Google’s Super App Wakeup Call

In June of 2019, PYMNTS asked a national sample of 1,037 smartphone users about their interest in having a single app that would make their everyday activities easier to access and manage.

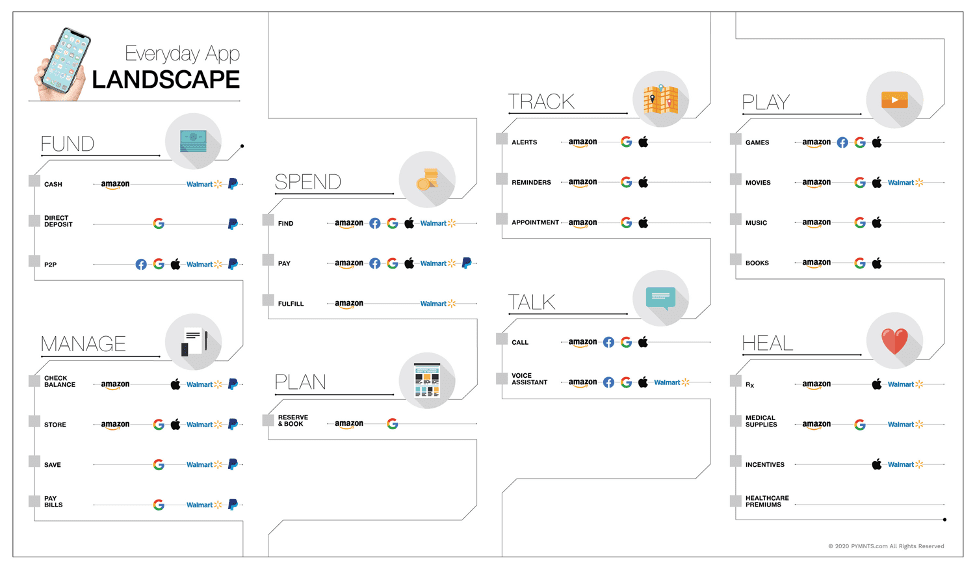

The study described the app’s functionality as a more seamless way for consumers to keep tabs on how to plan, manage, spend and send their money, and to receive funds from other sources. The app would include reminders and alerts across a variety of activities — bills to be paid, appointments to be kept, deliveries to be received, important dates to remember, what friends are doing, etc. — so as not to lose track of key dates and deliverables. There would be a way to opt-in to receive personalized offers and rewards and have those offers automatically applied at checkout when shopping and paying at those merchants.

This “super app,” we called it, would also include easier access to sign up for a variety of entertainment options like streaming services — games, music, books, video, live programming, restaurant and travel reservations and bookings, and healthcare services including the purchase of medical supplies, prescription drugs and other wellness services.

Most importantly, this “app of apps” would work across operating systems, channels and devices, and would be activated by voice and SMS.

At that time, many FinTech and Big Tech players had begun to integrate this kind of functionality into their own apps to keep users engaged and sticky, even if they didn’t call themselves “super apps.” It would be months before PayPal would announce its acquisition of the savings app Honey, and before Google would announce its Smart DDA concept with two financial institutions (FIs), adding more super app ammo to its offerings.

But even then, in June of 2019, a third of all consumers expressed a strong interest in such a super app experience, and more than half (54.2 percent) more or less said “sounds interesting, tell me more.” Only 13 percent of all consumers said “no-how-no-way.”

Labels notwithstanding, most survey respondents found this “app of apps” experience appealing. They said that hopscotching between apps and icons to access, track and organize all of the pieces of their everyday (and increasingly digital-first) lives wasted too much of their time.

Those with a keen interest in a super app — the one-third of consumers who said “sign me up” — said they’d trust Google (45 percent), followed by Amazon (29 percent), Apple (27 percent) and PayPal (22 percent) to deliver that experience. Facebook, Samsung Pay and Walmart all fared lower on the list.

