Even though nonbanks are just what the name implies, in the eyes of regulators, some say it might be easier to treat them as if they were.

For FinTechs, that approach may have a bit of a dampening effect on efforts to offer banking and related services outside the realm of traditional lenders.

To that end, as noted in The Wall Street Journal on Wednesday (Nov. 23), more federal oversight looms for nonbanks through the Financial Stability Oversight Council. Paving the road to that oversight would come by designating those nonbanks as systemically important financial institutions, according to reports. The goal is to address threats to the financial system from firms that don’t fall under the purview of traditional oversight of the financial services sector.

The Treasury Department has said, “the FSOC considers a ‘threat to the financial stability of the United States’ to exist if a nonbank financial company’s material financial distress or activities could be transmitted to, or otherwise affect, other firms or markets, thereby causing a broader impairment of financial intermediation or of financial market functioning.”

Beyond Hedge Funds and Cryptos

The roster of nonbanks is broad — in this case, involving entities as far-flung as hedge funds, asset managers and, not surprisingly, crypto exchanges. According to the FSOC documentation in the Federal Register from the FSOC from a decade ago, six quantitative thresholds apply to these nonbanks, among them: $50 billion in total consolidated assets; $3.5 billion of derivative liabilities; and a 15 to 1 leverage ratio of total consolidated assets to total equity.

Most immediately, designating crypto exchanges as SIFI would start to rein in the opaque activities of companies such as FTX. And within the nonbank, neobank and FinTech spaces, those aforementioned thresholds (which open the gate to further review) would winnow out all but the largest players (a PayPal, perhaps).

But nonbank lenders and others (Affirm, as they collect assets in the tens of billions of dollars, start to cross many of the quantitative thresholds.

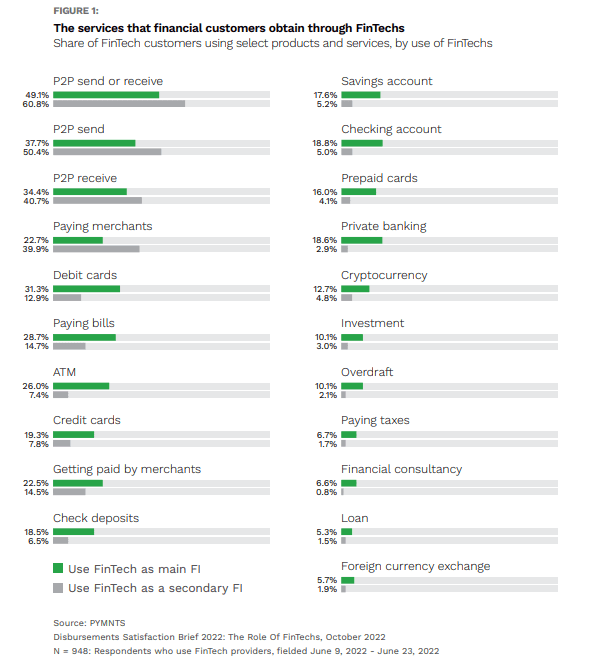

Recent PYMNTS’ research shows that 39% of consumers use FinTechs in some capacity, whether as their primary or secondary financial institution. And with a bit more granular insight, in the report “The Role of FinTechs: Disbursements Satisfaction Series 2022,” we see the broad range of services embraced by consumers. A mid-teens percentage point population of those who use FinTechs as their primary FIs use them for checking and savings accounts, which indicates that deposit/asset bases are growing; another 12% use them for cryptos. The net is being cast wider by the regulators, and it may be the case that worries over systemic risks — and limits over what these enterprises can and cannot do — wind up keeping these firms from becoming more connected within the traditional banking ecosystem.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More