One of the biggest pain points for both consumers and merchants is expired payment credentials. With card life-cycle management solutions, vaults can ease that pain by providing dynamic updates to cards that are reissued for any reason. These connections to the card networks or with third parties provide for minimal impact to transaction activity when a card is reissued to a cardholder.

One advantage of a third-party vault with card life-cycle services is that for customers with multiple gateway integrations, a single card update at the vault is all that is needed to update payment information. Clients with multiple vaults with gateway providers may be paying several times for a single card update. A third-party vault provider processes a single update to a card on file, and then it can transact across all integrated gateways. Enabling life-cycle management reduces costs, false declines and customer churn due to failed payments. This supports merchants in retaining transactions and protecting lifetime customer value.

Network tokenization offers similar value in that the underlying network token can be used to transact independently from the underlying payment account number (PAN) of the credit card. Modern vaults can provision network tokens automatically when a new card is being stored. That network token can then transact independently of the underlying PAN. This not only reduces the reliance on manual updates to card information by customers but also keeps update costs down while offering significant other benefits, such as higher throughput and lower processing costs. Card life-cycle management and network tokenization features work in concert to keep cardholders transacting freely across all recurring transaction business models.

Consumers want convenience, but security still matters

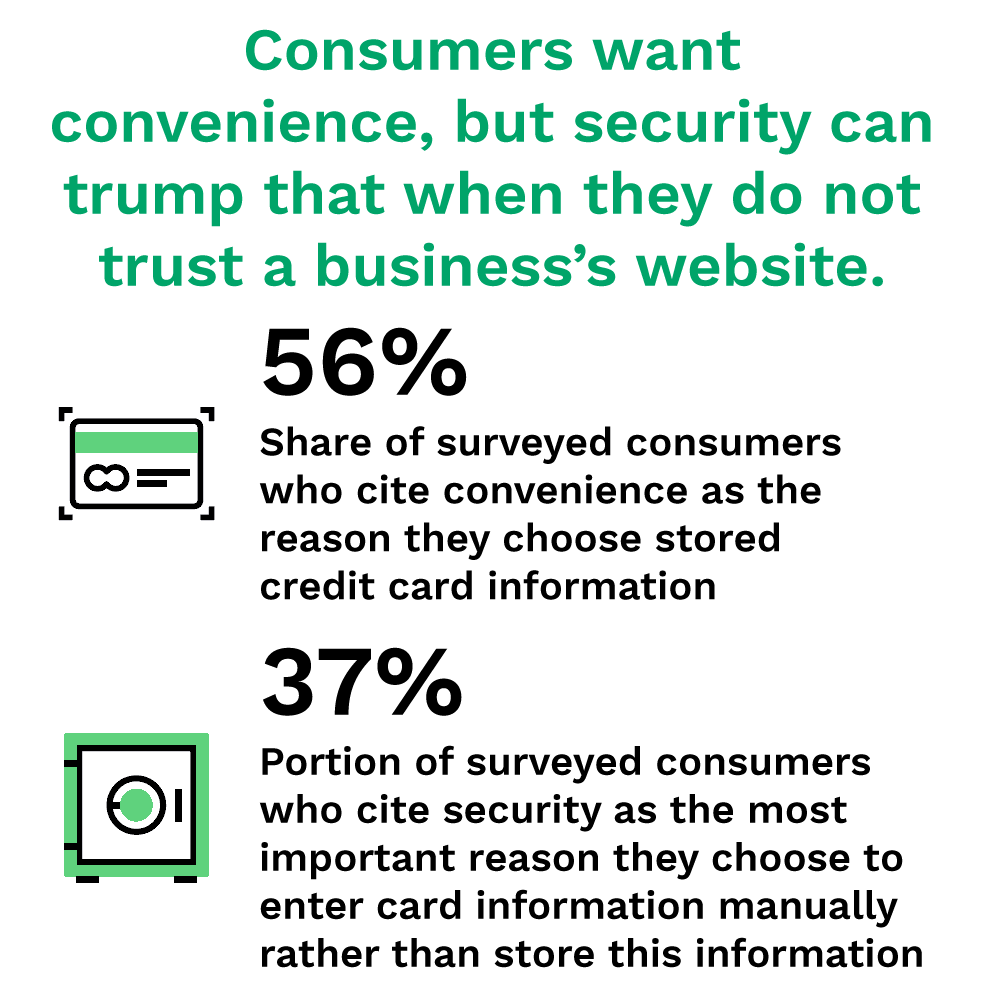

Consumers want to be able to transact securely, but they also want that experience to be easy and seamless. Fifty-six percent of consumers choose stored credit cards over inputting payments information manually because it is more convenient. The less customers must do to complete transactions, the happier they are — and the more likely they are to complete them.

