Merchants playing catch-up with consumer payment choice may more easily offer options with a third-party partnership.

Retailers operating primarily in the brick-and-mortar space have had a tough time keeping up. eCommerce’s continued grab of brick-and-mortar market share cannot be understated as consumers increasingly shop online for both seasonal items and everyday goods. In some cases, such as pet products, over half of consumers have embraced the convenience digital channels provide when purchasing these items.

This shift in consumer preference has ushered in an urgency for brick-and-mortar retailers to adopt certain eCommerce-led customer loyalty features, offering a more cross-channel shopping experience. Some of the tools implemented include in-store app features, hyper-personalized card-linked offers — and, perhaps most importantly when it comes to consumer demand, increased payment options.

The most recent PYMNTS and ACI Worldwide collaboration, “Retail Payments Innovation Year in Review,” outlines how U.S. retailers’ current or planned payments innovation investments vary, ranging from offering payment plans such as buy now, pay later (BNPL) to accepting QR codes at checkout.

Source: PYMNTS Navigating Big Retail’s Digital Shift, December 2022 N = 151: Responses from U.S.-based retailers, June 1, 2022 – June 21, 2022

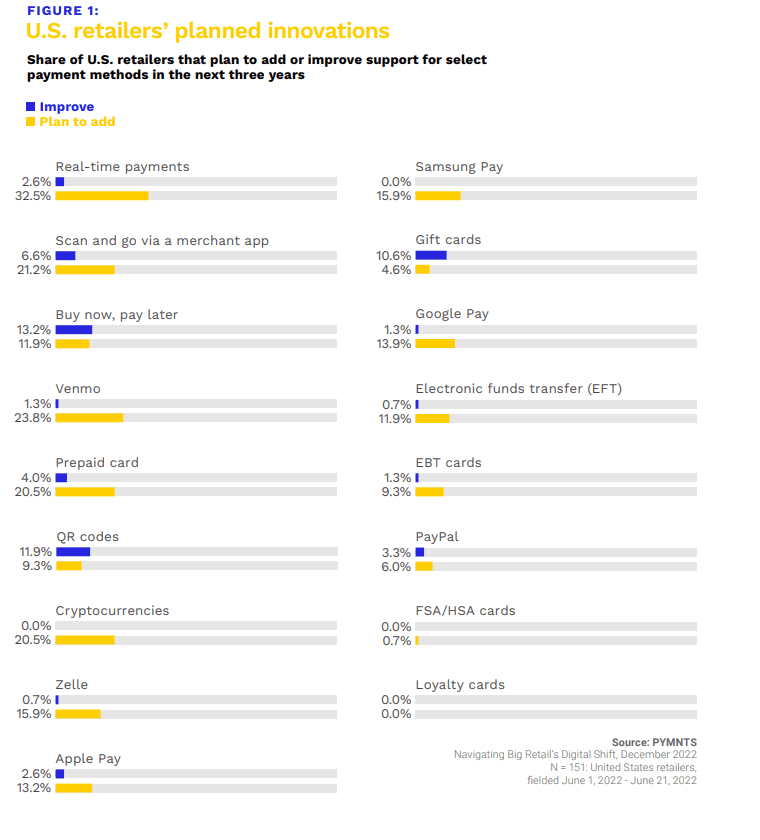

As the chart demonstrates, there is disparity between improvements and planned implementation. Merchants planning to improve on a select innovation already have the tool in place, while retailers planning to add an innovation could be starting from scratch. For example, although just 2.6% of U.S. retailers plan to improve the real-time payments support they have in the next three years, 33% plan to get started with real-time payments by launching support. Some merchants seem to be just getting a handle on consumer-facing offerings such as BNPL and peer-to-peer (P2P) products such as PayPal or Zelle. Ultimately, the payment method businesses are most looking to add are real-time payments.

Real-time payments are not exactly new to the United States. The Clearing House launched the RTP network in 2017, modernizing accounts payable (AP) systems that once may have relied on legacy systems such as wire transfers and paper checks. Since then, real-time payments capabilities have evolved, allowing for uses within retail and other consumer-facing sectors. For retailers, the benefits of implementing real-time payments go beyond offering consumers the speed and transparency of online shopping in-store. They can also enhance data tracking and loyalty programs, engage customers at the point of sale, as well as supporting other rising consumer-facing innovations, such as scan-and-go. Indeed, 64% of surveyed U.S. retailers plan to implement payment-related innovations to attract new customers, while 62% say it is to improve customer retention.

In an interview with PYMNTS, ACI Worldwide Chief Product Officer Debbie Guerra emphasized the importance for merchants to offer innovative payment choice. Real-time payments “create an unprecedented operational complexity for participants — but it also provides a once-in-a-generation opportunity for new [payments] offerings.” She continued, “If you’re a merchant today, you want to be able to offer the payment methods that your consumers want to use and in the ways in which they want to engage … no matter if it’s through their cellphone, their mobile device, whether it’s in person or across different modalities.”

While adoption of real-time payments by U.S. merchants remains low, its popularity is growing among retailers. Although excitement among U.S. retailers in adopting payments-related innovations is high, most aren’t interested in going it alone with it comes to implementing new payment methods. Fifty-one percent of U.S. retailers said they plan to outsource payment method innovation, while 30% planned to utilize some mix of in-house and outsourced solutions.

Retailers interested in implementing real-time payments innovation should look for a technology solution or provider allowing them to optimize the user experience and manage compliance through a single system. For example, ACI offers software solutions to support retailers offering real-time payments while firms such as Nuvei has developed a pay-by-bank instant solution.

The effort by merchants to meet the need of evolving consumer behavior and demands, especially when it comes to innovating payment choice, may initially seem like more of a headache than it is worth. However, with the right partner’s support, the long-term loyalty benefits may well outweigh any initial implementation efforts.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More