After credit and debit, what is the most popular method for paying bills? If you guessed pay by bank transfers, you’d be correct.

According to the study “New Payment Options: Building Stronger Customer Ties With Pay By Bank Transfer,” a PYMNTS and Nuvei collaboration, online bank transfers are the most preferred method for recurring bill pay, with consumers citing several reasons for that.

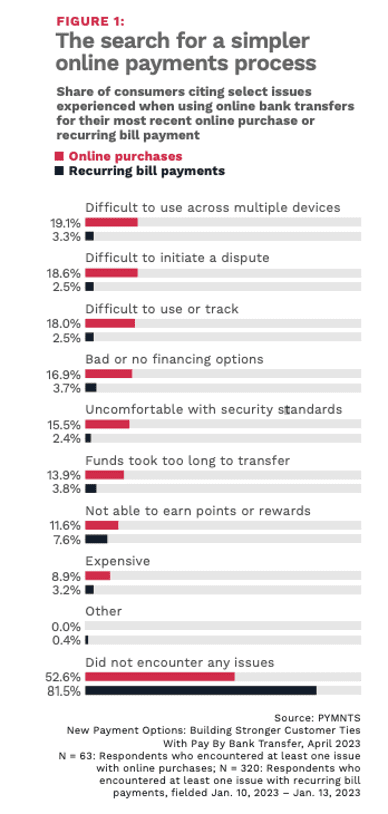

For context, we found that 60% of consumers experienced at least one payment problem during their most recent bill payment or online purchase, mentioning issues from a limited number of financing options to weak rewards to “perceived inadequacy with security.”

Our survey of over 2,000 U.S. consumers found 33% of consumers who paid recurring bills using online bank transfers cited ease and convenience as the main reasons for using this method.

Bill pay is a nascent use case for online bank transfers, but the data shows that 42% of consumers who have paid for an eCommerce purchase using online bank transfer find it easy and convenient, and those are strong drivers for greater use of the method for bill pay.

While bank transfers come with more friction complaints than credit and debit, for example, that friction is indicative of the more stringent security measures used by banks when sending money from a consumer’s account, and that “friendly friction” is a big part of the appeal.

To illustrate, 19% of consumers who paid for their most recent online purchase using an online bank transfer said they “encountered some difficulty when initiating a dispute with a merchant,” while another 19% said online bank transfers “are difficult to use across multiple devices.” Despite these issues, interest is building in this method, but it needs a nudge.

Rewarding New Behaviors

Consumers see this “nudge” as being rewards programs for using bank transfers for bill pay.

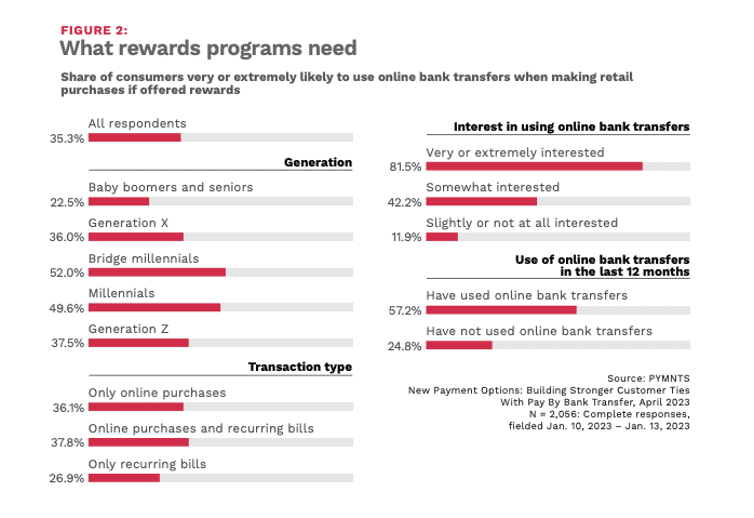

“The appeal of a rewards program for online bank transfers is a clear example where millennials and bridge millennials, consumers aged 27 to 45 who are highly valued by financial institutions, express a greater interest than other age groups,” the study states, adding that 52% of bridge millennials and 50% of millennials would be very or extremely likely to use online bank transfers to earn points in a rewards program.

Where rewards are concerned, cash is king, as close to half of those surveyed (45%) “want a program that gives them cash for paying via online bank transfers. No other potential reward category breaks the 10% threshold. Just 9.6% of consumers say gift cards are their preferred reward, while 8.2% would like discounts.”

It’s also a case where familiarity breeds trust.

The research shows that consumers who have previously used online bank transfers “are more likely to express an interest in using the method in the future than those who would be using it for the first time. Our data shows that 23% of consumers are interested in using online bank transfers when paying for retail purchases in the next year.”

Additionally, we found that 44% of those who have tried online bank transfers as a payment method are keen on doing so again. But as the study states, “the challenge is getting consumers to try the method, as just 12% of consumers who have not previously used online bank transfers are highly interested in using them in the future.”

A slow but steady increase in usage tells the tale: 35% of consumers used online bank transfers for online retail payments in January 2023, compared to 33% who did so in May 2022.

See report: New Payment Options: Building Stronger Customer Ties With Pay By Bank Transfer