However, security can drive consumers to choose to enter credit card information manually rather than trusting a website with storing that data. Thirty-seven percent of consumers said that security is the most important reason they choose to enter card data manually rather than using stored payment credentials.

However, security can drive consumers to choose to enter credit card information manually rather than trusting a website with storing that data. Thirty-seven percent of consumers said that security is the most important reason they choose to enter card data manually rather than using stored payment credentials.

Tokenization does more than just cards

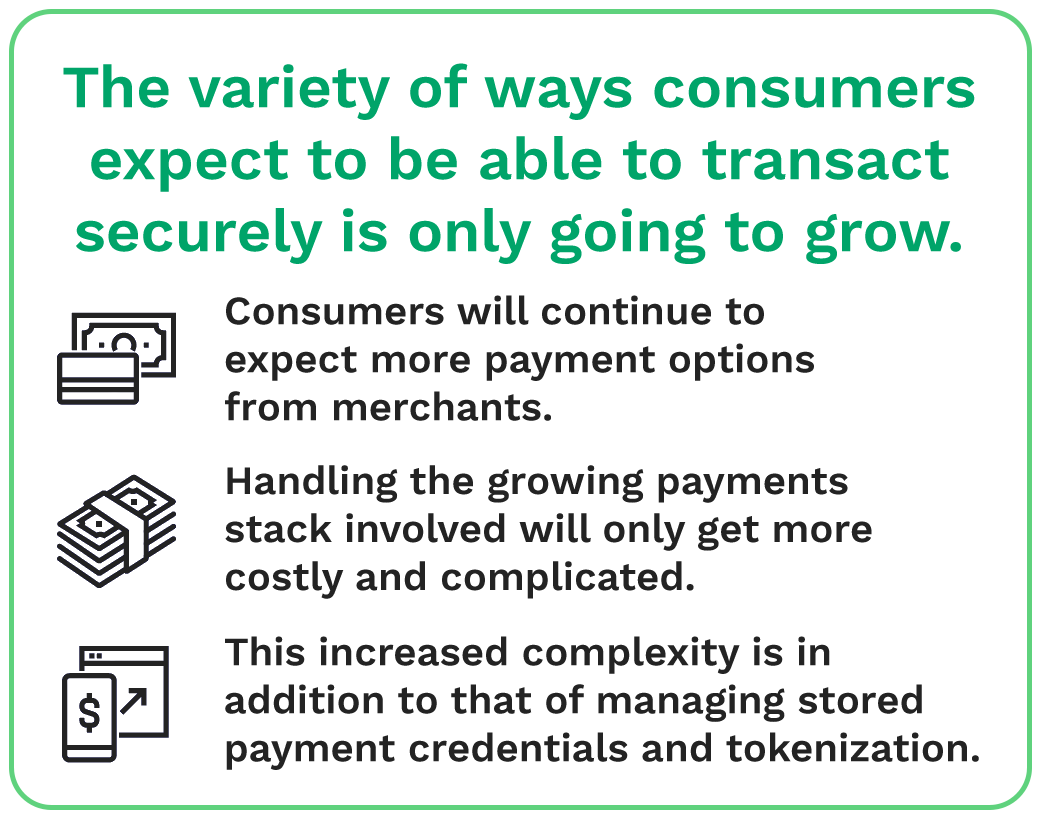

Merchants and merchant aggregators are increasingly adopting diverse payment methods to keep up with consumer expectations and demands. This can lead to an extensive and difficult-to-manage payments stack that eats up company resources and requires constant updates and improvements. However, the number of payment options and the technology involved likely will only continue to expand.

Tokenization can already be used to secure a variety of payment method details, such as the bank information needed to make ACH payments. Modern vaults are not simply storing card payment details but also can be used to protect any sensitive data that is vital for payment processing.