Although the real estate market remains too hot for some first-time buyers, rental prices are finally sinking.

This is according to CoreLogic’s recently released Single-Family Rent Index, which analyzes rental prices across the U.S., finding that nationally, rents are still higher than pre-pandemic levels. At 6.4% annually, they have risen an average $300 per unit over the past two years. This tide may be turning, however, as the report also noted that rent prices dropped in December for the eighth straight month. Ultimately, the a growth rate at the end of 2022 was half as large as it had been the prior year.

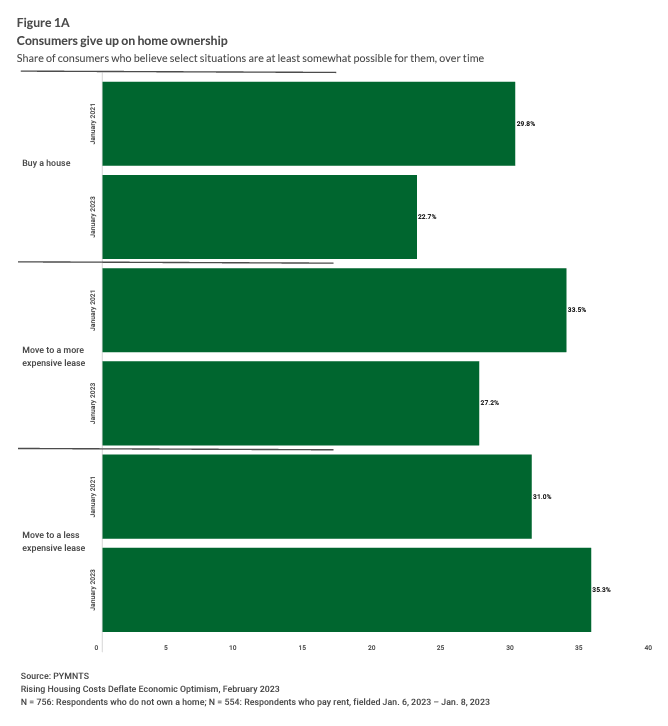

This trend may be good news for renting consumers, whose goals of moving to a more expensive lease may now be more affordable, as surveyed in PYMNTS’ “Consumer Inflation Sentiment: Rising Housing Costs Deflate Economic Optimism.”

The drop of 6 percentage points in the share of consumers believing they can afford a more expensive lease represents a significant share of the U.S. renting population when extrapolated. The sentiment shift could suggest that consumers are giving up on the idea of moving to an improved situation, or the ability to afford increases on a current lease.

Broad hints suggest that rent prices may continue to decline through the year, although affordability for consumers in certain metropolitan markets remains to be seen. Along with CoreLogic’s forecast, rental vacancy rates are also rising, from 5.6% in Q1 2021 to 5.8% in Q4 2022, per the Census Bureau . The slight increase could stem dramatic rent hikes as landlords seek to fill empty properties.

As renters wait for prices to decrease further, they may consider taking advantage of a few tools that are designed to bridge gaps in building renters’ all-important credit history. On-time rental payments aren’t generally included in credit scores, putting renters at a possible disadvantage when it comes time for future lending considerations.

For those living in eligible multifamily homes, last year Fannie Mae rolled out its Multifamily Positive Rent Payment Reporting program to speed up adoption of rent payment reporting. To assist renters looking to buy one day, Fannie Mae is also considering rent payment history when determining creditworthiness of those looking to finance homes.

Additionally, rental financial services company Jetty launched a new service to help renters improve their scores. Offered to select renters as part of Fannie Mae’s Equitable Housing Finance Plan, the service help renters build their credit history by reporting rent payments to all three credit bureaus.

Credit reporting giant Experian has gotten involved, launching a new tool that can help renters contribute qualifying, “positive” residential payments directly to benefit their Experian credit file. Based on the company’s preliminary analysis, 66% of consumers will see an instant increase in their FICO score resulting from the potential impact of positive residential rent payment reporting through its Experian Boost platform.

As the rental market seems likely set to slowly cool nationwide, renters seeking to move to a more expensive lease may have some hope of reaching that goal. Building a credit score, through rental reporting tools and other means, is one way of being prepared when that time comes.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More