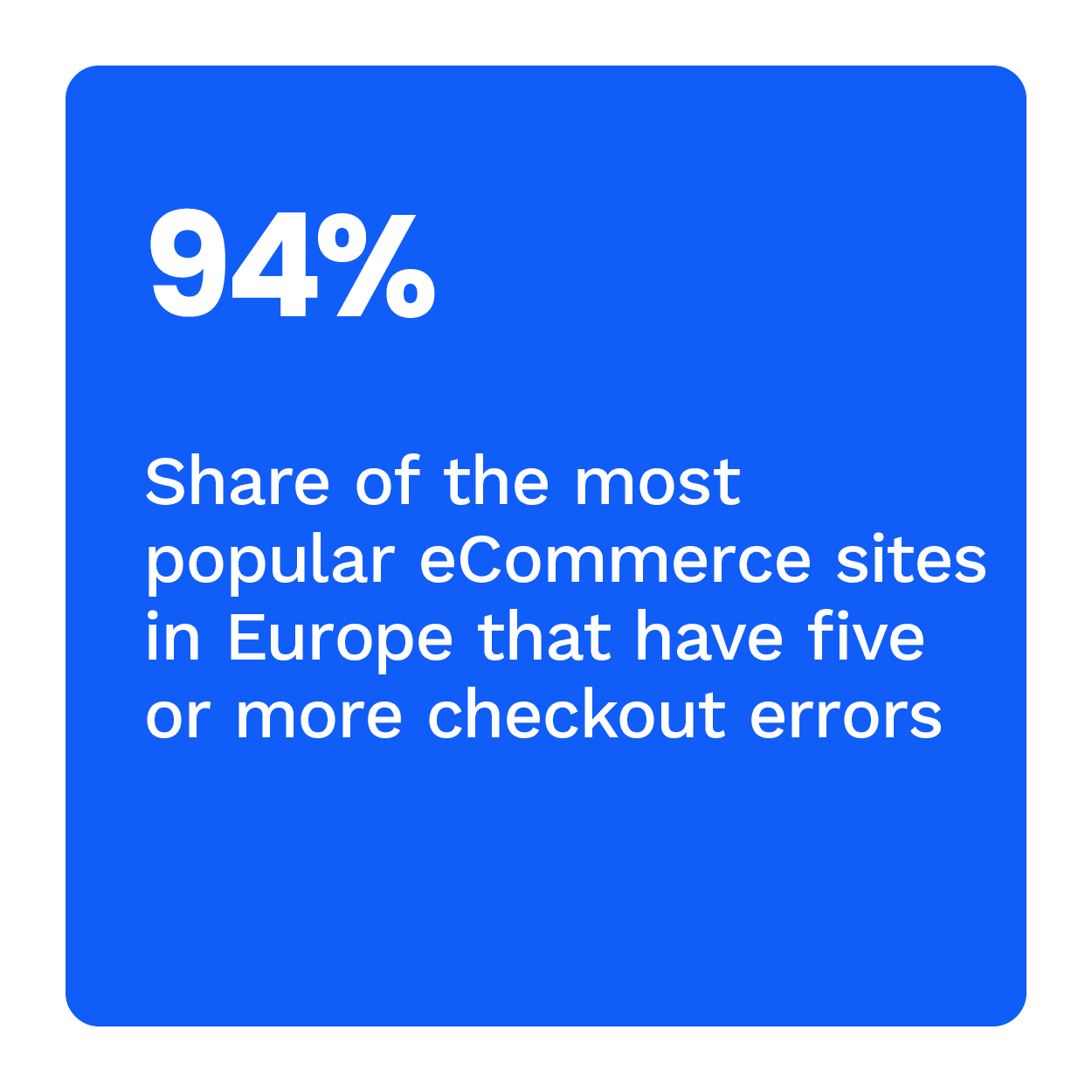

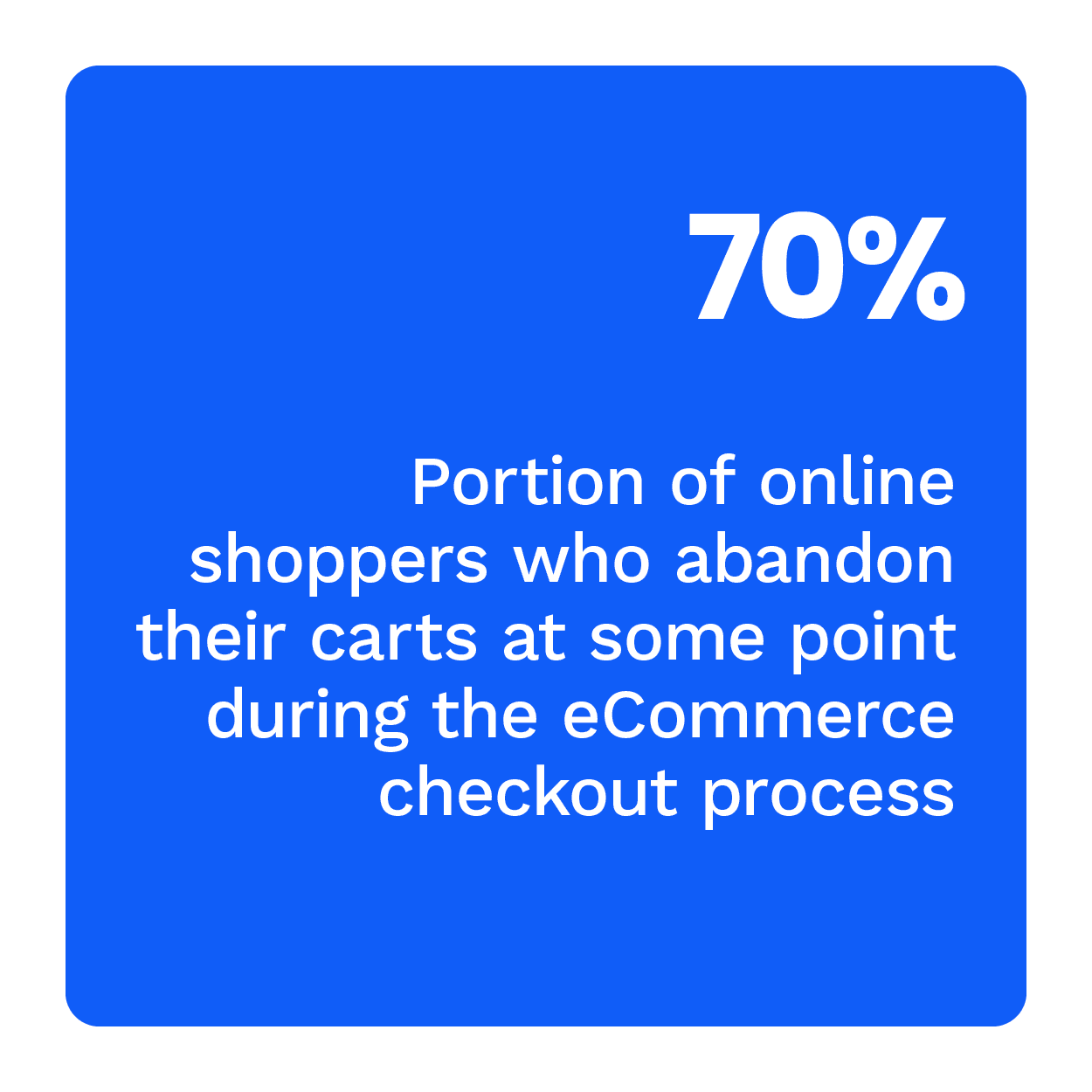

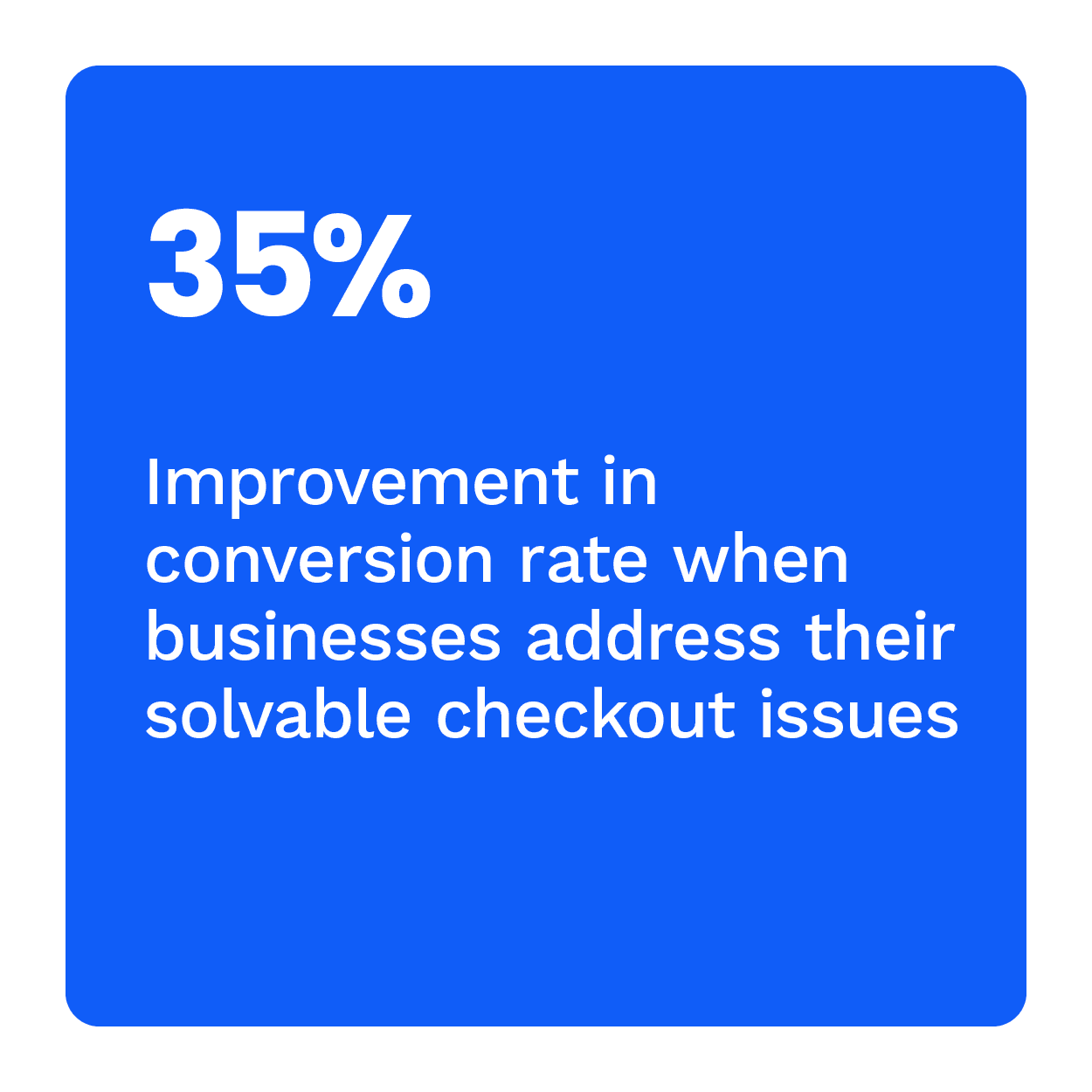

Global eCommerce sites continue to be riddled with checkout frictions, with a study finding that 94% of the most popular sites in Europe have five or more checkout errors. Formatting payment information or displaying error messages plagued 42% of these sites, while 61% did not support address autocomplete. Such errors could be solved using efficient payment gateways, helping cross-border merchants step up their game and keep pace with consumer expectations. In fact, 21% of respondents said they would abandon their carts if checkout took more than one minute, while another 15% said they would ditch their purchases if their preferred payment methods were unavailable.

The growing popularity of eCommerce is also driving growth in B2B cross-border payment transaction values. A study found that the transaction value of B2B cross-border payments of all payment types will grow by more than 25%, from $34 trillion this year to nearly $43 trillion by 2026. The mainstay for cross-border transactions, wire transfers, will reach 80% of overall transaction value by 2026. Instant payments still account for a relatively low proportion of B2B wire transfers, making up just 22% of overall transaction values by 2026.

