For FinTechs, the key to keeping customers lies with speed and ease, especially for money mobility.

Mobility refers to money in and money out — the ebb and flow of funds between accounts. And that money can include everything from peer-to-peer (P2P) payments to money moved between a single holder’s own accounts.

The FinTechs enabling that activity, day in and day out, are faced with the Herculean tasks of monitoring and measuring risk in an age where online transactions are the norm, and where fraudsters are wilier than ever. The issuers must grapple with the challenge of making it easier for customers to move money while ensuring that authentication and anti-fraud efforts are robust.

The FinTechs are jockeying for loyalty and wallet share among customers that could opt, instead, to keep their money with traditional financial institutions.

To that end, in the latest “Money Mobility Friction Index,” a PYMNTS and Ingo Money collaboration, there are some encouraging signs — and some pointed signs too — about where things can be improved.

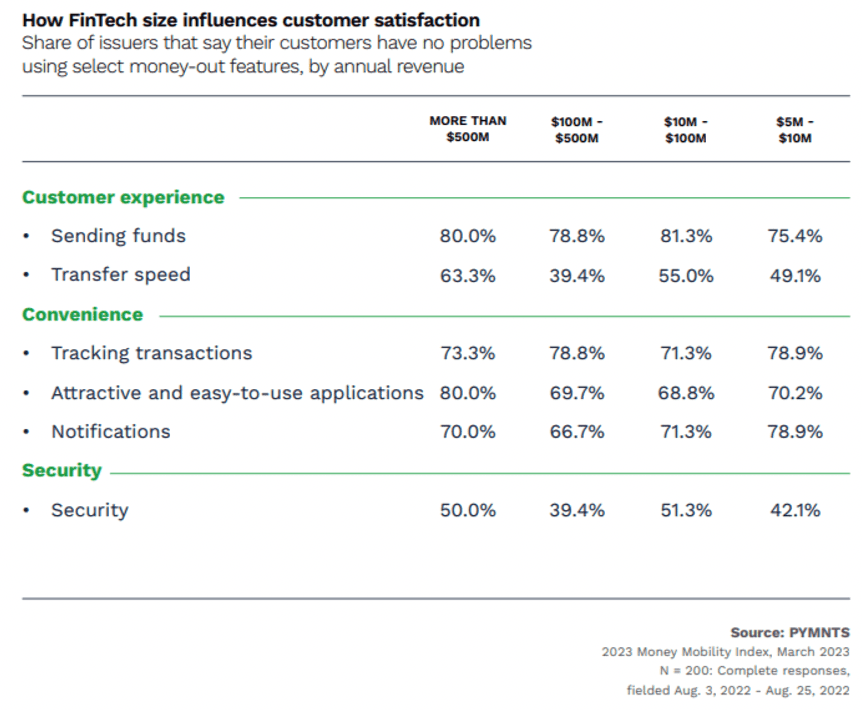

The vast majority of FinTechs said their customers don’t experience pain points and friction when it comes to sending money from their accounts. And, in this case, the bigger the institution, the more satisfied consumers are. The largest issuers, with top line above $500 million annually, see the highest satisfaction at more than 80%.

But as to where there is room for improvement, outbound money mobility is proving to be a smoother endeavor than inbound flows. PYMNTS research found that complex transfer processes can make it harder for consumers to deposit into accounts. Only about 57% of customers at the larger FinTech issuers — again the ones with more than $500 million in revenues — said that they have “no problems” receiving funds.

But as to where there is room for improvement, outbound money mobility is proving to be a smoother endeavor than inbound flows. PYMNTS research found that complex transfer processes can make it harder for consumers to deposit into accounts. Only about 57% of customers at the larger FinTech issuers — again the ones with more than $500 million in revenues — said that they have “no problems” receiving funds.

The complexity is spotlighted by the fact that the largest FinTech issuers offer an average of five payment methods for money in and money out. The more instant payment options issuers provide, the more their customers are apt to use their accounts, signaling to all issuers the paths they must take in the months and the years ahead.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More