Consumer demand for instant disbursements is at a crossroads. More people like the idea of getting that refund or insurance claim deposited directly onto cards or into accounts, but even when offered the option, many have data privacy fears or fee concerns holding them back.

It’s a major issue, as research conducted for “The Disbursements Satisfaction Report 2023: Instant Payouts Reach an Inflection Point,” a PYMNTS and Ingo Money collaboration, finds that 63% of all consumers receive various types of disbursements, but only 22% report receiving them as instant payouts.

This is true even though 68% of consumers would not only prefer instant payouts but over one-quarter of those wanting the service would pay a fee for it.

Now in its sixth year, our latest survey of nearly 2,300 U.S. consumers on this topic found that data security and cost are at the heart of consumer reluctance to use instant disbursements.

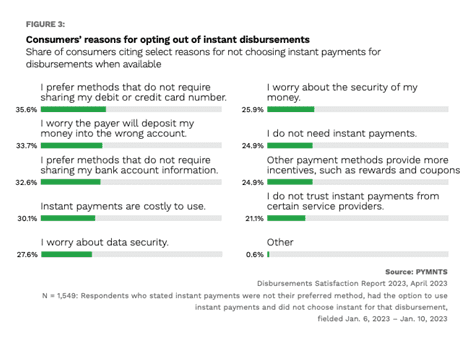

The study notes that 36% of consumers “who had the option to receive an instant disbursement did not because they did not want to share their card information for a push-to-card option, while 33% said they did not utilize an instant disbursement because they did not want to share their bank account information.”

The Reasons for Reluctance

Between inertia among instant disbursement payers and the distrust or disinterest of some consumers, it’s not a surprise that these instant payouts have stalled somewhat. The idea of fees isn’t universally appealing, but it holds some cachet for certain consumers.

With over 60% of U.S. workers living paycheck-to-paycheck, for example, consumers who are keen on instant disbursements without reservation are those awaiting loan payouts.

Per the study, “Consumers receiving borrowed funds are the most likely to report being willing to pay extra for an instant disbursement, at 52%. Thirty-nine percent of consumers who receive income disbursements, such as bonus or gig payments, would pay extra for an instant payout.

“Such a significant share of consumers are willing to pay extra for instant pay suggests that they need the funds immediately and cannot wait the three to five days it could otherwise take for a bank to process a disbursement. This may not be surprising, considering that our research finds that consumers are still facing inflationary pressures and economic uncertainty; it follows that they are more apt to rely on instant income disbursements to meet their mounting financial responsibilities,” the study adds.

On the flip side, make it free and 65% of consumers express interest in doing business with entities offering instant disbursements. “The growth potential highlighted by this finding should not be ignored,” per the study. “Even as our data shows that the current supply is not meeting demand, indications are that the issuers that step in and offer instant disbursements can develop a significant advantage in retaining existing customers while attracting new ones.”

Another factor keeping instant disbursements from catching on more widely is when discounts or other such motivations are offered to use other disbursement methods.

As we found, Gen Z consumers who prefer to receive instant payments “were particularly likely to report opting out of using instant disbursements because of a financial incentive to use a different method, cited by 52%.”

For Gen X, however, it’s the idea of fees turning them off to the concept, as 40% cited this reason for not using such a service.

Get Your Copy: The Disbursements Satisfaction Report 2023: Instant Payouts Reach an Inflection Point