Google Pay Goes Super

Last week, Google Pay introduced its redesign, including much of the functionality and user interface that consumers said they found appealing in a super app concept nearly 18 months ago. The Google Pay redesign also included the integration to their “Smart DDA” called Plex.

So far, 11 financial institutions have signed on to be part of Google Pay’s Plex account program. Two are now available via waitlist for consumers: Citi and Stanford Federal Credit Union. These were also the first two FIs to sign onto the Smart DDA proposition a little more than a year ago.

Time will tell whether consumers will do what they said they might do 18 months ago. In the meantime, Google Pay’s relaunch should serve as something of a wake-up call for digital wallets, payment apps and financial institutions as super apps in the U.S. get real.

And consumers will now have a taste for what it’s like to live in an opt-in, integrated and personalized “app of apps” digital-first commerce ecosystem.

The Digital Wallet Wake-Up Call: From Payments To Commerce

Paying for a purchase comes last — finding what to buy, getting the best deal on that item and knowing how that fits into the consumer’s budget comes first. Super apps promise to make that entire end-to-end experience seamless — and to make payments an invisible but important part of that process for consumers and merchants.

To be a super app contender, then, the starting point must be commerce, not payments. First, what consumers want to buy — their starting point — and then how they’ll pay for it.

We’ve observed this firsthand in the evolution of the general-purpose “Pay” wallets in physical stores over the five years since they launched.

What was initially positioned as a game-changer at the physical point of sale for consumers and merchants has been a disappointment.

The Pays started out by solving a checkout problem that didn’t need much fixing: What happened at the end of the shopping journey in a store already worked pretty well for consumers — pre-COVID, that is. At that point, payments for purchases just had to be fast, familiar and reliable. That’s why cards — and contactless cards — still rule at the physical point of sale, and the Pays haven’t made much difference.

Even in the midst of a global pandemic.

The latest PYMNTS data on in-store digital wallet usage reports that it’s largely flat year over year, at roughly 6 percent. After five years, Apple Pay, the in-store digital wallet pioneer, has a large share (roughly half) of that relatively small pond, but accounts for less than 1.5 percent of in-store retail sales.

We’ve observed this commerce-first, payments-second trend with the rapid shift to digital that’s happened in the wake of COVID-19.

Today, contactless payments in a store are being transformed into a digital-first and touchless commerce experience via digital channels — an experience that consumers say they find far more satisfying than shopping and checking out in a physical store.

COVID has accelerated consumers’ interest in a digital-first or digital-only experience when shopping, and all merchants report seeing explosive growth in that channel. Today, we find a consumer who is more interested in using apps and websites to shop and then pay for delivery or pick up curbside if a physical store encounter is wanted or necessary. Consumers expect that payments experience to be efficient, integrated and invisible.

But payments have had to integrate into that commerce experience — not the other way around.

We see this same trend in the relationship that consumers have with Amazon, where the starting point is searching for what to buy and payments just comes along for the ride.

It’s an ecosystem where half of online commerce now happens.

Being a Prime member gives consumers access to a growing variety of experiences inside of that expansive ecosystem — streaming services, groceries, delivery, health and fitness, and now an online pharmacy with free delivery — all linked to payments credentials that consumers don’t even think about anymore when they click “Buy.” All accessed through Amazon’s digital and mobile front door.

We observe this with the evolution of digital payment apps that started inside commerce ecosystems like Alipay (Alibaba) and PayPal (eBay) to eliminate payment friction, but are now themselves two-sided payment networks operating well beyond those marketplaces. They enable payments at online merchants and via mobile apps, but are now increasingly part of a larger shopping, savings and spending ecosystem. Acquisitions like PayPal with Honey and Xoom, and their partnerships with FinTechs like Acorns, adds commerce and financial services layers to PayPal’s core digital payments value prop.

In a digital-first world, commerce is the experience that drives differentiation, adoption and innovation, and payments is what closes the loop.

