Real-time payments are quickly becoming ubiquitous in developed nations worldwide, with businesses and consumers relying on this payment method in ever-growing numbers.  A PYMNTS study found that 86% of businesses generating between $500 million to $1 billion in annual revenue leverage real-time payments, for example, reporting improved cash flow management capabilities and greater transparency in the payments process.

A PYMNTS study found that 86% of businesses generating between $500 million to $1 billion in annual revenue leverage real-time payments, for example, reporting improved cash flow management capabilities and greater transparency in the payments process.

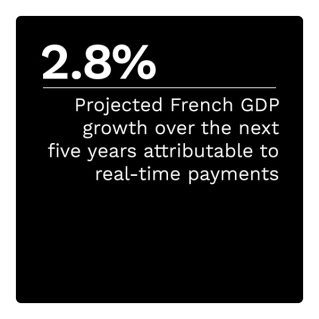

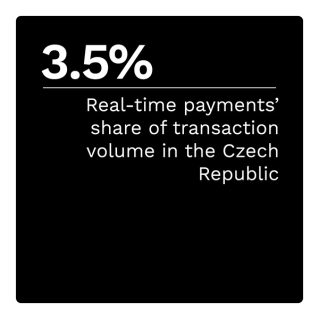

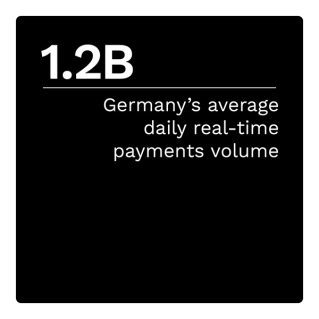

There are now more than 60 countries that possess or are developing a real-time payments scheme, representing approximately 72% of the global population. Each country is taking a different approach to its instant payments system, with many participating in multinational plans to ensure smooth cross-border transactions.  Nowhere has this multilateral approach seen more success than in Europe, where participating European Union countries are leveraging their preexisting economic relationships to ensure a smooth payment experience for their constituents.

Nowhere has this multilateral approach seen more success than in Europe, where participating European Union countries are leveraging their preexisting economic relationships to ensure a smooth payment experience for their constituents.

Several systems facilitate these payments across the continent, including the Single Euro Payments Area (SEPA) Instant Credit Transfer scheme, launched in 2017, allowing for instant cross-border payments within the SEPA region. Some European countries have developed internal payment systems to supplement the existing pan-continental scheme, such as the United Kingdom’s Faster Payments Service, in operation since 2008, and Sweden’s Swish system, launched in 2012.

Concerns about fraud have plagued real-time payment systems since their inception, as the sender cannot reverse these transactions once the funds instantly arrive at their recipient. The EU has tried to combat this via the Payment Services Directive 2 (PSD2), which introduced new requirements for strong customer authentication. All electronic payments must authenticate using at least two factors, such as a password and a fingerprint, to ensure that only authorized individuals can access the accounts.

Efforts like these will shape the real-time payments scene around the world as the industry grows more widespread and sophisticated. The “Real-Time Payments World Map,” a collaboration with The Clearing House, examines real-time payments systems worldwide, with this issue focusing on five European nations in particular.