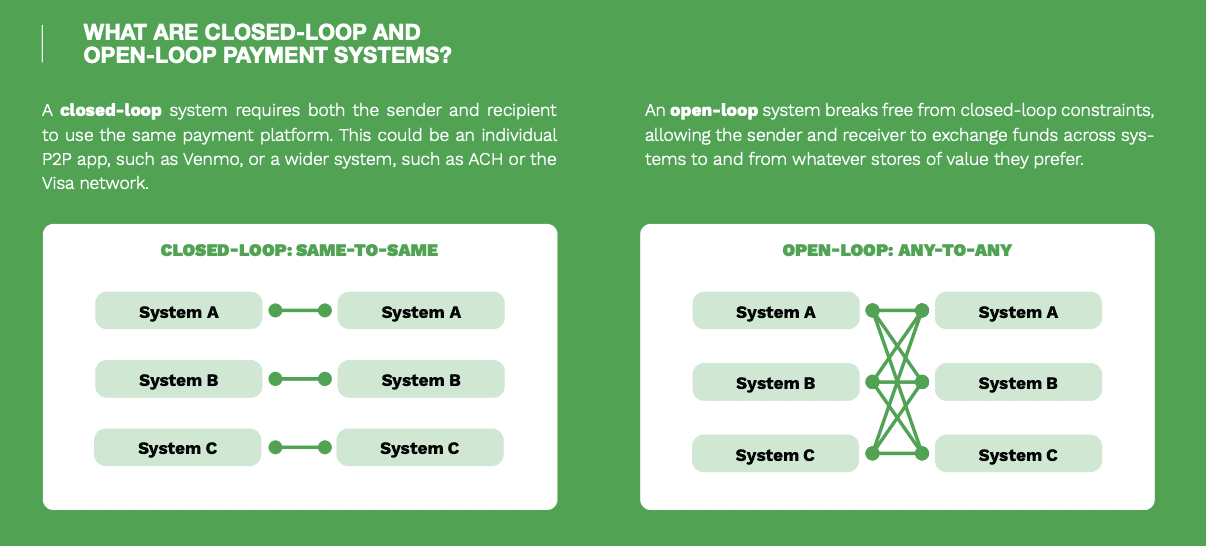

Closed-loop P2P platforms like Venmo and Zelle are handy but have limitations, requiring each party to the transfer to use the same app. Open-loop money transfers are seen as an answer to this problem.

As stated in “The Money Mobility Playbook,” a PYMNTS and Ingo Money collaboration, an open-loop, “any-to-any” framework “facilitates universal connectivity across all platforms and account types — including banking and investment, credit cards, digital wallets, lines of credit, cryptocurrency, gift cards and more. This empowers consumers and businesses to send and receive payments to and from all available stores of value — including those that may emerge in the future.”

As stated in “The Money Mobility Playbook,” a PYMNTS and Ingo Money collaboration, an open-loop, “any-to-any” framework “facilitates universal connectivity across all platforms and account types — including banking and investment, credit cards, digital wallets, lines of credit, cryptocurrency, gift cards and more. This empowers consumers and businesses to send and receive payments to and from all available stores of value — including those that may emerge in the future.”

In a somewhat fragmented selection of P2P and money transfer apps from PayPal to Venmo to Zelle, the rising trend is creating more platform interconnectedness and interoperability, offering a more seamless experience regardless of the apps or systems used.

Evidence of this demand is seen in the announcement on Tuesday (April 11) that Visa is set to pilot its Visa+ person-to-person product later this year, starting with PayPal and Venmo, then extending to other platforms to go beyond sending money to friends and family, embracing use cases from gig economy pay to earned wage access via other partners to the launch.

P2P Transfers Show Steady Growth

It’s a timely development, as PYMNTS data shows that P2P transfers are on the rise. Our analysis finds that the share of consumers who report making a P2P transfer in the past 30 days rose from 27.5% in December 2021 to 34.5% as of March 2023 — an increase of seven percentage points in just over one year.

The value of transfers has also increased over the same timeframe, as our analysis finds amounts sent were in the range of $190 in late 2021, spiking to nearly $300 in March 2022, and hovered in the range of $234 on average in March 2023.

Per our data, PayPal is the dominant P2P transfer method with 30% of consumers surveyed have used that service for their most recent P2P payment. Venmo is a distant second at 17% followed by credit cards (12%), bank transfers (11%), and digital wallets like Apple Pay (6%) and unspecified digital wallets (5%) pulling up the rear. Google Pay is dead last at 3% of transfers.

Those figures pertain to digital transfers. The picture changes for on-premises transfers like the popular “split the restaurant bill” use case. In that scenario, PayPal still comes out on top at 21%, but cash is the second most used option at 18%, followed by credit cards (14%) and bank account transfers (11%). Venmo is used just 5% of the time in on-premises transfers.

The reason P2P apps have such low usage on-premises is partly due to the different apps being used, which brings Visa+ into clearer focus as an enabler of more digital transfers regardless of setting or who around the table is using which P2P app.

As “The Money Mobility Playbook” states, “Today’s consumers and businesses want to transact at the speed of their decision-making and through any store of value they wish to deploy, without the constraints of a traditional bank, digital wallet, FinTech or other financial services provider. Genuine open-loop P2P payment networks deliver this capability.”