The growing popularity of eCommerce is also driving growth in B2B cross-border payment transaction values. A study found that the transaction value of B2B cross-border payments of all payment types will grow by more than 25%, from $34 trillion this year to nearly $43 trillion by 2026. The mainstay for cross-border transactions, wire transfers, will reach 80% of overall transaction value by 2026. Instant payments still account for a relatively low proportion of B2B wire transfers, making up just 22% of overall transaction values by 2026.

The central banks of Indonesia and Thailand announced an agreement that links both nations’ retail payment system operators, allowing consumers and merchants to make and accept instant cross-border QR code payments. Consumers in each country can use their mobile devices to scan QR codes to pay merchants in real time in the other country. The initiative, currently in the pilot phase, is scheduled for a full rollout in the first quarter of 2022.

For more on these stories and other cross-border retail payment developments, read the Tracker’s News and Trends section.

Artsy on How Leveraging a Mobile-First Approach Helps Drive Frictionless Cross-Border Sales

As the demand for buying art online soared during the lockdown, galleries and auction houses became less reticent to transacting with customers outside their traditional brick-and-mortar display and sales outlets. The pandemic saw a dramatic increase in collectors turning to eCommerce marketplaces to view and purchase art, along with a surge in new art buyers.

In this month’s Feature Story, Artsy Chief Revenue Officer Dustyn Kim explains how the online brokerage’s mobile-first approach helps drive global art sales while ensuring frictionless cross-border transactions.

Deep Dive: Helping Cross-Border eRetailers Embrace Local Payment Options

As cross-border eCommerce continues to grow, it offers a significant opportunity for merchants looking to expand their global trade. To thrive on the world stage, however, retailers need to accommodate an expanding range of payment options specific to various local markets.

This month’s Deep Dive explores how deploying one or more payment gateway can help minimize payment frictions, facilitating faster and more transparent online sales transactions and keeping customers coming back for more.

About the Tracker

The “Cross-Border Retail Payments Tracker®,” done in collaboration with Citcon, examines the latest developments in cross-border retail payments.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More