The country’s PesaLink instant payments scheme was first launched in 2017, the same year that the European SEPA Instant Credit Transfer (SCT Inst) scheme went live to facilitate ultra-fast euro payments across the 36 countries within the Single European Payment Area (SEPA).

PesaLink, which has since migrated from ISO 8583 to the ISO 20022 standard, supports use cases such as Request to Pay (RTP), payment initiation and direct debits, and it enables Kenyan consumers and businesses to instantly transfer money between bank accounts. Apart from Kenya shillings, the scheme is also compatible with multiple foreign currencies, including U.S. dollars, euros and pounds sterling.

But despite Kenya having a head start compared to other African counterparts in the development of real-time payment systems, the country’s population has been very slow to adopt instant payments en masse, a trend also seen among several European countries like the Czech Republic, France and Belgium.

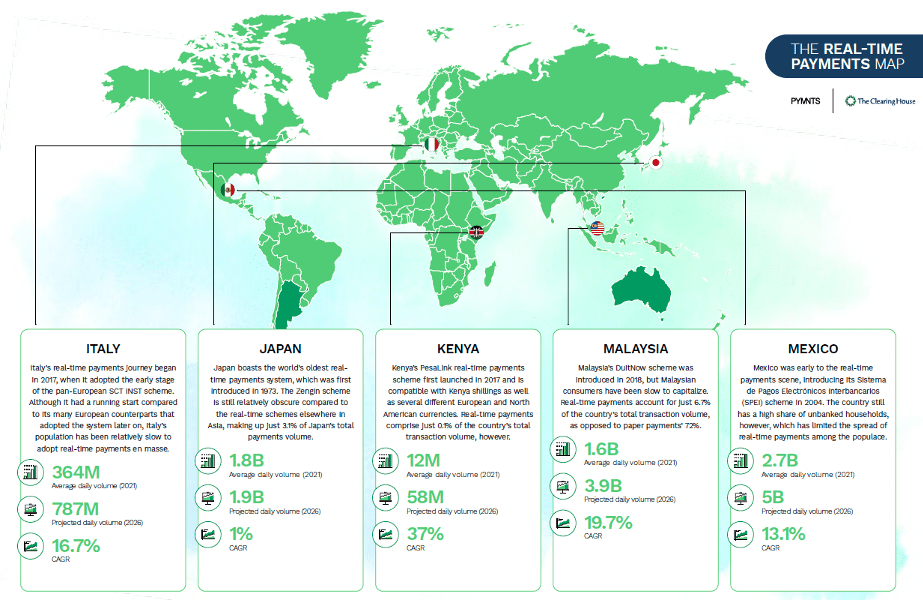

According to the latest “Real-Time Payments World Map,” a PYMNTS study that examines the state of real-time payments across countries around the globe, real-time payments make up just 0.1% of Kenya’s total transaction volume.

Data captured in the study also noted that average daily volume in Kenya is projected to increase from 12 million in 2021 to reach 58 million in 2026, growing at a compound annual growth rate (CAGR) of 37% during that period.

That growth potential further highlights a huge untapped instant payments opportunity when compared to a country of relatively similar population size like Italy where average real-time daily volume is projected to increase from 364 million to 787 million during the same period.

Data in an ACI Worldwide 2023 Prime Time for Real-Time report corroborated these findings and showed that paper-based transactions and electronic payments (excluding real-time payments) dominate the local payments landscape, representing an 84.5% and 15.4% share, respectively, of total payments volume in 2022.

As an explanation for that uneven share, the ACI report pointed to the strong hold that mobile money services, particularly M-Pesa which is used by at least one person in 96% of Kenyan households, currently have on the electronic payments market in Kenya as one of the main reasons hindering the adoption of real-time payments in the country.

“Few Kenyan consumers have access to bank accounts, and mobile money has largely taken the place of formal financial services providers for the majority of Kenyans,” the report stated, adding that a collaboration with Safaricom, the company behind M-Pesa, would be necessary “in order for real-time payments to make any real headway.”

It’s a move that Safaricom CEO Peter Ndegwa said he could likely embrace. In an interview with PYMNTS last year, he referred to the firm as one that is creating “an enabling ecosystem” and is open to partnerships with other players to ensure they are meeting the needs of the customers they serve.

Read more: Safaricom Launches Mobile Wallet and Mini App for Kenyan Students

For all PYMNTS EMEA coverage, subscribe to the daily EMEA Newsletter.