A super app ecosystem builds that bridge and drives value for all stakeholders.

Players with digital-first as their DNA have a leg up.

Google Pay’s Super App Path

We now see evidence of this in what Google Pay introduced last week.

The Google Pay app is organized around three activities: paying friends and businesses, finding offers and rewards across the Google ecosystem, and getting insights on consumer spending, all in one place.

The integration of Plex accounts into Google Pay adds a banking layer with products created by banks and credit unions for interested Google Pay users. Users who link bank accounts to Google Pay, Plex or others will be able to track spending habits and trends over time via an “Insights” tab, where users can search and group transactions over categories, receipts or merchants.

The app focuses on the most frequent transactions and organizes them around tabs and “conversations” that consider the individuals and businesses paid most often. The grouping functions aid in visibility, streamline transactions and track a trail of payments between parties — much in the way that a string of emails shows the progression of communications between parties, but here with debits and credits (and even refunds) presented in a single, related thread.

Google Pay also allows its 150 million users to redeem offers (through an “Explore” tab) in-app, via tap — and the discounts and promotions are automatically applied whether the transaction occurs in-store or online (the offers come directly from merchants or through aggregators). With the integration of Google Lens, Google Pay users can scan product barcodes or QR codes straight from Google Pay and make purchases. The integration with Gmail makes it possible for receipts and bill payments to become part of the transaction and spend management functionality.

Google has taken a “privacy-forward” design approach to Google Pay, and says it won’t sell data to third parties or share transaction history with the rest of Google for ad targeting. The personalization setting is off by default, but users can turn it on to try for three months, and then turn it off if they don’t like it. Keeping the setting turned on fine-tunes the offers presented to users.

Google Pay is also voice-activated, with capabilities available at a variety of connected endpoints and information that is synched across them.

Raising The Bar

The public showing of the redesigned Google Pay is less than a week old, but already there are important insights into how it could reshape the commerce landscape and the players operating within it.

The Google Pay ecosystem creates an incentive for third parties to compete for the consumer’s time and attention by making their products and services innovative and unique — and for Google Pay to make it easy for new players to become an integrated part of their ecosystem and to add value for its users.

Banks who become part of Plex will create products that support their customers’ payments, banking, money management and credit needs, in hopes that they will be compelling enough to become their primary bank. With Plex, Google Pay can offer consumers banking services without being a bank, and without asking consumers to trust Google as their bank. With Plex, participating banks can also tailor new banking services for businesses and merchants given their visibility into transaction and payments flows — building on what they do best, and offering consumers and businesses new ways to get and consume those services. Smaller FIs will have an opportunity to find new customers in new and different ways. Existing financial institutions will up their own games to compete.

With that competition will come innovation — and consumers and businesses will both benefit.

Merchants that become more integrated with Google Pay will be motivated to create offers and promotions tailored to the opt-in preferences of Google Pay users, potentially reducing their cost of customer acquisition and increasing their odds of making a sale. This universe of merchants also includes Shopify merchants, which are now part of Google’s Shopping platform and have access to a new set of customers who opt-in to certain preferences. Any merchant found via a Google search has a shot at becoming part of a bigger, commerce-first ecosystem — and attracting the new customer eyeballs and the spend that brings.

Google Pay is available on iPhones and Android devices. In the past, iPhone users might not have thought much about downloading the Google Pay app, given that it wasn’t all that useful within the Apple ecosystem. But with its status as a commerce super app, with QR code functionality that can also be used to check out in the physical store, iPhone users (37 percent of whom use Chrome as their browser, in a sign of Google loyalty) could become a lot more interested.

Less than a week in, it’s way too soon to tell whether Google Pay is super enough to take off as a super app.

But it certainly sets the bar for everyone else — including Apple, whose single-use app, inside an ecosystem it keeps closed oh-so-tightly, seems so yesterday.