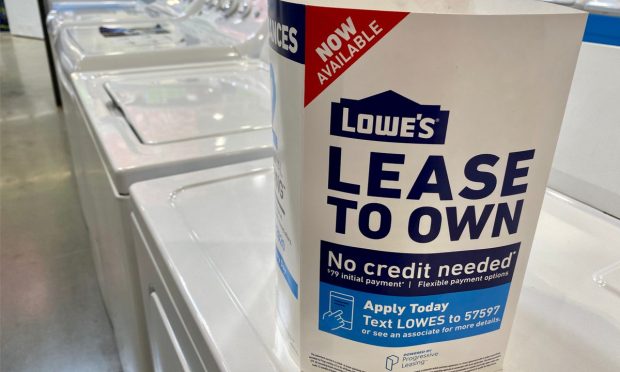

As inflation puts more pressure on already strained pocketbooks and with millions of households now living paycheck to paycheck — including many making over $100,000 a year — durable goods retailers are keenly interested in making sure their payment options are aligned with 2022 realities.

PYMNTS research found that consumers are leaning more into lease-to-own (LTO) options for reasons ranging from bad credit/thin file to the installments-style flexibility it offers at a time of continuing economic uncertainty where in which the pandemic is passing the bad news baton to inflation.

“Finding Retail’s Invisibles: Leveraging Flexible Digital Payments to Reach New Durable Goods Customers,” a PYMNTS and Katapult collaboration, noted: “A sample representative of nearly one-quarter of adult American consumers who purchased durable goods in the past 12 months reported that they were very interested in participating in lease-to-own programs,” translating to up to 46 million new consumers for retailers equipped with LTO financing.

Get the study: Leveraging Flexible Digital Payments to Reach New Durable Goods Customers

What’s good for the customer is good for the retailer, as Katapult CEO Orlando “Oz” Zayas told PYMNTS in an interview.

“For retailers, [LTO] brings a new incremental customer,” he said.

While retail credit approval typically runs as high as 70%, Zayas said “there’s still a wide swath of people that are not getting approved. What eCommerce retailers specifically have found is that the customer who’s shopping for financing needs a solution now. It’s not like walking into a store and thinking about it and coming back later.”

Retailers that see the writing on the wall are capitalizing on that urgency with LTO solutions that have flipped the script on rent-to-own concepts seen as predatory and unforgiving.

“We’ve all had it where you build a shopping cart and then you leave for whatever reason, and all of a sudden you’re getting emails and texts from that retailer saying, ‘Hey, you left a cart open,’” Zayas said. “The reason that is, and the same with financing and lease-to-own, is that you’ve got to capture that customer when they’re making the transaction.”

LTO Beefs Up the Bottom Line

Having done tests showing that LTO sales are genuinely incremental, Zayas told PYMNTS that being “able to capture the sale at the time of purchase … develops a loyal customer.”

“It boils down to prioritization,” he said. “If you look at how much volume we can bring a retailer, it’s anywhere from 3% to 10%, maybe 15% of incremental sales, which is a huge amount. For any retailer, even a 4% increase in sales, and they’ll jump at the chance.”

With retailers still in a whirlwind of adopting and integrating many pandemic-era digital tools, there can be integration hesitation with concepts like LTO. With Katapult’s integrations with platforms including Shopify, BigCommerce and Magento, Zayas said that’s really not a barrier.

“We have [application programming interfaces (APIs)] set up, and [retailers] can, in as quickly as a day, have us as an option in their shopping cart,” he said. “If it’s a waterfall integration, we do have an integration with Affirm where if they’re an Affirm customer, we can turn on what’s called Affirm Connect and within a day or two, be in the waterfall and start getting the application flow.”

Legacy retailers are more challenging, but that’s rapidly changing too. Zayas said “some of the larger retailers where there’s old point-of-sale systems” don’t always see the financial benefit of changing POS to handle LTO financing.

The convincer is incremental sales that can be quantified, and more importantly, adding LTO gives retailers the opportunity to gain new customers with a solid sense of loyalty.

“A few years ago, the Federal Reserve came out with the statistic that said 40% of the population has trouble if they have a $400 emergency,” Zayas said. That’s the population we’re trying to serve, and we’re trying to serve them in a clear and transparent way. If the retailer gets that, they can tap into a new customer base.”

See also: 75% of Lease-to-Own Consumers Say It’s Their Only Option to Obtain Durable Goods

Communicating a Deeper Loyalty

Adding to inflation and the malingering pandemic is oncoming tax season. But Zayas said these are fairly ideal conditions for LTO consumers, and by extension, the retailers they buy from.

“[LTO] does bring a new customer who is loyal because they were shunned or discouraged [at] other retailers, and we gave them the options they need,” he said.

As it pertains to the retailer, getting the word out on LTO’s availability is important. Retailers decide how to present the option at checkout, and there are several variations.

“Some retailers will have a financing page,” he said. “In the checkout itself, you’ll see the prime options — Visa, Mastercard, what other options they may have for financing — and then they’ll have lease-to-own. We call it the NASCAR checkout with all the different names.”

“We usually put ours with a little tagline on it [saying], ‘No credit required,’ and that helps the customer self-identify, ‘My credit’s not so great. I want to try this option,’” he added. “Then when they apply, it’s real simple information that we get.”

As this is happening online, “They’re not in a store getting dazzled with all this new stuff that they can buy,” Zayas said. “They’ll have a finance page, they’ll have it in the checkout, they’ll do social media letting them know that there’s an option available,” which brings LTO into social selling.

Read also: Katapult Says 2021 Was the Year of Inclusion

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More