Small businesses aiming to expand their eCommerce presence across borders in 2023 may want to keep cross-border frictions top of mind.

Whether domestic or international, payments management is resource-intensive but essential to a business’s stability. Small businesses, startups and leaner organizations seeking to expand their reach beyond domestic confines can thus face difficulties navigating this space. Challenges include ensuring payments are compliant with global regulations and customs, managing multiple currencies and managing accounts payable and receivable. Research has found that navigating cross-border payment complexity is a leading limitation to growth for 27% of small and midsized businesses (SMBs).

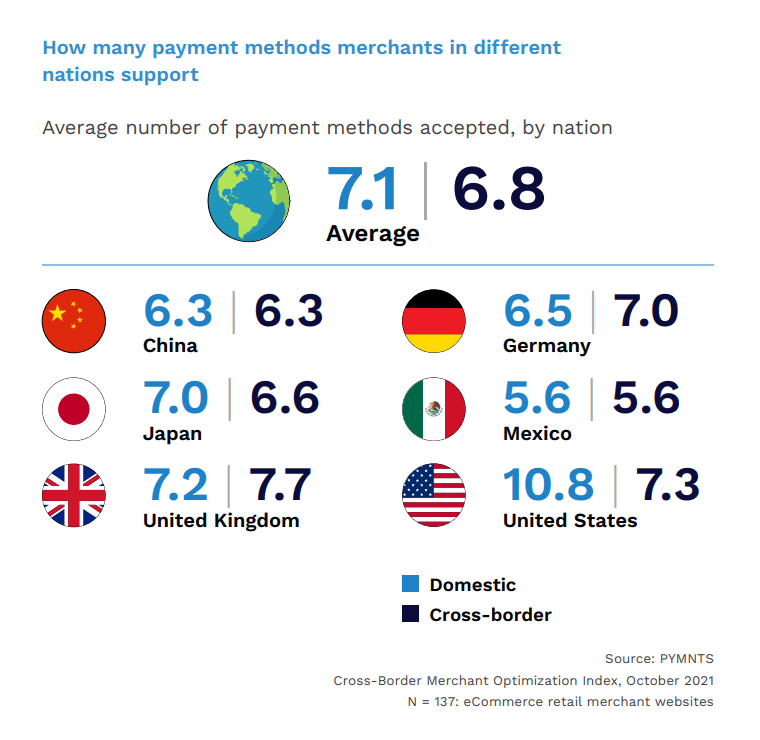

One example of this payments complexity in action: PYMNTS has found that the number of payment methods merchants in different countries accept can vary wildly. The average merchant in Mexico accepts just 5.6 payment cross-border payment methods, for example, whereas in the U.S., the average U.S. merchant accepts 7.3 internationally and 10.8 domestically. Additionally, friction between platforms can result in delay-based fluctuations in cross-border payment processing times, making it harder for SMBs to accurately estimate future revenue streams. As many SMBs operate under slim margins, any erratic payments could quickly become a critical problem.

To avoid payment delays, SMBs may seek a more appropriate cross-border digital solution that incorporates faster or real-time payment functionality — including an easy-to-use experience providing customers with critical details such as current exchange rates and accurate delivery dates.

Understanding this growing demand, the majority of financial institutions (FIs) do currently offer business customers an array of digital tools to facilitate international payments. However, most FIs are also aware that their solutions could be more effective at addressing payment friction for the businesses they serve.

For small businesses exploring their global reach, a third-party solution may be the simplest and most effective way to handle cross-border payment frictions. This type of one-tool solution often is able to onboard and manage new client and customer payments internationally more seamlessly than other options, which could afford SMBs much-needed agility in reacting to fresh opportunities. A compliant and regulation-aware payments partner can also offer SMBs valuable expertise and knowledge.

Future (or near future) solutions could be on their way to the economy at large. Groundwork is rapidly being made toward a U.S. digital dollar, for example; partners for that project include the New York Federal Reserve and leading financial institutions such as Wells Fargo, Citi, TD Bank and Mastercard. The digital currency aims to allow for more efficient and safer cross-border payments — a particularly timely development, as FIs are reporting that the battle against fraud is intensifying.

Navigating cross-border payments does not have to be a seemingly insurmountable obstacle or someday aspiration. Entrepreneurs once might have been restricted to a domestic consumer base due to a lack of time or available effort. With more third-party platform partners to choose from and the digital dollar potentially on the horizon, they can contemplate going global in streamlined, efficient ways previous businesses may never have thought possible.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More