For 60 years, Walmart’s stores have dotted the American landscape, its cavernous Supercenters serving as the one-stop-shop of choice for value-minded consumers, often in rural or modest communities that offered few other choices.

Fast forward to the present, and a year of rising prices fueled by record inflation has been able to do things for Walmart that the Arkansas-based brand could never do on its own.

“We’ve continued to gain grocery market share from households across income demographics with nearly three-quarters of the share gain coming from those exceeding $100,000 in annual income,” Walmart CFO John David Rainey told investors and analysts on the retailer’s third-quarter earnings call last week.

In doing so, the company’s newly hired executive dispelled a long-standing belief that capped Walmart’s reach to lower income demographics. While the company’s value prop still rings true with stressed and stretched consumers, Rainey’s revelation confirmed that “everyday low prices” now appeal to the wealthy.

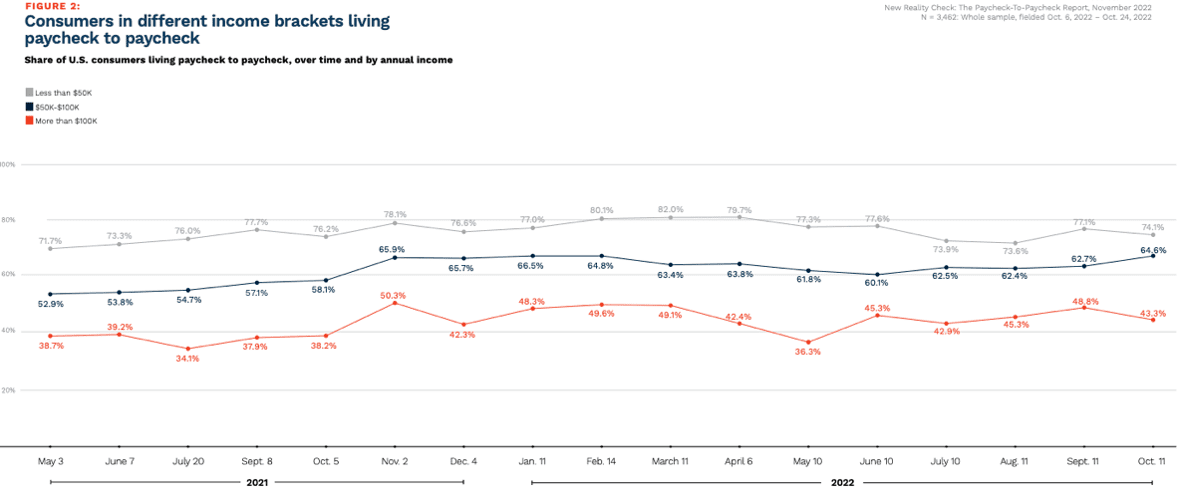

Makes sense to us. Digging into findings from the latest “New Reality Check: The Paycheck-To-Paycheck Report: Holiday Shopping Edition,” a PYMNTS and LendingClub collaboration, we see that in October 2022, “43% of those earning more than $100,000 per year reported living paycheck to paycheck,” up 38% in the same period last year. Eat the rich? We think not.

Read more: Walmart Says Inventory is Down and $100K+ Shoppers Are Up

At Home With Renovating

Not long after, another logic-challenging shocker was delivered. After taking in the fact that six-figure earners are relying more and more on discounted groceries, we learned that spending on home improvements is not, in fact, cratering like the broader housing market which coincidentally delivered its ninth consecutive monthly retreat this week.

Seriously? Yes. Quite.

“Even in the U.S. market where home prices have declined after a particularly steep run-up during the pandemic, we are not seeing any impact to sales,” Lowe’s CEO Marvin Ellison said on the retailer’s third-quarter earnings call Wednesday (Nov. 16), adding that higher home prices and owner-equity, an aging housing stock and disposable income are three preeminent factors driving this demand.

As goes Lowe’s so goes The Home Depot, more or less, also handing in better-than-expected Q3 results on Tuesday (Nov. 15), at which time CEO Ted Decker told analysts, “We are pleased with the traction we are seeing in our interconnected business as we continue to build on our momentum with both our Pro and DIY customers.”

Decker chalked much of this up to “better functionality and capabilities in our Home Depot app where we see greater engagement. In fact, throughout the year, we have seen strong double-digit growth in monthly active users versus last year.”

Also read: Lowe’s Says Home Remodeling Trend Still Strong and Set to Boom

In both cases, the country’s two largest home improvement retailers flipped the script and said because of the weak housing market and mortgage rates popping to a 20-year high, their big-spending Pro customers overwhelmingly expect to do more work next year than they did this year.

“This unique combination of factors is causing homeowners to trade-up in place, preferring to invest in repairs and renovations to make their current homes meet their family’s evolving needs, rather than buying a new home,” Ellison said, specifically challenging what he called common misperceptions about the home improvement business.

Another Miracle on 34th Street

Macy’s has been counted out more times than there are floats in its Thanksgiving Day parade, it seems, filing bankruptcy in 1992, again in 2003, and barely escaping it once more in 2020.

Fast forward to this post-COVID, hyper-inflation, “pre-cessionary” world we live in today, and The Weekender is happy to say that Macy’s military-sounding “Polaris strategy” has given the icon of American department store retailing reason for holiday cheer.

“It’s a different company than we were back in March of 2020,” CEO Jeff Gennette said in summing up the retailer’s Q3 earnings on Thursday (Nov. 17).

Reclaiming the “timeless” appeal of one-stop-shopping experiences across a portfolio that also includes upscale Bloomingdale’s, Gennette talked up digital initiatives galore, as well as the success of the Toys R Us store-in-store partnership that he said will be a permanent fixture in all 500+ brick and mortar locations.

“Overall the Toys R Us customer is younger and more diverse than our Macy’s customer and we have discovered that 85% of Toys R Us customers are cross shopping,” Gennette said. The deal is “a great example of finding a hole in the market and strategically filling it, gaining share and loyalty and creating lasting memories for children and adults alike,” he said. sounding more like a scene from Elf than the musing of 40-year company veteran who has been there and back again.

“I’d say the headline here is that we’re a more modern department store,” he added.

See also: Macy’s CEO: ‘We’re a Financially Strong, More Modern Department Store’

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More