Dozens of mergers scuttled. Dwindling share prices. A market that is so volatile that, frankly, it’s no surprise that special purpose acquisition companies (SPACs) have seemingly had their run and now are done.

Bloomberg reported Wednesday (June 29) that more than two dozen firms have called off mergers with so-called blank check companies this year. The volatility in the markets, and the looming threat of recession of course are playing a role. So is the specter of regulation.

As noted in this space, there’s some push and pull over just how SPACs should be regulated.

Groups representing the U.S. financial industry are trying to get the federal Securities and Exchange Commission (SEC) to dilute proposed new regulations. The SEC and other bodies are wary of SPACs’ rather lax rules governing projections and financial disclosures.

Read also: US Financial Groups Back SPACs as SEC Seeks to Rein Them In

But it seems a certainty that some tightening will be in order. The falloff in SPAC activity reflects this — indeed, is an anticipation of sorts that investor enthusiasm for the investment vehicles will wane.

To recap, SPACs are “shell companies” listed on the stock market that hunt for private companies to buy and take public. Very roughly speaking, they have two years in which to get a deal done, and then, typically, investors can redeem their money and the vehicle is unwound.

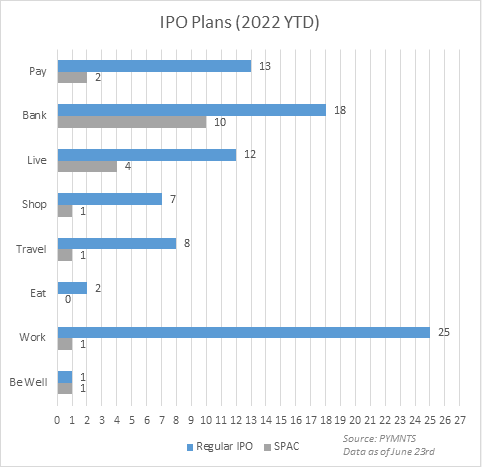

As PYMNTS’ own data show, the traditional initial public offering (IPO) — the model where companies come to market with roadshows and with traditional SEC documents and direct sales in place — have thus far outpaced SPACs, sometimes by an order of magnitude. The launches that are planned are not the ones that come to market, of course, and anything can happen between now and then.

Only last month, it was reported that dealmakers looking at taking companies public through SPAC mergers are having trouble finding investors. As a result, many dealmakers have been making “short-term agreements” with funds and other means of alternative financing.

Read more: SPACs Turn to Alternative Funding as Investor Cash Dries Up

Short terms agreements do not auger well for long term business models. For the SPACs, the tapping of alternative levels of financing mean that the “easy” money has been made, and that the retail and institutional players who had been so ardent just a few months ago are — now — less than enthused.

That leaves an avenue of “exit strategy” decidedly and increasingly off limits to the nascent companies that might have been looking for capital and backing to go public and to launch new products and services.

In the end, the heyday is over, the cold light of day hits a once-hot sector — and Wall Street moves onto the new, new thing.