![]()

—

![]() Harry Luscombe hears it all the time from merchants. When considering faster payment options, they are concerned that customers may not want an open banking payment at checkout.

Harry Luscombe hears it all the time from merchants. When considering faster payment options, they are concerned that customers may not want an open banking payment at checkout.

Luscombe, the co-founder and CEO of mobile-first open banking payment solution Boodil, is quick to point out that most customers do not express their preferences and might even abandon their checkouts or choose less preferable payment options if their preferred methods are not available.

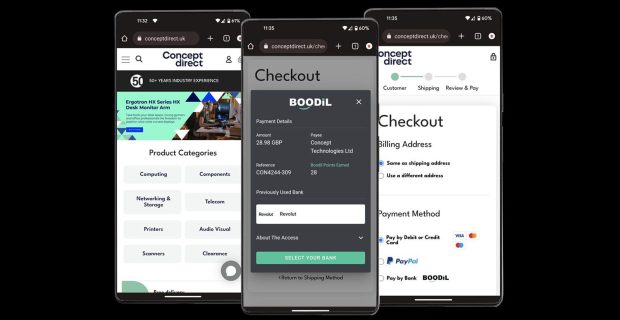

Boodil aims to create a compelling reason for customers to choose its payment method through its innovative rewards program, ultimately benefiting the merchants through lower fees, instant settlement of funds and removal of chargebacks. The Manchester, United Kingdom-based startup is using the country’s open banking rails to provide a mobile-first payment solution and consumer engagement platform.

“Our aim is to reward and incentivize consumers every time they check out via our payment method,” said Luscombe.

The company has grown quickly since launching its offering early this year. Luscombe and his co-founders were committed to creating a faster payment solution that was unique and offered more than just open banking payment rails, especially considering how open banking has matured in the U.K. since its introduction in 2017.

Boodil is helping merchants adopt faster payments and drive increased customer loyalty by offering redeemable points every time customers spend using Boodil as their payment method. Through the Boodil app, customers can redeem points for prize draws and discounts at various retailers, further incentivizing customers to choose Boodil for their payments.

Boodil has added 50 businesses to its client list in the space of about three months. The open banking payments adoption rate, however, is still low, hovering between 3% and 5%, Luscombe estimated. One reason for the lag in adoption is that the U.K.’s biggest eCommerce retailers have yet to jump on board. Consumers, meanwhile, are faced with inconsistent terminology — pay by bank, pay with bank, cardless payments or open banking payments — which creates confusion and stifles awareness.

Luscombe drew a comparison to contactless payments adoption over the first three years. PYMNTS data shows that open banking’s growth rate over its first three years has been faster than that of contactless, demonstrating its potential.

Luscombe said he is surprised to see so many businesses continue to use manual bank transfers, which can be prone to error and are slow and inefficient, when open banking payment options such as Boodil’s can save 60% to 70% on credit card costs while driving increased loyalty and customer engagement.

“The more merchants adopt the payment method, the more customers will become [familiar] with it, which will thus stimulate adoption and growth,” said Luscombe.

Of course, it can be cumbersome to implement new payment solutions to checkout. To make implementation as seamless as possible for merchants, Boodil has built a simple onboarding experience and easy integration options. Luscombe said the entire process takes less than 10 minutes.

“We have seen certain providers that don’t offer that out-of-the-box solution, so we have made it simple and easy for merchants to add to their checkout,” said Luscombe.

When considering adopting faster payments or new payment methods, Boodil suggests that businesses provide information and marketing collateral to instill trust and encourage customers to try out the new payment solution. By highlighting the safety, security and rewarding nature of their payment methods on their websites or through marketing materials, businesses can help drive customer adoption and loyalty.

Luscombe said Boodil will be enhancing its app throughout the year, with a “version 2.0” launching by early next year. Along the way, Boodil is adding tools for businesses such as its payments portal, which enables businesses to send out payment links via SMS, email or QR codes and customers to pay invoices and bills through open banking payments. The company is also rolling out a merchant dashboard detailing Boodil-led transactions and customer insights as it positions itself for a seed raise in Q3 2023.

“We’re planning for constant improvements going forward,” Luscome said.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More